1. Introduction

The European Union (EU) Emissions Trading System (ETS) is often characterized as a cornerstone of EU climate policy. Since its establishment in 2005,Footnote 1 the scheme has undergone 17 revisions, progressively broadening its scope to encompass a variety of greenhouse gases (GHGs) and economic activities. The EU ETS covers emissions from power generation, heavy industry, and aviation within the European Economic Area.Footnote 2 The latest legislative revision of 2023 extended the scheme to maritime transport, while a separate emissions trading scheme will be established to cover fuel combustion in buildings, road vehicles and additional sectors.Footnote 3 However, as the EU carbon market and the associated scholarly literature have expanded, less explicit attention has been paid to its core objectives: which goals does the EU ETS, along with its subsequent amendments and expansions, aim to achieve?

According to Article 1 of the EU ETS Directive, the ETS aims ‘to promote reductions of greenhouse gas emissions in a cost-effective and economically efficient manner’.Footnote 4 Yet, what does the objectiveFootnote 5 of ‘promoting’ GHG emissions reductions entail? What do ‘cost-effective’ and ‘economically efficient’ mean in this context? Does the scheme pursue additional (sub-)goals beyond those outlined in Article 1 and, if it does, is there a legal hierarchy among these objectives? These are not marginal theoretical considerations but constitute key questions with also practical implications. As Quemin and Pahle point out, clarifying the ambiguous scope of the objectives pursued by the EU ETS Directive is necessary for defining a normative benchmark for the functioning of the carbon market.Footnote 6

This article aims to answer the aforementioned questions and develop a framework for evaluating the EU ETS and its amendments, based on a systematic analysis of the objectives of the scheme, as enshrined in EU law. In general, such objectives can either be purely ‘internal’ to a legal system, such as the goal of maintaining coherence with other legal norms, or can express non-legal considerations that have been ‘internalized’ into law by the legislators, such as the goal of economic efficiency.Footnote 7 To our knowledge, the internal normative framework of the EU ETS Directive – namely, the framework of the internal(ized) goals it pursues – has not yet been mapped. By doing so, our analysis supports decision-making and climate policy evaluation in three ways. Firstly, it can facilitate future evaluations of the EU ETS to be more comprehensive and consistent by providing a set of criteria that capture the nuances of and relationships between the specific goals of the emissions trading legislation. Secondly, it can aid in mitigating bias in the selection and prioritization of evaluation criteria. Thirdly, it can improve transparency and comparability across different evaluations of the EU ETS, as explained below.

As evaluations are inherently normative, they require a set of explicit or implicit criteria as a basis for formulating assessments.Footnote 8 Various publications have applied different (combinations of) criteria to evaluate amendments to the EU ETS.Footnote 9 While certain aspects have been commonly examined, such as the level and costs of emissions abatement, there are nonetheless important variations, both in the objectives identified and in the formulation of the criteria.Footnote 10 Even the European Commission has refrained from precisely defining the overall objectives of the EU ETS, and has instead used different formulations of the criteria in its impact assessments over the years.Footnote 11 This heterogeneity of normative frameworks across EU ETS evaluation studies poses challenges in comparing and synthesizing their findings. Moreover, many evaluations focus predominantly on economic criteria and disregard other relevant considerations of a legal or institutional nature.Footnote 12

Such legal-institutional aspects have been addressed by earlier legal scholarship on emissions trading, upon which our article builds.Footnote 13 This scholarship has, among others, shed light on the competing conceptual models that underlie the different designs of emissions trading systems.Footnote 14 It has also reviewed certain policy objectives that emissions trading systems often pursue, highlighting that their simultaneous attainment necessitates compromises and trade-offs between different goals.Footnote 15 Our contribution is a first endeavour to go beyond generic policy objectives and systematically analyze the specific legal objectives of the EU ETS, namely, the goals embedded in current EU emissions trading legislation.

The remainder of the article is organized as follows. Section 2 highlights the methodological value of using legal objectives as bases for evaluations and explains the document analysis method used to identify the goals enshrined in the EU ETS legislation. Section 3 presents the findings and employs the legal-dogmatic method to interpret and prioritize the identified objectives,Footnote 16 taking into account primary and secondary EU law and case law of the Court of Justice of the EU (CJEU).Footnote 17 Complementing the legal analysis, Section 4 draws insights from economic theory to appreciate the economic rationale of the EU ETS as a market-based mechanism. Section 5 combines the findings of the previous sections to formulate evaluation criteria that reflect the contents and interrelations of the different legal goals of the EU ETS. Section 6 concludes.

2. Methodology

Legal objectives are important for four reasons. Firstly, they can provide legitimate reference points for conducting evaluations, as they are the outcomes of established legislative procedures. The extent to which such procedures are participatory and deliberative influences the legitimacy of the legislation produced and the goals enshrined therein.Footnote 18 Secondly, legal objectives result from a political balancing of various, often opposing, interests.Footnote 19 Particularly in a jurisdiction such as the EU, the ordinary legislative procedure of which requires broad agreement among political groups in the European Parliament and among Member States’ ministers in the Council of the EU, the objectives embedded in the law are likely to reflect a comprehensive set of considerations, balanced in the pursuit of political compromise.Footnote 20 Thirdly, legal goals provide a framework that is universally applicable within a jurisdiction and that remains stable until revised by the legislature. This is an advantage compared with policy goals, which can be ephemeral and divergent between different institutions and policy actors. Lastly, goals enshrined in legislation have an objective normative significance, as they drive the implementation of the law, being at the core of the teleological (purpose-driven) method of interpretation applied by courts. Particularly the CJEU has given priority to teleological interpretation over other methods.Footnote 21

