In mid-2007 in the United States, well before the failure of Bear Sterns, clear signs of banking distress were already evident. The housing market was declining and investment funds, both international and domestic, were losing billions of dollars. One of the nations’ largest mortgage lenders had just gone bankrupt,Footnote 1 following the recent trend set by the bankruptcies of several of Bear Stearns’s investment funds in July. The “TED Spread,” an indicator of financial instability,Footnote 2 was at high levels not seen since the bursting of the Dot-Com bubble that had sparked the 2001 US recession. And France’s largest bank, BNP Paribas, would soon cease honoring investor withdrawal requests from its main housing-backed investment funds, sparking a crisis of confidence and the early stages of the liquidity crisis. Even amidst this financial turbulence, the Federal Reserve decided to refrain from monetary easing, partly given that oil prices had recently “pushed overall inflation … uncomfortably high” (Bernanke Reference Bernanke2015). While the Fed then cut the federal funds rate at its September meeting, to go along with new lending facilities to address the incipient liquidity pressures, in the Fed’s October meeting the committee again lowered rates but noted that it was “a very, very close call,” given that “inflation was a concern.” Additionally, as Bernanke notes in his memoirs, he agreed to language in the committee’s press release that indicated they were not eager for additional rate cuts unless the data showed a clear weakening in the inflation rate.

Internationally, Governor Mervyn King, a prototypical conservative central banker primarily concerned with maintaining low inflation, criticized his international peers for these policies.Footnote 3 Meanwhile, even after the Fed had begun rate reductions, the European Central Bank (ECB; whose level of central bank independence [CBI] scholars consider very high, in the 95th percentile) actually increased interest rates and didn’t begin monetary easing until after the collapse of Lehman brothers.Footnote 4 Later, even after the European debt crisis was in full swing, the ECB again raised interest rates multiple times before eventually realizing the need to be more aggressive in combating the decline in growth (Frieden and Walter Reference Frieden and Walter2017).

These examples demonstrate the central importance regarding the role of CBI in the modern economy. As economic first responders, these institutions, either via action or inaction, have a substantial influence on the degree of joblessness and economic insecurity in a country in addition to shaping the political aftershocks from poorly managed crises (Bartels and Bermeo Reference Bartels and Bermeo2014; Fetzer Reference Fetzer2019). Such destabilizing episodes raise fundamental questions about the democratic legitimacy and adequacy of governmental delegation to quasi-independent economic institutions (Aklin and Kern Reference Aklin and Kern2021; Dietsch Reference Dietsch2020), calling into question a basic framework to prevent political manipulation of essential functions. Notably, while extant monetary theory suggests that CBI should enhance the management of economic crises (Adolph Reference Adolph2013; Bodea Reference Bodea2014; Diamond and Rajan Reference Diamond and Rajan2012; Yildirim-Karaman Reference Yildirim-Karaman2017), these cases demonstrate how CBI, which incentivizes a strong focus on inflationary objectives, may actually be a significant hindrance to effective crisis management.

Along these lines, I argue that banking crises under high CBI (with its inflation-centric focus) will produce more severe economic outcomes. Although the literature has long considered CBI to be virtually without meaningful costs (Garriga and Rodriguez Reference Garriga and Rodriguez2020; Grilli et al. Reference Grilli, Masciandaro, Tabellini, Malinvaud and Pagano1991), I demonstrate that there are substantial trade-offs in establishing very high levels of CBI. However, I also show that these negative trade-offs can be balanced, potentially achieving inflation stability, without having to sacrifice financial stability at the same time. This is possible by preserving some aspects of CBI, such as restrictions on political dismissals of central bank governors (what is called political independence), which remain essential to prevent electorally minded governments from demanding inflationary policies from the central bank. On the other hand, I argue that inflation-centric bank mandates (classically considered part of CBI) are unnecessary to stabilize inflation while also inducing central bankers to be too cautious in responding to banking crises, which manifests as larger economic shocks.

Using country fixed effects panel models spanning from 1970 to 2012 for up to 142 countries, I show that banking crises under high levels of CBI lead to larger unemployment shocks and larger credit and stock market contractions. At the same time, banking crises lead to less severe outcomes for banks that do not hierarchically prioritize inflation or possess what I simply refer to as an “employment mandate.” I demonstrate that central banks with employment mandates also lead to lower real interest rates, illustrating the monetary transmission from the central bank. Importantly, I also assess whether employment mandates incur the inflation feared by the early literature (Herrendorf and Lockwood Reference Herrendorf and Lockwood1997; Lohmann Reference Lohmann1992; Rogoff Reference Rogoff1985) and find that they do not, and thus appear to be a more flexible central banking design. These results are robust to using an instrumental variable approach as well as employing an inverse probability of treatment weighting estimator (Benguria and Taylor Reference Benguria and Taylor2020; Creamer and Simmons Reference Creamer and Simmons2019) to deal with potential bias arising from the onset of crises.

The paper offers a significant contribution in several ways. First, the strong consensus regarding CBI has long been that it is a universally positive institution with little in the way of costs. Although recent literature questions CBI in a general sense (Aklin and Kern Reference Aklin and Kern2021; Dietsch Reference Dietsch2020; Jones and Matthijs Reference Jones and Matthijs2019), scholars demonstrating directly adverse effects from CBI are virtually nonexistent. In this case, I show that CBI strongly shapes the outcomes of arguably the most politically destabilizing events in the global economy—banking crises. Additionally, it has long been considered paramount to enshrine inflation-centric mandates into central bank charters in order to effectively constrain liberal central bankers. So central is this concept that indices of CBI code inflation-centric mandates as granting more independence to the bank, and the clear majority of central banks worldwide now give clear priority to inflation. This is the first paper, to my knowledge, to demonstrate that this design offers no clear inflation gainsFootnote 5 while leading adversely to worse management of economic shocks. Therefore, it can no longer be taken as a given that higher CBI necessarily leads to more positive outcomes, and it encourages a serious rethinking of how to achieve optimal delegation for this important economic institution.