Analyzing the objectives and priorities of the law can be valuable in understanding, evaluating, and improving climate policies. Law is an essential tool for mitigating the climate crisis. Making its internal logic explicit and accessible to a non-legal audience can provide a common ground for social dialogue and for regulatory collaboration among various disciplines. Our contribution identifies and analyzes the legal objectives of the EU ETS, by combining legal research methods with complementary insights from economic theory, and subsequently transposes those objectives into evaluation criteria. The resulting framework can be used by lawmakers, policymakers, and researchers at all stages of the policy cycle.Footnote 22 It can help them (i) to evaluate the effectiveness of the EU ETS, namely, its ability to achieve its legal goals; (ii) to critically analyze different proposals to amend the EU ETS; (iii) to highlight possible trade-offs between specific design options; and (iv) to formulate regulatory amendments that align with the legal objectives of the scheme. Moreover, our methodological approach to develop an evaluation framework based on a systematic analysis of goals in the law can be applied to other regulations or jurisdictions, and can guide the selection, definition, and ranking of criteria in decision-making techniques used in policy evaluation, such as multi-criteria analysis.Footnote 23

Using legal objectives as a normative basis for policy evaluations does not prevent the inclusion of additional criteria that are not found in law when they are deemed to be relevant.Footnote 24 However, by requiring additions of such external criteria to be made explicit, the normative basis of formulated assessments becomes more transparent and thus easier to criticize and compare. Similarly, it is entirely acceptable to conduct more focused evaluations that concentrate on a limited set of criteria, provided that the normative foundation and scope of these evaluations are clearly defined.Footnote 25

Our methodological approach can be characterized as ‘law first’, as it prioritizes an analysis of the objectives in the law over other sources of evaluation criteria. It departs from previous endeavours in the emissions trading literature to set evaluation criteria based on guidelines by the Intergovernmental Panel on Climate Change (IPCC).Footnote 26 Interestingly, in these guidelines the IPCC acknowledges that the economic and political science literature ‘does not provide much guidance in terms of determining which evaluation criteria are the most appropriate for an analysis of environmental policy’.Footnote 27 Our approach also departs from formulating criteria based on a general understanding by social scientists, including economists, of ‘how climate mitigation instruments should work’.Footnote 28 Such approaches seem to assume that all jurisdictions share the same objectives, which is not necessarily true.Footnote 29 For example, evaluating the EU ETS and the Chinese National ETS under the same set of criteria would fail to take into account the different climate mitigation goals and priorities of the EU and China, as well as their different institutional and regulatory landscapes. Evaluation frameworks that are tailor-made to the specific objectives of each jurisdiction more closely reflect the bottom-up architecture of international climate law, in which countries set nationally determined contributions (NDCs) in the light of their self-perceived common but differentiated responsibilities and capabilities, as well as development priorities.Footnote 30

To identify the legal objectives of the EU ETS, the first step is to locate provisions in the legislation that set out EU ETS goals. We conduct this exercise with the legal research method of document analysis, a systematic process for reviewing legislative documents to extract information, which can then be organized into categories.Footnote 31 The scope of our analysis includes both the operative provisions and the recitals of the EU ETS Directive – namely, Directive 2003/87/EC and all 17 legal acts that have amended it up to March 2024.Footnote 32

The goals outlined in the legislation are expressed with varying degrees of explicitness.Footnote 33 Depending on the context, terms such as ‘aim’, ‘goal’, ‘objective’, ‘purpose’, and ‘in order to’ may indicate an expression of goals. However, goals may also be formulated in less explicit ways, such as ‘in an economically efficient manner’, which may not be captured by a set of pre-defined keywords. For this reason, it is necessary to go beyond the linguistic formulation and examine the meaning of each provision. We define a goal-expressing provision as a provision that expresses a specific intended outcome in relation to the EU ETS. Thus, we exclude provisions that express generic intended outcomes or refer to instruments other than the EU ETS. Finally, we categorize relevant provisions based on the goal(s) they express. Additional methodological details and a comprehensive list of the sentences identified as expressing goals are available in the Supplementary Material to this article.

3. Legal Analysis of EU ETS Objectives

3.1. Identification of EU ETS Objectives

We have identified 16 EU ETS goals in total, which are presented in a non-structured manner in Figure 1.

Figure 1. Identified EU ETS Objectives

Three of these goals are found within the first sentence of Article 1 of the EU ETS Directive: (a) to promote reductions of GHG emissions (‘emissions reductions’), (b) to do so in a cost-effective manner (‘cost-effectiveness’), and (c) to do so in an economically efficient manner (‘economic efficiency’). These are complemented by 13 goals, each of which may be either (i) additional to the Article 1 objectives, or (ii) constituent, thus serving as a sub-objective, of the Article 1 objectives or of other goals. In Table 1 (in Section 5 below) we classify the identified goals accordingly, based on the findings of our legal and economic analysis.

Table 1. EU ETS Objectives Arranged Based on Their Interrelations

The Supplementary Material to this article lists the legal sources corresponding to each identified objective, facilitating the location of specific provisions of the EU ETS Directive based on expressed goals. Moreover, it aids in tracking the evolution of these goals over time. For instance, the goal of avoiding carbon leakage was not part of the initial Directive 2003/87/EC but was introduced later by Directive 2008/101/EC and subsequent acts.Footnote 34 The fact that goals have not remained static over the years is not surprising as legal changes may reflect not only evolving political priorities and a developing policy environment, but also empirical data and practical experience accumulated from the operation of the EU ETS.