Central Bank Independence and Macroeconomic Outcomes

The literature on CBI is voluminous, and scholarly consensus has revolved around the idea that it is effective not only at preventing bad outcomes like inflation, debt crises, or exchange rate instability (Cukierman Reference Cukierman1992; Dincer and Eichengreen Reference Dincer and Eichengreen2007; Reference Dincer and Eichengreen2009; Garriga and Rodriguez Reference Garriga and Rodriguez2020; Keefer and Stasavage Reference Keefer and Stasavage2003) but also in actively fostering positive financial outcomes. For instance, recent work establishes that CBI not only reduces risk but also improves government credit outcomes and attracts foreign direct investment (Bodea and Hicks Reference Bodea and Hicks2015; Reference Bodea and Hicks2018). Generally speaking, scholars have often upheld Grilli et al. (Reference Grilli, Masciandaro, Tabellini, Malinvaud and Pagano1991) when they famously declared CBI to be a “free lunch” because it appeared to reduce inflation but without significant costs to the economy.

In addition to these gains, a subset of the literature examines gains to the economy that arise from CBI’s role as a credible commitment device. Specifically, scholars have examined whether CBI has led to smaller economic adjustment costs in periods of inflation stabilization.Footnote 6 Given that fighting high levels of inflation is economically costly, scholars have studied such cases by measuring the amount of economic output or employment (Cukierman Reference Cukierman2002; Stasavage Reference Stasavage2003) lost during the stabilization period in what is called the “sacrifice ratio” (Ball Reference Ball1994; Daniels, Nourzad, and VanHoose Reference Daniels, Nourzad and VanHoose2005; Mazumder Reference Mazumder2014).

The literature in general has argued that CBI, because of its credibility premium to monetary policy, should result in lower sacrifice ratios. This is because inflation is partly a function of policy expectations (Drazen Reference Drazen2002; Kydland and Prescott Reference Kydland and Prescott1977; Rogoff Reference Rogoff1985) such that when high interest rates (which increase unemployment) are necessary to fight inflation, public belief in the resolve of the monetary authority in fighting inflation will hasten a more rapid decline in wage demands and will thus achieve the inflation target with less economic adjustment pain. Thus, CBI should be beneficial—translating into lower employment or output costs. Although there have been some mixed findings in this literature (Caporale and Caporale Reference Caporale and Caporale2008; Katayama, Ponomareva, and Sharma Reference Katayama, Ponomareva and Sharma2011), more recent evidence has suggested smaller sacrifice ratios for non-OECD countries due to its “credibility bonus” (Mazumder Reference Mazumder2014) or for banks with greater transparency (Dincer and Eichengreen Reference Dincer and Eichengreen2007; Reference Dincer and Eichengreen2009; Stasavage Reference Stasavage2003).

Given the same credibility effect inherent in analyses of sacrifice ratios, it is also well established that in principle CBI should also give more policy space in order to combat recessionary pressures or cyclical downturns (Adolph Reference Adolph2013; Bodea Reference Bodea2014). Goodfriend (Reference Goodfriend2007), in using the historical experience of the US Federal Reserve, makes this explicit argument in terms of how the Fed established its anti-inflationary credibility. After several bouts of “inflation scares,” where monetary easing stimulated shocks to long-term interest rates due to heightened inflation expectations, Goodfriend argues that once the Fed achieved its credibility by the 1990s the Fed could respond to unemployment with much more substantial reductions in the federal funds rate, minimizing employment losses. The credibility of the central bank’s commitment, in this way, “improves the flexibility for monetary policy to stabilize employment over the business cycle” (Goodfriend Reference Goodfriend2007, 56). In his memoirs, Alan Greenspan referred to this as the Fed achieving a “soft landing”—having used more aggressive easing in light of their hard-won credibility, the effects of the downturn were minimal. Such reasoning is broadly shared and often is incorporated in formal modeling of monetary policy by prominent central bankers (Diamond and Rajan Reference Diamond and Rajan2012). An important implication is thus that CBI should in fact lead to more favorable outcomes during recessions or extreme events such as banking crises. However, existing studies on this line of reasoning have focused exclusively on inflation stabilization (a now antiquated problem), and there are no existing studies to the best of my knowledge that examine whether CBI leads to better management of banking crises.

Recent literature has moved closer toward examining the potential harmful consequences of CBI. Aklin and Kern (Reference Aklin and Kern2021), for instance, argue that because CBI limits the ability of the government to direct monetary policy, in addition to constraining their discretion over fiscal spending (Alpanda and Honig Reference Alpanda and Honig2009; Bodea and Higashijima Reference Bodea and Higashijima2017; Keefer and Stasavage Reference Keefer and Stasavage2003), governments liberalize the financial sector when they retain regulatory control, potentially creating a biased regulatory regime. These findings clearly have important implications that merit deeper analysis. At the same time, it suggests the byproduct of CBI may at times be suboptimal but does not demonstrate that CBI itself generates negative consequences. Moreover, the literature on financial development (Rajan and Zingales Reference Rajan and Zingales2001; Reference Rajan and Zingales1998) largely argues that the deregulatory policies discussed by Aklin and Kern can be pro-growth policies, a finding corroborated by Ashraf (Reference Ashraf2017) in showing that a broad spectrum of financial liberalization policies decrease banking sector risk. It is therefore vital to further tease out under what pathways CBI may or may not be a harmful institutional design.