3.2. Interpretation of EU ETS Objectives

A legal interpretation of the objectives enshrined in EU ETS legislation can offer insights into their content and interaction. As in any endeavour to interpret EU law, due care should be given to the interpretive methods of the CJEU:Footnote 35 literal, contextual, and teleological interpretation.Footnote 36 Below we explain each of these methods and apply them to the three goals found in the introductory provision of the EU ETS Directive – emissions reductions, cost-effectiveness, and economic efficiency – while seeking to obtain insights into their relationship with the other identified goals.

Our decision to focus on a limited set of three objectives, rather than all 16 goals, was based on the hypothesis that many of the remaining goals are constituent (sub-goals) of these three objectives enshrined in Article 1 of the EU ETS Directive. This hypothesis was later confirmed by our findings, while two additional objectives were identified: equity and coherence.

Literal interpretation

The starting point of the CJEU methodology is literal interpretation, which focuses on the meaning of words in a text.Footnote 37 Article 1 of the EU ETS Directive reads: ‘This Directive establishes a system for greenhouse gas emission allowance trading within the Union (hereinafter referred to as the ‘EU ETS’) in order to promote reductions of greenhouse gas emissions in a cost-effective and economically efficient manner’. Regarding the emissions reductions objective, it is unclear whether the use of the verb ‘promote’ signals an obligation of conduct or an obligation of result. At first glance, the choice of this verb over a more determinate one like ‘ensure’, which would have clearly indicated an obligation of result, may suggest a degree of uncertainty in relation to the achievement of emissions reductions. Regarding the objectives of cost-effectiveness and economic efficiency, the literal interpretation method offers little guidance. The terms ‘cost-effective’ and ‘economically efficient’ are economic in nature and are not defined in the Directive.

As all different language versions of EU legislation carry equal authenticity,Footnote 38 a literal interpretation also entails a comparison of the English text with other linguistic versions of the EU ETS Directive.Footnote 39 This comparison is crucial to ensure a uniform interpretation of EU law.Footnote 40 Nuances can be observed with regard to the word ‘promote’.Footnote 41 In some language versions the wording is quite similar to the English (‘favoriser’ in French, ‘promuovere’ in Italian, or ‘fomentar’ in Spanish). However, in certain cases, it appears to lean more towards an obligation of conduct (‘work towards’, ‘hinzuwirken’ in German). In others, it leans more towards an obligation of result (‘with a view to / with the aim to reduce’, ‘teneinde … te verminderen’ in Dutch or ‘syftar till … minska’ in Swedish).

Important variations are also noticeable with regard to the sentence ‘in a cost-effective and economically efficient manner’. Different terms are encountered, from ‘cost-efficient’ in German and in Greek (‘kosteneffiziente’ and ‘αποδοτικό από πλɛυράς κόστους’, respectively) to ‘economically effective’ in Swedish and in French (‘ekonomiskt effektivt’ and ‘économiquement efficaces’, respectively). A more divergent formulation can be found in Slovak, namely, ‘in a financially and economically advantageous manner’ (‘finančne a ekonomicky výhodným spôsobom’). The existence of deviations among the various official language versions of the provision requires resorting to two complementary legal methods of interpretation related to its context and purpose: contextual and teleological interpretation.Footnote 42

Contextual interpretation

Contextual interpretation involves the examination of the legislative process that led to the adoption of the provision in question, based on the relevant legislative documents (so-called ‘travaux préparatoires’).Footnote 43 Although the role of travaux préparatoires is more limited compared with other interpretative methods, the CJEU has shown increasing interest in the drafting history of secondary EU legal acts in recent years.Footnote 44

In the initial Commission proposal for the EU ETS, Article 1 did not mention economic efficiency but only cost-effectiveness.Footnote 45 The European Economic and Social Committee (EESC) adopted an opinion on the proposal, in which it submitted its disagreement with the proposed Article 1:

The purpose of this Directive should not be to ‘promote reductions of greenhouse gas emissions in a cost-effective manner’ but to ensure that greenhouse gas emissions are reduced in a manner that is cost-effective and minimises the impact on competitiveness and overall employment in the European Union.Footnote 46

These considerations were reflected in the subsequent position of the European Parliament in proposing the following addition to Article 1:

This Directive establishes a Community greenhouse gas emission allowance trading scheme in order to promote reductions of greenhouse gas emissions in a cost-effective manner. It contributes to fulfilling the commitments of the EU and its Member States more effectively, with the least possible diminution of economic development and employment.Footnote 47

In its amended proposal for the EU ETS Directive, the Commission agreed in principle with the Parliament's amendment but noted that, because of its explanatory nature, a text on minimizing impacts on economic development and employment should be transferred to the recitals.Footnote 48 On that basis, the Council of the EU moved the Parliament's sentence to Recital 5 and replaced it with the concise reference to economic efficiency.Footnote 49 That change was subsequently accepted by the Parliament and has remained in Article 1 ever since: ‘in a cost-effective and economically efficient manner’. Therefore, the drafting history of the Directive shows that the term ‘economically efficient’ in Article 1 is a product of inter-institutional compromise and that it encapsulates the need to minimize impacts on competitiveness, economic development, and employment from the operation of the EU ETS.