Central Bank Independence, Mandates, and the Consequences of Banking Crises

Given the above discussion, one might predict that CBI would lead to more favorable outcomes during banking crises, as Goodfriend (Reference Goodfriend2007) would imply. This widely presumed and sanguine view is that because CBI generates credibility to fight inflation, independent central banks can more aggressively fight economic downturns such as banking crises or general recessions. Given the credible commitment, substantial monetary easing shouldn’t affect long-run inflation expectations and should remain stable such that monetary easing alleviates unemployment without generating a strong inflationary response.

By contrast, I argue that CBI as currently conceived fails to live up to this potential and instead induces policy rigidity in the face of financial turmoil, exacerbating economic outcomes. In brief, I argue this is because central banking mandates (legislated objectives) that prioritize inflation goals at the exclusion of other economic objectives incentivize a myopic focus on inflation by central bankers such that they are too cautious in responding to banking instability. In this section I will elaborate on this logic, and in the next section I will articulate how CBI can be thought of in parts: what I term “functional independence” or functional CBI, coupled with a legislative mandate that prioritizes employment goals rather than inflation. There, I will argue that employment mandates give central banks important policy leeway that permit them to respond more aggressively to banking shocks, offering a potential redesign of central banking governance that renders them more flexible in the face of crises.

CBI induces inflation myopia, in my view, for three essential reasons. First, as noted, inflation mandates have long been considered a fundamental necessity for central banking design such that they have become increasingly used over time and indices of CBI code such mandates as possessing more independence. Second, monetary theory has advanced tremendously since these inflation mandates were originally promulgated, to the extent that it isn’t plausible that central bankers would revert to the inflationary policies of the 1970s. And third, partly as a consequence of advances in monetary theory, central bankers zealously guard their reputations as inflation fighters and are highly averse to the risk of their credibility being impaired. This last point regarding reputational concerns is especially noteworthy, as it leads inflation mandates to become especially binding on their behavior partially because of market expectations. I will address these in turn.

Monetary Learning and Reputational Concerns

The monetarist revolution in monetary economics (Friedman and Schwartz Reference Friedman and Schwartz1971; Hall and Sargent Reference Hall and Sargent2018; Kydland and Prescott Reference Kydland and Prescott1977) had a transformational effect on the understanding of what can be accomplished with monetary policy such that even liberal central bankers more focused on employment gains understood that employment objectives cannot be realistically achieved unless inflation is low and stable. For instance, McNamara (Reference McNamara1999) argues that the emergent neoliberal consensus in monetary economics led even Communists in Italy and Socialists in France in the 1980s to agree with inflation-centric monetary objectives, which implied enduring higher costs to unemployment and tighter monetary policy, at least over the short run. In short, there was a convergence in understanding in which even liberal economists understood they could not achieve progressive policy objectives unless inflation was stabilized.

This cultural and ideational shift in the policy view means that central bankers in the modern era implicitly elevate inflation performance as crucial and understand that losing a credible reputation for fighting inflation is extremely difficult and economically costly to regain. The profession of central banking thus implicitly values the importance of reputation as inflation fighters and bankers are likely to be highly reactive against threats to this reputation. As a consequence, it seems evident that central bankers are already socialized to prioritize inflation and, even if the central bank charter contained no mandate for inflation, would be unlikely to return to the inflationary policies of the premonetarist revolution era provided they have insulation from political pressure. In essence, one cannot put Milton Friedman back in the bottle (Hall and Sargent Reference Hall and Sargent2018). Central bankers now are likely to set policy in a much more inflation-averse fashion than in the era when the importance of inflation mandates was articulated. This is a crucial point because it implies that inflation mandates would be unnecessary at best and potentially harmful at worst. Inflation mandates may come with little inflationary gain and at the cost of ineffectiveness in the face of crises.

Based on similar reputational reasoning, Ainsley (Reference Ainsley2017) argues that even though central banks with inflation targets typically suggest the target is symmetric—such that inflation above-or-below target is weighted equally—in practice central bankers are much more sensitive to the risk of overshooting the inflation target and consequently use stricter monetary policy than might be necessary to maintain inflation stability. In this way CBI, which prioritizes inflation in the central bank mandate, may induce central bankers to hold especially asymmetric preferences with respect to the inflation target. Historically, reputational motivations have long been paramount with respect to not only inflation but also exchange rate management, which have common implications because low-inflation policies imply the same adverse effects as fixed exchange-rate policies. In the Bretton Woods experience of exchange-rate management, for instance, countries failed to use built-in flexibility mechanisms—exchange-rate adjustments—because they worried that use of adjustments would have weakened the credibility of their exchange-rate commitment (Eichengreen Reference Eichengreen2008b). The result was delayed economic adjustment and likely worse economic outcomes as time passed (Eichengreen Reference Eichengreen2008a; Walter Reference Walter2013).Footnote 7 Simmons’s (Reference Simmons1996) classic work on CBI during the Interwar years and Great Depression is another powerful example of this dynamic. In studying the ability of countries to stay on the gold standard, Simmons found that CBI led to more contractionary policiesFootnote 8 than were actually required to maintain their peg to gold. As a result, these excessively tight monetary policies produced larger contractions and greater increases in unemployment than were actually required, further demonstrating the economic damage that can occur due either to reputational concerns or implicit asymmetric policy preferences. And anecdotally, former Federal Reserve Chair Janet Yellen has suggested that concern over the credibility of the inflation commitment makes her very cautious in evaluating the possibility of raising the Fed’s inflation target, despite compelling evidence that changes in the neutral rate of interest imply a higher inflation target would be optimal.Footnote 9