Contextual interpretation also examines internally the consistency of the provision in question with other provisions in the legal system (systematic interpretation).Footnote 50 As our analysis focuses on objectives, we follow the Court's frequent practice and intertwine systematic interpretation with teleological interpretation below.Footnote 51

Teleological interpretation

Teleological interpretation examines the provision in question in the light of the relevant overarching objectives that primary EU law pursues.Footnote 52 Articles 11 and 191 to 193 of the Treaty on the Functioning of the European Union (TFEU)Footnote 53 establish the main objectives and principles of EU environmental policy.Footnote 54 The EU ETS Directive and its amending acts have all been adopted based on Article 192(1) TFEU. Legislative action on that basis should aim at a high level of environmental protection, including the promotion of international measures to combat climate change, based on the precautionary, preventive, and polluter pays principles.Footnote 55

Relying on the same legal basis, the EU concluded the Paris Agreement, Footnote 56 the central target of which is to enhance implementation of the United Nations Framework Convention on Climate Change (UNFCCC)Footnote 57 by limiting the increase in global average temperature to well below 2°C and preferably 1.5°C.Footnote 58 In pursuit of this international goal, Regulation (EU) 2021/1119 (European Climate Law) established specific binding emissions reduction targets and a framework to ensure that EU legislation is aligned with a trajectory towards climate neutrality by 2050.Footnote 59

Accordingly, in 2023 many provisions of the EU ETS Directive were amended to achieve the more ambitious target of 62% emissions reductions from ETS sectors by 2030 compared to 2005.Footnote 60 With the addition of an explicit reference to the European Climate Law and Paris Agreement targets in Article 1 of the EU ETS Directive, specific values were provided as to ‘the levels of reductions that are considered scientifically necessary to avoid dangerous climate change’.Footnote 61 Therefore, within this structure of goal-oriented obligations, it appears that the linguistically ambiguous verb ‘promote’ in Article 1 of the EU ETS Directive should be interpreted as an obligation of result rather than as an obligation of conduct, as it aims for a concrete outcome that contributes to the achievement of the EU's domestic and international emissions reduction commitments.Footnote 62

While primary EU law does not provide definitions for cost-effectiveness or economic efficiency, it does require the preparation of EU environmental policy to take into account the potential costs and benefits of action or the lack thereof.Footnote 63 Additional criteria that must be considered are the available scientific-technical data and the environmental conditions across the EU, the economic and social development of the Union as a whole, as well as the balanced development of its different regions.Footnote 64 EU primary law thus establishes high environmental standards but also requires the consideration of economic, social and other equity-related objectives. This multitude of overarching goals is reflected both in the European Climate LawFootnote 65 and in the EU ETS Directive, as shown in Figure 1. The questions of whether there is a legal hierarchy between the various objectives, and how possible tensions and trade-offs among them should be administered, are examined in the following section.

3.3. Hierarchy of EU ETS Objectives

Typically, each secondary EU legal act is characterized by one main or predominant purpose.Footnote 66 The CJEU confirms that the ‘principal and ultimate’ objective of the EU ETS Directive is the substantial reduction of GHG emissions in the Union as a whole, in line with the EU's international climate commitments.Footnote 67 At the same time, the Court points out that the principal objective must be achieved in compliance with certain secondary (sub-)objectives.Footnote 68 These secondary (sub-)goals include, among others, cost-effectiveness and economic efficiency, protecting economic development and employment, preserving the integrity of the internal market and competition, as well as promoting technological improvements.Footnote 69 While the Court accepts that the principal aim of reducing GHG emissions ‘as a whole’ should not be harmed as a result of pursuing secondary goals, it also emphasizes the need to reconcile the former with the latter.Footnote 70

CJEU case law also shows that certain secondary objectives can be more relevant than others, depending on the context and issue at stake. For example, in Germany v. Commission, the Court considered that, in relation to distributing allowances through national allocation plans, the goal of avoiding competitive distortions in the internal market was ‘of particular importance’.Footnote 71 Conversely, in Arcelor, priority was given to the goal of reducing the administrative burden, as it was deemed that the inclusion of an excessive number of installations at the initial stage of the EU ETS could jeopardize its proper implementation.Footnote 72 Thus, while it clearly follows from CJEU case law that emissions reduction is the principal goal of the EU ETS, no fixed legal hierarchy can be established between the various secondary sub-goals.

Generally, when a legal act pursues multiple objectives and a conflict arises between them, or between respective rights or interests, the CJEU applies the general principle of proportionality to strike a balance between mutually contradictory goals.Footnote 73 When reviewing the proportionality of EU acts, the CJEU limits itself to examining whether the measure in question is manifestly inappropriate or disproportionate – namely, whether the legislators made manifest errors, misused their powers or clearly exceeded the bounds of their discretion.Footnote 74 This relatively lenient standard of review stems from the premise that the EU legislature enjoys broad discretion in determining its course of action, particularly when the balancing of complex political, economic, and social considerations is at stake.Footnote 75

In Arcelor, the Court recognized the legislature's broad discretion with regard to the EU ETS amendments in question.Footnote 76 It then delineated the boundaries of that discretion, requiring the legislators to balance conflicting goals on the basis of appropriate objective criteria and by ‘taking into account all the facts and the technical and scientific data available at the time’.Footnote 77 Moreover, the Court asserted that even if the importance of an objective can justify trade-offs with other goals – in that case emissions reductions over economic impacts on certain operators – the legislators are obliged to ‘fully take into account all the interests involved’.Footnote 78 The adopted measure ‘must not produce results that are manifestly less appropriate than those that would be produced by other measures that were also suitable’.Footnote 79

The uncontested primacy of emissions reductions does not mean that EU lawmakers are obliged to prioritize their maximization over any secondary objectives involved when amending the EU ETS.Footnote 80 The legislators are nonetheless procedurally obliged to formulate their choices based on objective criteria, while taking into consideration all relevant interests, facts, and data. Substantively, they may not undermine the principal objective but must also refrain from choices that are manifestly less appropriate (such as vis-à-vis secondary goals) compared with other options that are also suitable for attaining the emissions reductions targets.