Economic Implications of Inflation Myopia

For modern times, it must be understood that as a central bank eases interest rates or potentially engages in substantial monetary stimulus such as quantitative easing, this occurs with a potential risk that stabilization today comes at the cost of inflation tomorrow, and the result is that an inflation-averse central bank will exhibit monetary rigidity—easing less due to the long-run concern of inflation. Much as Governor Bernanke was conflicted about responding to the early signs of financial distress in 2007, given that inflation was “uncomfortably” high, independent central banks are likely to maintain higher interest rates in these circumstances until the crisis is severe enough to bring inflation down to the point at which inflation no longer worries the bank. And then, once the most intense phase of financial instability has passed, the inflationary focus induced by CBI may implicitly bind how far the bank is willing to implement stimulus policies. In this stage, doubts about pursuing further stimulus will mount and potentially hasten a premature return to monetary tightening. For instance, once the crisis had passed in the United States, eventual Federal Reserve Governor Nominee Marvin Goodfriend had publicly called for prioritizing inflation and raising rates as early as 2011, when the unemployment rate was still as high as 9% and having only barely come down from its peak. For reference, the Federal Reserve did not begin to raise rates until 2015.Footnote 10 Given that I argue CBI induces an excessive focus on inflation stabilization—given learning in monetary economics, inflation-centric bank mandates, and reputational concerns—we can see that this portends potentially significant adverse consequences for the economy.

It is certainly true that in the most intense, middle phase of a banking crisis, distinctions over monetary preferences may diminish. Yet even if this is the case, strong distinctions in the early and later stages of a crisis would be sufficient to dramatically alter outcomes. Eichengreen (Reference Eichengreen2015), for instance, argues that the Atlanta Fed in the early 1920s averted what could have been a major regional crisis because of rapid and potent emergency stabilization policies. It is commonly argued that China did not experience a major crisis or even recession due to the US financial crisis because of extremely rapid and substantial financial support (Wen and Wu Reference Wen and Wu2019). In other cases, tightening policy too early has led to disastrous consequences and is one reason why many financial crises experience “double dip” recessions (Reinhart and Rogoff Reference Reinhart and Rogoff2014), including the US during the Great Depression (Romer and Romer Reference Romer and Romer2013). As noted, in the evolution of the Euro crisis, it is widely perceived that the ECB amplified the crisis by raising interest rates far too early, forcing them to quickly reverse course (Frieden and Walter Reference Frieden and Walter2017). Consequently, even if policy distinctions may diminish in the most intense crisis stage, hesitancy in the early stages can be sufficient to permit a crisis snowballing effect to take root, and policy distinctions are likely to reemerge in important ways at the back end of a crisis.

What economic outcomes do we expect to observe if in fact CBI amplifies the costs due to banking crises? Because I am implicitly interested in understanding the human toll associated with crises, assessing the unemployment consequences of crises is a meaningful starting point. Much literature has established the political convulsions that arise from unemployment (Fetzer Reference Fetzer2019; Foster and Frieden Reference Foster and Frieden2017; Goodwin and Milazzo Reference Goodwin and Milazzo2017; Hays, Lim, and Spoon Reference Hays, Lim and Spoon2019; Mansfield, Mutz, and Brackbill Reference Mansfield, Mutz and Brackbill2019; Norris and Inglehart Reference Norris and Inglehart2019), thus centering its importance in understanding the consequences of imprudent governance design. Beyond this reasoning, studies of monetary policy have long focused on its influence on unemployment, recalling that some “sacrifice ratios” explicitly measured the number of jobs lost in stabilizing inflation. A recent example is Stockhammer and Sturn (Reference Stockhammer and Sturn2011), who study how an expansive monetary stimulus during recessions can alleviate unemployment hysteresis, or Blanchard and Galí (Reference Blanchard and Galí2010) who study the unemployment consequences for central banks caught between unemployment and inflation stabilization objectives. If CBI induces tepid responsiveness to the onset of banking crises, this should manifest in terms of less monetary easing, higher relative interest rates, and a decline in investment and business spending. Consequently, if CBI amplifies crises because of inflationary concerns, standard monetary theory leads to the prediction that banking crises would lead to higher unemployment shocks when the level of CBI is high.

H1: Banking crises produce larger unemployment increases when CBI is high.

To illuminate the role of central banking, I also examine financial pathways that are known to be highly reactive to monetary policy decisions. Two prominent examples are changes in lending behavior and the reaction of stock markets to monetary policy decisions. Lending by and borrowing from banks has long been considered a transmission mechanism of monetary policy in what is called the bank lending channel (Ippolito, Ozdagli, and Perez-Orive Reference Ippolito, Ozdagli and Perez-Orive2018; Matousek and Sarantis Reference Matousek and Sarantis2009). When central banks restrain from monetary easing especially during negative shocks like banking crises, uncertainty rises (which dampens investment) and without an extra expansion of the money supply, interest rates remain elevated, weakening lending and borrowing incentives. This is especially salient during economic contractions, when economic conditions and financial markets are more sensitive to interest rate changes and when asymmetric information problems are influential. Evidence suggests that stock market and lending contractions will be larger in such contexts (Correia et al. Reference Correia, Farhi, Nicolini and Teles2013; Kulish, Morley, and Robinson Reference Kulish, Morley and Robinson2017; Wu and Xia Reference Wu and Xia2016). Higher interest rates have also been shown to have sizable negative effects when the volume of lending has been large (as would be common in a precrisis lending boom). Examining lending contractions is thus a natural outflow in studying the role of CBI in its amplifying effect of banking crises.

H2: Banking crises produce larger credit contractions (decreases in credit) when CBI is high.