4. Economic Analysis of EU ETS Objectives

Legal methods were useful for identifying the goals embedded in the law and for understanding more about their content and interrelationships. Nevertheless, in our ‘law first’ approach, some important aspects remain unclear. The EU ETS Directive does not legally specify how the EU ETS aims to ‘promote’ emissions reductions. Moreover, legal interpretation did not sufficiently delineate the differences between ‘cost-effectiveness’ and ‘economic efficiency’. In fact, the lack of legal definitions for these economic terms has led legal scholars to the assumption that both objectives refer to the same concept of realizing emissions reduction at the lowest cost.Footnote 81 Economists, in contrast, have treated cost-effectiveness as a component of economic efficiency, but without examining the legal context and purpose of the two terms.Footnote 82

The above makes clear that our ‘law first’ approach cannot remain limited to a ‘law only’ approach. In the light of the economic conceptual origins of the EU ETS, the legislators decided to internalize economic goals in the EU ETS Directive.Footnote 83 Accordingly, the CJEU has repeatedly examined and taken into consideration the economic logic of the scheme while confronted with questions of a legal nature.Footnote 84 Thus, we also use insights from economic theory to complement our legal findings and map the internal normative framework of the EU ETS.

4.1. Promotion of Emissions Reductions

Our legal findings suggest that the principal objective of the EU ETS Directive to ‘promote’ emissions reductions refers to the achievement of a 62% reduction in the emissions of the covered sectors by 2030. This target aims to attain the EU climate targets and contribute to the Paris Agreement goals. How can the EU ETS achieve the required emissions reductions?

From an economic perspective, the EU ETS is essentially a cap-and-trade instrument that promotes GHG emissions reductions in two ways. Firstly, it requires companies to cover their emissions with emission certificates, so-called ‘allowances’. By maintaining an absolute and declining cap on the overall supply of allowances, it imposes an absolute and declining limit on the total amount of emissions from the activities that it covers.Footnote 85 Secondly, since allowances are scarce and freely tradeable, the economic externality of GHG emissions is partly or wholly internalized at a price determined by the supply and demand of allowances in the market. This makes emissions-intensive activities more expensive, creating an economic incentive to switch towards less emitting technologies and practices.Footnote 86

However, empirical evidence suggests that carbon pricing does not necessarily induce the technological change needed for deep decarbonization, for instance, as a result of relatively low carbon prices, myopic behaviour by market participants, and technological lock-in.Footnote 87 The principal emissions reduction function of the EU ETS is thus undertaken by the progressive decline of the emissions cap, which strengthens the price signal as allowances in the market become more scarce.Footnote 88 Accordingly, a significant allowance surplus, like the one that accumulated in the EU ETS, not only depresses the allowance price but could also jeopardize the timely achievement of the emissions reduction target, if not addressed.Footnote 89 Since 2019, a Market Stability Reserve has operated within the EU ETS to automatically reduce the allowance auction volume in the event of an allowance surplus and invalidate a share of these excess allowances.Footnote 90

Therefore, the economic logic of the EU ETS Directive suggests that the ‘promotion’ of GHG emissions reductions refers to an aggregate reduction of emissions from covered activities because of a progressive decrease of allowances available in the market. Similar to a waterbed, certain companies or sectors under the EU ETS can emit more as long as other covered companies or sectors emit less.Footnote 91 As a consequence, the inclusion of a new sector in the EU ETS does not ensure that emissions within that particular sector will be reduced in the short to medium term. Nevertheless, certain in-sector emissions reductions may still be incentivized by the carbon price, and all sectors will eventually need to decarbonize in the long run, as the cap will be gradually tightened to zero. Outside its covered sectors, the EU ETS may also ‘promote’ emissions reductions in a broader sense. Examples include the use of auctioning revenues for financing climate actions within and beyond the EU,Footnote 92 as well as the propagation of ETS-induced technological innovations and the diffusion of carbon pricing policies in third countries.Footnote 93

4.2. Cost-effectiveness and Economic Efficiency

Although our legal analysis showed that cost-effectiveness and economic efficiency are among the secondary objectives of the EU ETS Directive, these terms are not defined in the law. In economics, a general definition of cost-effectiveness is ‘the achievement of results in the most economical way’, while economic efficiency can be understood as a ‘general term for making the maximum use of available resources’.Footnote 94 Economic efficiency can broadly be distinguished between productive efficiency and allocative efficiency.Footnote 95 Productive (or technical) efficiency is achieved when an organization produces its outputs at minimum average cost.Footnote 96 Allocative efficiency refers more broadly to the optimal allocation of resources in a society, such as in a manner that maximizes utility for consumers.Footnote 97

In the context of environmental policy instruments, Mickwitz makes a similar distinction between economic efficiency interpreted as cost-effectiveness and economic efficiency with the meaning of a cost-benefit analysis (CBA).Footnote 98 On the one hand, cost-effectiveness focuses on whether the same environmental result could have been achieved with fewer economic resources, similarly to productive efficiency.Footnote 99 On the other hand, the CBA variation of economic efficiency requires a comparison between the overall benefits and costs of an environmental instrument, resembling the notion of allocative efficiency.Footnote 100