Bank lending can also work by way of the “balance sheet” channel, which predicts that monetary easing expands company stock pricesFootnote 11 and incentivizes additional investment spending (which increases the demand for loans). The balance sheet channel thus offers an intersection between H2 and H3, because monetary easing is expected to both expand lending and boost asset prices such as stocks. Consequently, we should also observe larger stock market contractions if banking crises emerge and the central bank has eased policy less due to institutional design. Existing literature corroborates that stocks are often highly reactive to monetary policy announcements (Bohl, Siklos, and Sondermann Reference Bohl, Siklos and Sondermann2008; D’Amico and Farka Reference D’Amico and Farka2011; Hussain Reference Hussain2011; Papadamou, Sidiropoulos, and Spyromitros Reference Papadamou, Sidiropoulos and Spyromitros2017). This expectation is further validated with historical experience in that the Fed is considered to have “popped” the stock market bubble with interest rate increases in 1929 at the onset of the Great Depression (Friedman and Schwartz Reference Friedman and Schwartz1971; Meltzer Reference Meltzer2002).

H3: Banking crises produce larger contractions in the stock market when CBI is high.

Central Bank Mandates—Why Employment Mandates May Be Superior to Inflation Mandates

Some central banks such as the ECB or the Reserve Bank of New Zealand contain what are called “inflation only” mandates, where the only explicit objective legislated to the bank is price stability. On the other hand, the Federal Reserve exemplifies a common example of a CB (central bank) with competing objectives in which there is a “dual mandate” to stabilize prices while at the same time pursuing maximum employment. Because dual mandates create tension between fighting inflation and pursuing low unemployment, it has long been thought necessary to constrain the freedom of central bankers by giving them explicit inflation mandatesFootnote 12 (Kydland and Prescott Reference Kydland and Prescott1977; Rogoff Reference Rogoff1985; Herrendorf and Lockwood Reference Herrendorf and Lockwood1997). This is why central bank mandates giving equal or greater priority to employmentFootnote 13 have been declining over time, as can be seen in Appendix Figure A0.

In contrast to this established literature, I argue that inflation-centric mandates are excessive to the task of maintaining price stability when the CB is sufficiently independent in other areas. In essence, CBI should be considered as two components: “Functional CBI” (FCBI) and its economic mandate. Classical CBI aggregates both into a single index, though I argue it is useful to split these conceptually. Functional CBI refers to aspects of CB design such as political independence (protections against arbitrary dismissal), policy independence (the government has no policy vote), and limits on lending to the government (to forestall inflationary finance). Each of these in principle should be essential to preserving the ability of central bankers to refrain from politically induced policy making. At low levels of FCBI, mandates shouldn’t matter especially during a banking crisis because central bank activity will simply be absorbed by the governments’ objectives. Consequently, we should expect to see variation on mandates at higher levels of FCBI such that central bankers are insulated from politics but are still conditioned by the mandate. Because I argue that inflation mandates are redundant, given modern understanding of monetary theory, high levels of FCBI should be sufficient to generate inflation stability but management of banking crises will be constrained if the mandate induces elevated reputational costs surrounding inflation objectives. Thus, high FCBI with employment mandates may render the CB more flexible in the face of incipient financial disruptions without incurring higher inflationary costs.

It is important to be clear about the potential costs to a central bank if the bank is perceived to have deviated from its mandate. If central bankers respond to unemployment increases and it is clear that inflation is near target, then markets might anticipate that the central bank will permit long-run inflation to rise. How costly this might be would depend on how convinced markets previously were of the central banks’ commitment to low inflation relative to employment goals, which is partly a function of its mandate. In the presence of an inflation-centric mandate, the potential reputational costs would be larger, in which case uncertainty would increase and long-run interest rates would rise more substantially. Mandates in this way coordinate market expectations by generating focal points such that deviations from expectations should generate significant market corrections. Given that modern central bankers already value low inflation, inflation-centric mandates may unnecessarily escalate the potential reputational costs associated with more aggressively responding to unemployment shocks.

Therefore, in order to forestall risks to the banks’ reputation, inflation is likely to be too heavily weighted because the involved costs are larger and markets have locked them in with expectations. The result would be that they are too slow to respond to financial disruptions and too quick to tighten policy. Romer and Romer (Reference Romer and Romer2013) note that in the middle of the Great Depression, the Federal Reserve doubled reserve requirements (a contractionary policy that may have caused the double-dip recession), which was “motivated by fear of inflation in a still-depressed economy.” In a formal model, Woodford (Reference Woodford2012) similarly demonstrates that inflation targeting entails risks to the financial sector and stresses the need for a flexible policy approach. And in a working paper examining the fiscal costs of crises, Gandrud and Hallerberg (Reference Gandrud and Hallerberg2016) suggest from interviews that the independent South African Reserve Bank—which has an inflation-only mandate—felt restricted from providing liquidity assistance to prevent the failure of a large bank partly due to “strong incentives from its mandate.” Due to these concerns, Reis (Reference Reis2013, 24) suggests that the worst economic outcomes arise from neglecting output or employment effects and thus that “including some measure … like employment, in the objective function of the central bank” would be optimal. Consequently, I argue that inflation-centric mandates lead to monetary rigidity and that this exacerbates the costs of banking crises. Employment mandates (the inverse of inflation-centric mandates), when combined with high functional independence (FCBI), should provide the most flexibility to respond to crises, minimizing the magnitude of economic shocks. As such, the next formal hypothesis of the paper is that employment mandates reduce the costs of banking crises.

H4: CB Employment mandates mitigate the economic costs [unemployment/financial shocks] of banking crises when Functional CBI is high.