In the light of the above, cost-effectiveness in the EU ETS can be perceived as the realization of its emissions reduction target at the lowest possible cost. Cost-effectiveness is attained by the tradeable nature of emissions allowances, which equalizes marginal abatement costs across emissions sources covered by the scheme, as the market discovers the cheapest options for reducing each additional ton of emissions.Footnote 101 Under theoretical perfect market conditions, the allowance price equals these marginal abatement costs.Footnote 102 However, in reality, various market or regulatory imperfections can distort the price signal and have a negative impact on cost-effectiveness.Footnote 103 Moreover, the actual cost of realizing the emissions target under the EU ETS is increased on account of transaction costs.Footnote 104 These include additional costs incurred by companies in complying with the scheme, such as reporting their emissions and organizing allowance transactions, as well as costs incurred by government agencies in administering it, such as maintaining the allowance registry and monitoring compliance.Footnote 105 An assessment of the cost-effectiveness of the EU ETS should thus include the sum of the above-mentioned abatement and transaction costs in a given period. This sum can be labelled as ‘partial equilibrium’ costs, as the scope of a relevant economic assessment is limited to the emissions trading market without extending to other parts of the economy.Footnote 106

Conversely, economic efficiency implies an assessment of the overall benefits and costs that the EU ETS entails for society. The scope of this exercise is broader compared with assessing cost-effectiveness, as it is not limited to the emissions trading market (partial equilibrium) but also encompasses the interaction of the ETS with other markets in the economy (general equilibrium).Footnote 107 The main societal benefits of the EU ETS stem from the reduction of GHG emissions, and thus from the avoidance of the damage that the abated emissions would have imposed on society. The quantification of these types of damage and their corresponding abatement benefits remains controversial, as different methodological choices and assumptions have led to widely divergent, albeit increasing, estimates of the social cost of carbon.Footnote 108 Additional ETS benefits can potentially arise from the use of allowance auctioning revenues, positive effects of carbon pricing on innovation, and co-benefits for the environment, public health, energy security, and employment.Footnote 109 On the other side of the equation, the costs of the EU ETS consist of partial equilibrium costs, as discussed above, as well as general equilibrium costs. The latter encompass potential economy-wide effects, such as competitive distortions and impacts on production levels, employment or international competitiveness in emissions-intensive sectors, which could eventually have a negative influence on gross domestic product (GDP).Footnote 110

Several references in the European Commission's impact assessments are aligned with the distinction of the terms presented above – namely, cost-effectiveness as the minimization of the costs of meeting the declining emissions cap of the EU ETS (partial equilibrium), and economic efficiency as the maximization of the net benefits of the EU ETS to society (general equilibrium).Footnote 111 Our legal interpretation that the term ‘economic efficiency’ was aimed at minimizing potential impacts on competitiveness, economic development, and employment also fits this definition. With all other factors held constant, a reduction of such impacts increases the net benefits of the EU ETS to society.

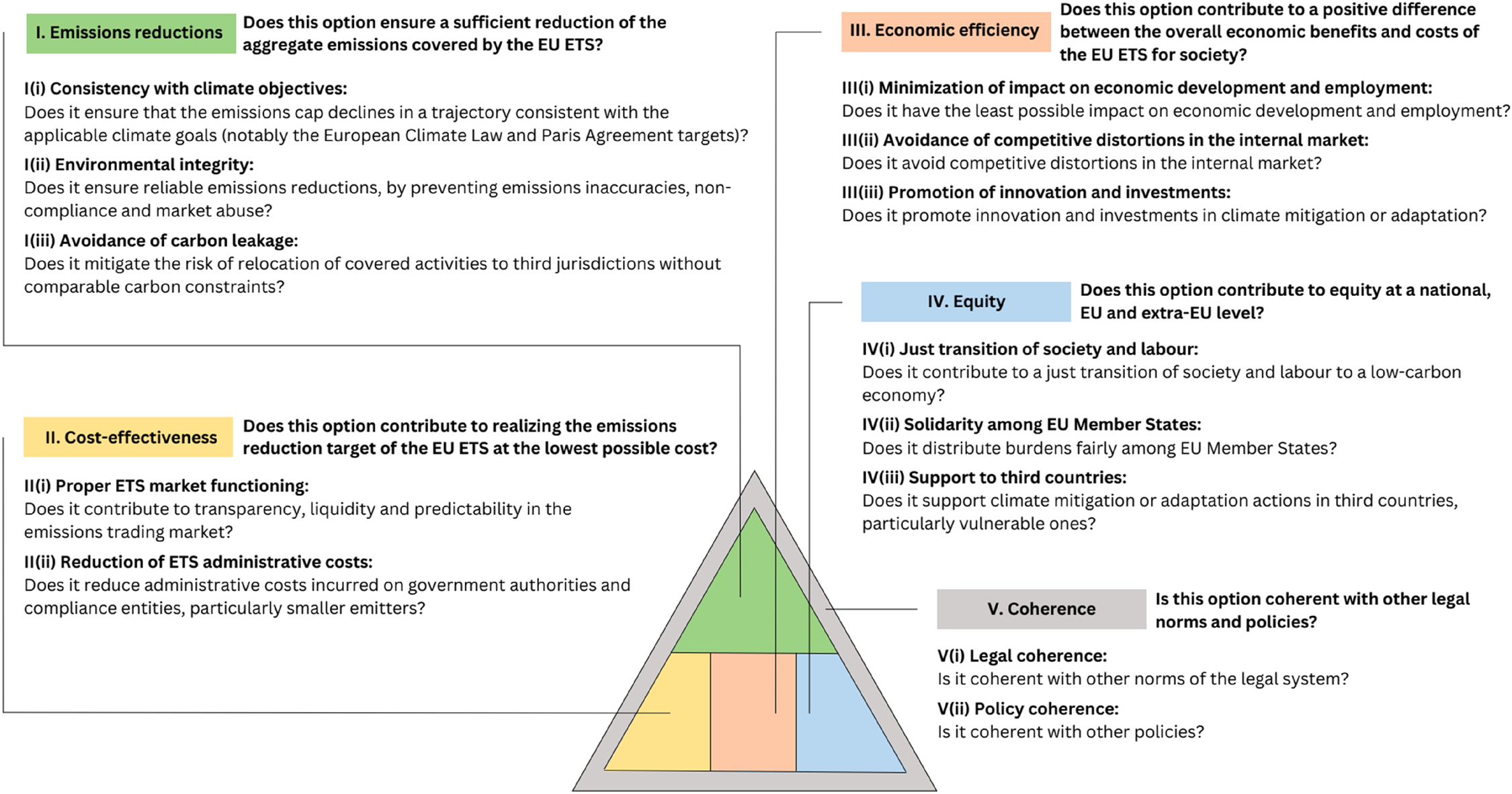

5. Transposition of EU ETS Objectives into Evaluation Criteria

To make the EU ETS goals usable for evaluation, they need to take the form of specific criteria. The first step is to arrange the identified goals in a manner that expresses their interrelations – namely, their legal hierarchy and their functional relationships. The second step is to formulate evaluation criteria and sub-criteria that encapsulate the legal contents of the resulting goals and sub-goals.

Based on the findings of our law and economics analysis, Table 1 structures the goals that were presented in Figure 1 into sets of objectives and sub-objectives. Following the basic-level categorization approach, we form categories by grouping goals according to their functional similarities and differences.Footnote 112 Specifically, each objective in Table 1 is expressed as a category which includes sub-objectives that share the highest degree of common functions within that category and, at the same time, the lowest degree of common functions with sub-objectives from other categories.Footnote 113 This categorization approach can cater for the fact that, in many cases, EU ETS goals are not functionally distinct and independent from each other.Footnote 114 Some sub-objectives are linked to more than one objective: carbon leakage, for instance, can affect both emissions reduction and economic efficiency. It is beyond the scope of the present analysis to provide exhaustive definitions of the identified goals and their interlinkages. Below we explain the functional relationship between each objective and its sub-objectives, while highlighting some indicative examples of interaction between different goals.

From the 16 EU ETS goals identified in the law, five main objectives are deduced: (i) emissions reductions, (ii) cost-effectiveness, (iii) economic efficiency, (iv) equity, and (v) coherence. The reduction of emissions is the principal objective of the scheme, while no fixed legal hierarchy is established among the secondary goals of cost-effectiveness, economic efficiency, and equity. As explained below, we use the term ‘equity’ to describe the secondary goal that comprises three identified sub-objectives, which pertain to distributional aspects of the EU ETS – namely, just transition, solidarity among Member States, and support for third countries.Footnote 115 Coherence is hereby labelled as a ‘meta-objective’, meaning that it is not part of the hierarchy of objectives but refers to the interaction between objectives, on the one hand, and other norms of the legal system and other policies, on the other.Footnote 116 Below we highlight that the extent to which an EU ETS objective should be aligned with another norm or policy depends on the nature of the norm or policy in question.

Emissions reductions by the EU ETS must be (i) consistent with the broader EU and international climate objectives. This sub-objective refers to the consistency of the EU ETS cap and its reduction trajectory with the emissions targets set by the European Climate Law and the Paris Agreement goals. Consideration should also be given to the parallel sectoral targets and processes for international aviation and shipping at the International Civil Aviation Organization (ICAO) and the International Maritime Organization (IMO), respectively.Footnote 117 A precondition for achieving the required emissions reductions is (ii) environmental integrity, which encompasses the need for accurate emissions accounting and prevention of non-compliance and abuse.Footnote 118 Finally, the emissions reductions objective of the EU ETS can be compromised if companies circumvent its emissions cap by relocating to third jurisdictions with laxer climate policies, referred to as carbon leakage.Footnote 119 This risk also raises considerations of economic efficiency, in so far as the relocation of companies can have an impact on economic development and employment in the EU.Footnote 120 The sub-goal of (iii) avoiding carbon leakage has so far been pursued mainly with the free allocation of allowances to support the competitiveness of companies highly exposed to that risk and, recently, with the gradual introduction of the EU Carbon Border Adjustment Mechanism (CBAM).Footnote 121

From a strictly economic perspective, cost-effectiveness could be categorized as a sub-objective of the broader notion of economic efficiency. Nevertheless, it follows from CJEU case law that where the co-legislators ‘have departed from the proposal of the Commission, the resulting EU act may not be interpreted in a way which runs counter to such departure’.Footnote 122 Therefore, cost-effectiveness and economic efficiency are categorized in the internal normative framework as separate secondary objectives, as the latter was not included in the initial Commission proposal but was introduced by the co-legislators. Cost-effectiveness, on the one hand, encompasses the ‘partial equilibrium’ sub-objectives of (i) ensuring the proper functioning (namely, the transparency, liquidity and predictability) of the emissions trading market, and (ii) reducing ETS administrative (transaction) costs.Footnote 123 On the other hand, economic efficiency encompasses the ‘general equilibrium’ sub-objectives of (i) minimizing the impact on economic development and employment, (ii) avoiding competitive distortions (ensuring a level playing field) in the EU internal market, and (iii) promoting innovation and investments.Footnote 124 The latter sub-objective is also intertwined with cost-effectiveness, as the dynamic incentives created by the EU ETS can induce the development and deployment of technologies that can subsequently lower the cost of meeting the emissions reduction target.Footnote 125