Another test that can be employed is a more explicit test of the potential mechanism. I have already discussed how bank lending is directly related to monetary policy actions (as are stock market reactions), though these conditions are still one step further in the monetary chain of causality. Thus, a test on interest rate behavior would also prove illuminating. Here I focus on the real interest rate, which is the nominal interest rate adjusted for inflation. The real interest rate is crucial because, as Meltzer (Reference Meltzer2002) has shown, ignoring movements in inflation can give a misleading picture of overall credit conditions. In the Great Depression, for instance, the Federal Reserve did not fully appreciate that deflation meant rising real interest rates and thus rising borrowing costs, even though nominal rates were low by historical comparisons. I thus test whether employment mandates predict larger reductions in the real interest rates, again conditional on high FCBI.

H5: Banking crises lead to larger reductions in the real interest rate when FCBI is high and CBs have employment mandates.

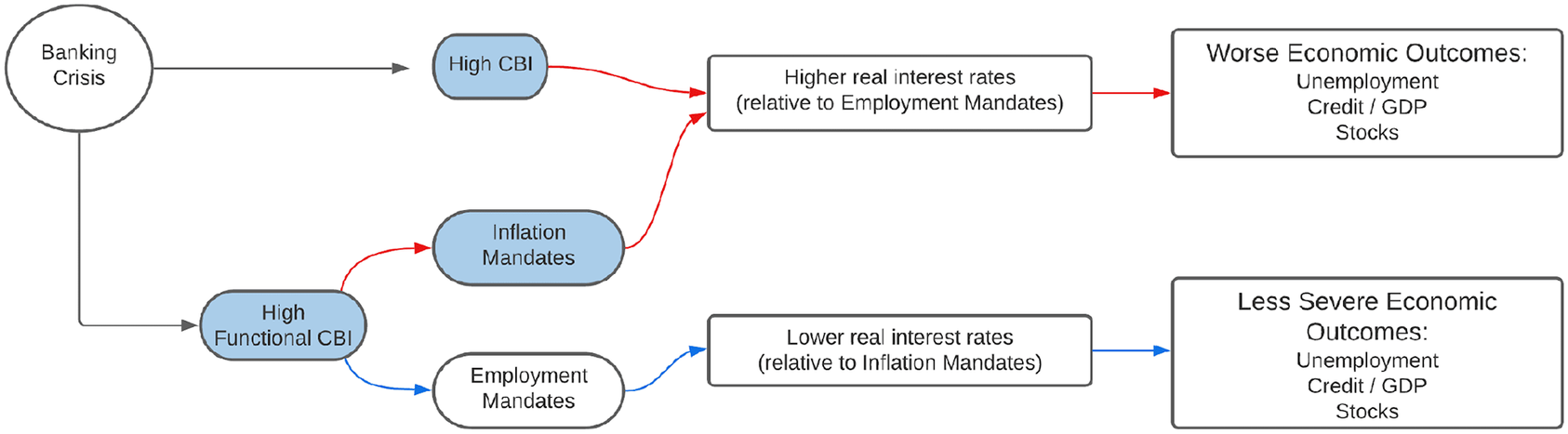

Figure 1 depicts the theoretical expectations. Banking crises cause the shock to the system, and we observe variation in the severity of outcomes based on the institutional arrangement of the central bank. High CBI is shaded along with high FCBI and inflation mandates to illustrate that this is what classical CBI is coded to represent. Thus, CBI is split into parts here to distinguish the relative merits of FCBI versus inflation mandates. From there, we observe different monetary policies, and importantly, variation in the severity of the main economic indicators. H1 through H3 are tested via the first pathway through the full CBI index on the main economic outcomes, whereas H4 and H5 are tested by examining the variation in central bank components in explaining both the policy mechanism (real interest rates) and the main economic outcomes.

Figure 1. Theoretical Expectations

Research Design and Data

The data for banking crises come from a combination of Laeven and Valencia (Reference Laeven and Valencia2018), who provide an updated database of 151 systemic banking crises from 1970 to 2017, with the Reinhart and Rogoff (Reference Reinhart and Rogoff2014) coding for systemic banking crises. A banking crisis is considered to have started once a substantial increase in bank loan defaults has arisen and for which a large portion of the banking sector is on the verge of bankruptcy. Data for CBI comes from Garriga (Reference Garriga2016), who provides the most expansive country coverage and thus allows for the best tests regarding the effect of banking crises conditional on CBI. Garriga’s dataset also includes a six-category measure on the objectives listed in the charter for each central bank and is included as part of the overall CBI index. This measure tracks the degree to which CB mandates prioritize inflation. I invert this index such that a 6 is the highest and equals mandates that list economic objectives but do not even mention inflation, whereas a 1 is the lowest value and essentially represents the classic “inflation only” mandate. In the empirical analysis I refer to this as the employment mandate index.Footnote 14

Every model reported in the paper excludes the most authoritarian countries, including only those with a polity2 score greater than -6. This choice follows Garriga and Rodriguez (Reference Garriga and Rodriguez2020), who show that this appears to be the threshold at which CBI becomes at least marginally effective in reducing inflation. The dependent variables are the unemployment rate from the International Labor Organization, domestic bank credit/GDP ratio, which comes from the IMF’s Global Financial Development Database (GFDD), Stock Market Capitalization (GFDD), and real interest rates (WDI). For all dependent variables, I take the log of the dependent variable to constrain outliers and use the first-difference transformation, as I am interested in predicting how the economy changes in response to banking crises. For the full panel data regressions, I include a conventional lag of the dependent variable.

Isolating the effect of CBI requires careful consideration of what other features of the economy may correlate with CBI and could plausibly explain the results. The likeliest candidates would be the overall level of financial liberalization (such as an open capital account or the broader KOF Financial Globalization Index), which could explain larger magnitudes of financial disruptions in crises. Additional possibilities include highly developed financial markets (e.g., the Financial Development Index from the GFDD), the potential for excess risk-taking by lenders (measured by a high level of lending relative to assets in the GFDD), banking system structure (the market/bank ratio; Copelovitch and Singer Reference Copelovitch and Singer2017), or the susceptibility to “credit booms.” The financial development measure tracks the extent and size of banking, mutual fund, and stock market development, which accounts for the potential “wealth effect” argument that a wealthy middle class with financial assets leads to larger government responses to banking instability (Chwieroth and Walter Reference Chwieroth and Walter2019).

I also control for the current account deficit (logged) to capture international financial flow arguments (Davis et al. Reference Davis, Mack, Phoa and Vandenabeele2016), taken from the updated Lane and Milesi-Ferretti (Reference Lane and Milesi-Ferretti2006) EWN database. Additionally, I also control for pegged exchange rates (Shambaugh Reference Shambaugh2004) and de jure financial globalization (which tracks capital account openness). Other economic controls come from the World Bank WDI database. These include government fiscal balances (which establishes that the effects are not driven by the executive branch), currency reserves/GDP ratio (logged), the average of Western interest rates, a dummy variable for the Global Financial Crisis (“US Crisis”), the government’s Debt/GDP ratio (logged), IMF credits (logged), GDP per capita, logged population, the logged CPI inflation index, and trade openness. In addition to controlling for these factors, I also use country fixed effects in the baseline models, helping to guard against omitted country specific idiosyncrasies.

My baseline empirical strategy follows literature examining the cost magnitude of banking crises, such as Dell’Ariccia, Detragiache, and Rajan (Reference Dell’Ariccia, Detragiache and Rajan2008), wherein they interact banking crises with market aspects they argue explain the magnitude of the shocks. This permits the use of the full range of data available for the dependent variables in examining how banking crises affect these measures compared with their historical baseline in addition to maximizing the sample size. For my purposes, I test the interaction of the event of a banking crisis with CBI in order to predict the relevant dependent variable.

Results—CBI

Table 1 reports the results of the effect of banking crises conditional on the aggregate index of CBI. The different economic severity dependent variables are noted in the column headers, and the models use country clustered standard errors. For each dependent variable, I alternate between a more parsimonious and robustly specified model with a larger set of controls, and unless the variable is noted to use the difference operator (D), almost all controlsFootnote 15 are lagged to avoid the concern of posttreatment bias on the crisis dummy. The controls that are in first-difference form—a country’s fiscal balance (% of GDP), international economic (globalization) flows, and the exchange rate (capturing currency depreciations)—were differenced because theoretically changes in these measures would better capture the changing economic responses during a crisis. Because the onset of a banking crisis clearly changes the exigency of fiscal action by the government, controlling for changes in the government budget allows me to rule out that somehow the effect of CBI is really driven by external government (in)actions. In other words, it helps me to pin down that the economic outcomes we observe in relation to CBI are not driven by executive branch fiscal policy and are in fact related to central bank activity.

Table 1. CBI and Banking Crises

Note: All models are country fixed effects models with country clustered standard errors. All control variables are lagged unless given a differenced notation (D), except for Left Govt or XR peg. *p < 0.1, **p < 0.05, ***p < 0.01.

Before we directly interpret the results presented here, it is worth addressing conceptually the potential interpretation of an interaction between banking crises and CBI. If banking crisis onset is not a function of CBI, then one might interpret the interaction implicitly as a difference-in-difference design, where crises are exogenous shocks with respect to CBI and we see how the treated group (high CBI) responds to the shock compared with the control group (low CBI). Thus, given an interpretation that CBI is not causally related to crisis onset, we have a cleaner interpretation of the interactive effect. To assess this potential, I used a model selection technique—Bayesian model averaging (BMA)—in order to agnostically assess which predictors of banking crises appear to be robust predictors of crisis onset in a systematic fashion. BMA computes the degree to which various combinations of regressors maximize the predictive accuracy of the model, comparing all possible combinations of regressors while penalizing model complexity. For my purposes, BMA estimates the probability that each regressor should be included based on the frequency with which its inclusion improved the fit of the model and the degree to which the model fit was improved with its inclusion. Thus, compared with all possible combinations of models (given the set of variables included), BMA computes a posterior inclusion probability (PIP) as an overall indicator of the success of each variableFootnote 16 in contributing to model fit.

I estimated the BMAFootnote 17 with a large list of common crisis predictors, both political and economic, and for many variables where sensible I included differences of the variables in case changes predicted crises better than levels. A plot of the best models are depicted as Figure A1 in the appendix, where we can see the lions’ share of the predictive power in the banking crisis model comes from the top 8 or 9 variables, after which improvements in model fit (the x-axis) become infinitesimally small. CBI does very poorly as a predictor, coming far down the list and with a PIP of nearly zero (0.4%) and a density plot showing predicted confidence intervals overlapping with zero. Thus, we can proceed on the assessment that CBI is not a significant predictor of crisis onset. Regardless, in the robustness section I discuss implementation of a model controlling for the nonrandomness of crisis onset. The results are completely consistent with the main results from the fixed effects estimation.

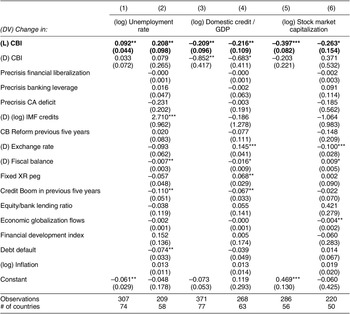

Table 1 shows strong support for the argument that CBI magnifies the costs of crises. In each model we observe that the interaction of CBI and banking crises is significant at the 0.05 level and in the expected direction. For the unemployment rate models, banking crises lead to significantly higher unemployment as the level of CBI increases. The coefficient of 0.11 is substantively large in that it puts the response to the unemployment rate in the 90th percentile of upward positive shocks to the unemployment rate. In a purely descriptive sense, the average unemployment increase in a banking crisis is roughly triple the magnitude of the typical unemployment response when the level of CBI is above its mean compared with below its mean. The results thus offer significant support for the contention that CBI exacerbates unemployment during a banking crisis. In the credit and stock market models, we see negative coefficients, suggesting that the magnitude of financial shocks (market contractions) is larger when the level of CBI is high.