The secondary objective of equity pertains to the fact that even when the overall economic benefits of a regulation exceed its costs, the distribution of these benefits and costs is typically uneven among different parts of society or different countries.Footnote 126 Such distributional consequences can be evaluated and addressed on the normative basis of various equity theories, as developed by political philosophers and economists among others, to gauge which inequalities are unfair.Footnote 127 The EU ETS Directive enshrines three sub-goals in relation to three different governance levels of equity: (i) just transition of society and labour (national level), (ii) solidarity among EU Member States (EU level), and (iii) support for third countries beyond the EU (extra-EU level).Footnote 128 The use of ETS auctioning revenues is an instrument for addressing such distributional aspects.Footnote 129

Lastly, the (meta-)objective of coherence consists of the (i) ‘inward-looking’ sub-objective of maintaining coherence between the norms of the legal system, and the (ii) ‘outward-looking’ sub-objective of optimizing interaction between policies. On the one hand, legal coherence essentially means that the legal system should function as a consistent whole and that the hierarchy of norms must be observed.Footnote 130 The systematic and teleological methods of interpretation introduced in Section 3 are founded upon this meta-objective.Footnote 131 Accordingly, as secondary EU legislation, the EU ETS Directive and its objectives must avoid conflicting with other norms of secondary EU law and conform with hierarchically superior norms of primary EU law and international law.Footnote 132 As explained in Section 3.3, the principle of proportionality is applied by the CJEU as a balancing tool for resolving conflicts between objectives, thereby contributing to legal coherence.

On the other hand, policy coherence is attained by avoiding conflicts or undesirable effects,Footnote 133 and by pursuing synergiesFootnote 134 between the EU ETS and other policies.Footnote 135 Relevant policies may be implemented at Member State level (such as national carbon taxes),Footnote 136 at the EU level (such as energy security or broader environmental policies),Footnote 137 or at an extra-EU level (such as policies adopted by other jurisdictions beyond the EU or by international organizations).Footnote 138 The difference between legal and policy coherence is that the former concerns legal norms whereas the latter refers to actual effects from policy interaction. As policies are often implemented through law, the two sub-goals can overlap to the extent that policies also create norms that become part of the EU legal order.

In Figure 2 we formulate evaluation criteria and sub-criteria that reflect the respective objectives and sub-objectives of the EU ETS. The formulation of criteria as questions facilitates their practical application in evaluations of the EU ETS and its amendments.Footnote 139

Figure 2. Evaluation Criteria Based on the EU ETS Objectives

6. Conclusion

The EU ETS carries a substantial and increasing share of the EU's effort to become climate neutral by 2050. Criteria that align with the objectives embedded in the EU ETS legislation are essential for enabling more effective evaluations and reforms of the scheme in the crucial years ahead. By systematically mapping and analyzing its multiple legal goals, we made a first attempt to map the internal normative framework of the EU ETS and formulate evaluation criteria that reflect the content and interrelations of these internal objectives. This process has also helped to shed light on persisting ambiguities about the fundamentals of the EU ETS.

Our analysis shows that the scheme pursues a diverse and nuanced set of objectives that go beyond those outlined in Article 1 of the EU ETS Directive. The principal goal among them is the reduction of the aggregate GHG emissions covered by the scheme, which needs to be balanced with the three secondary objectives of cost-effectiveness, economic efficiency, and equity. The EU legislators enjoy a broad but limited margin of political discretion in this balancing process, subject to a high-threshold proportionality check by the CJEU. They also need to ensure that their legislative choices are coherent with other applicable legal norms and relevant policies.

Policy evaluations often assign different weights to selected criteria, based on a perception of their normative ranking. For instance, Konidari and Mavrakis determine weight coefficients based on the expressed preferences of certain stakeholder groups.Footnote 140 Our article does not follow that approach because the internal normative framework of the EU ETS classifies emissions reduction as its principal objective but does not establish a fixed ranking between the rest of its goals. Users of our evaluation framework can complement its criteria with weighting factors while making clear that these weights constitute external normative elements. Likewise, they may complement it with additional external criteria, such as that of ‘political feasibility’, which is commonly encountered in past evaluations.Footnote 141

Our contribution lays the foundations for further research into the internal normative framework of the EU ETS and the legal interpretation of its multiple (sub-)goals. In particular, the objectives of equity and coherence have received relatively limited attention so far, but are becoming increasingly relevant. As the emissions cap declines further, allowance prices are projected to rise,Footnote 142 which can amplify negative distributional impacts. At the same time, the expanding scope of the EU ETS is accompanied by an increasing need to maintain consistency with other applicable norms and policies. Researchers and policymakers could refine the qualitative evaluation criteria developed in this article, and transpose them into quantitative metrics suitable for conducting economic modelling exercises. Future research can also apply the interdisciplinary methodology of our contribution to construct evaluation frameworks for other policy instruments or jurisdictions, based on analyses of the objectives enshrined in their respective laws.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/S2047102524000153.

Acknowledgements

We wish to thank the attendees of the 14th Annual Meeting of the Society for Environmental Law and Economics (SELE) at the University of Cambridge (Cambridge, United Kingdom) for their feedback on our paper presentation, especially Arden Rowell. We are also grateful to our colleagues at the Groningen Centre of Energy Law and Sustainability (GCELS), Groningen (The Netherlands), for their suggestions and for helping us to translate different language versions of the EU ETS Directive. Moreover, we wish to thank Frans Nelissen and Lorenzo Squintani for their comments on an earlier version of the manuscript. Lastly, our article has been improved thanks to the excellent remarks of three anonymous TEL reviewers.

Funding statement

Not applicable.

Competing interests

The authors declare none.

Open access

Open access