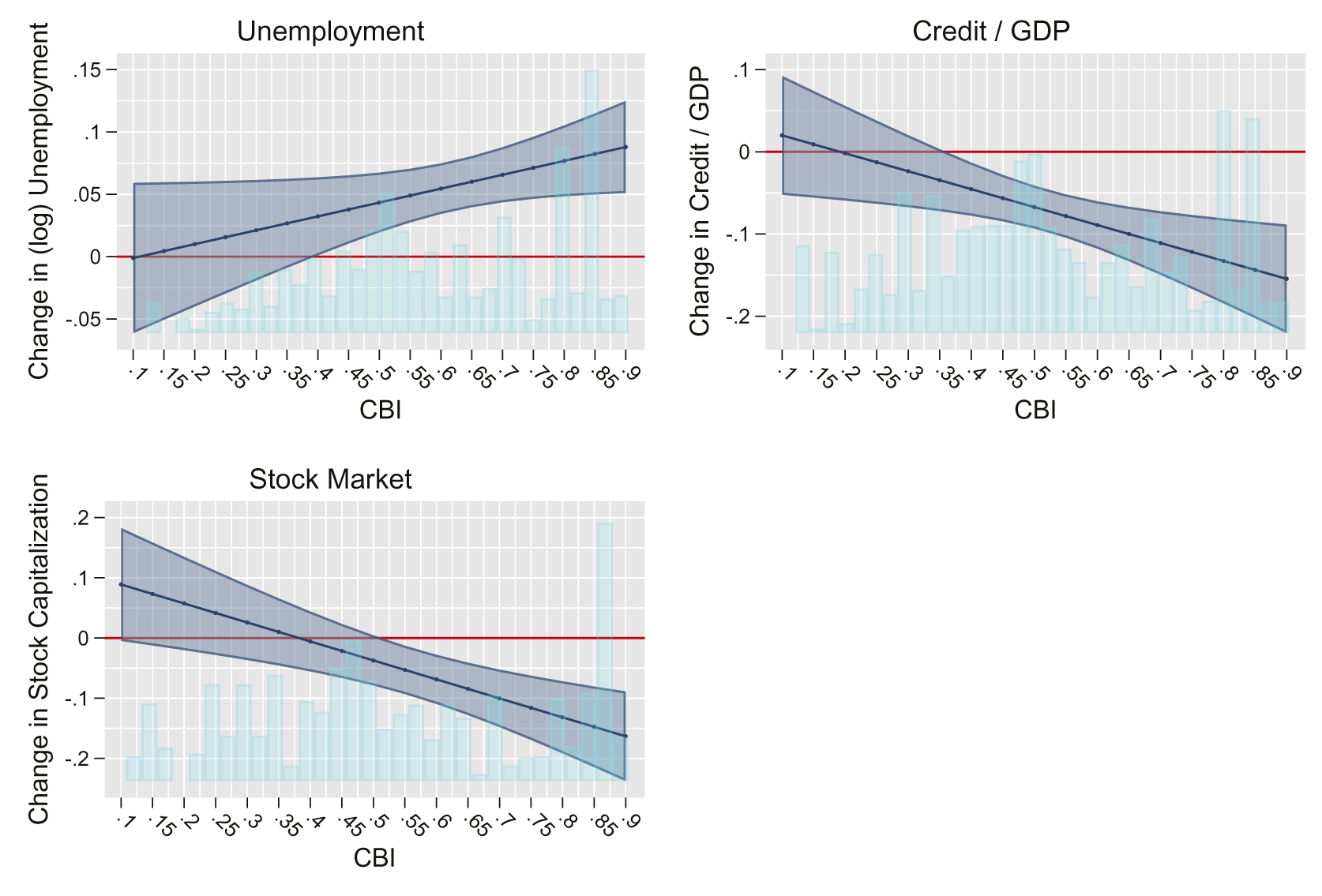

Figure 2 shows the marginal effect of banking crises on economic outcomes varied by the level of CBI,Footnote 18 predicted from the sparse models of Table 1. We see that at low levels of CBI, the effect of banking crises on unemployment varies significantly and overlaps with zero, whereas at high levels of CBI changes to unemployment rise much more significantly. It is interesting that banking crises predict only very small changes in unemployment at low levels of CBI, which may relate to existing research showing that not all banking crises actually lead to recessions, a not widely appreciated but established fact (Devereux and Dwyer Reference Devereux and Dwyer2016). For credit and stock market valuations, we see that crises lead to significantly steeper market contractions—larger drops in Credit/GDP and Stock Market Valuation—as the level of CBI increases.

Figure 2. Marginal Effect of Banking Crises across CBI

Alternatively, I model the effect of CBI on crisis magnitudes by subsetting the models to banking crisis year observations only. Doing so is advantageous because, while it sacrifices sample size and the long-run behavior in the economic series of the full panel data approach in Table 1, it allows me to cleanly hold fixed some measures prior to the onset of crises and contrast the effect of CBI during the crisis with other predictors. For instance, in theory it is possible simply that CBI correlates with financial liberalization or banking system leverage, so perhaps those measures have been driving the results. In Table 2, subset to banking crisis observations, I calculate the level of financial liberalization,Footnote 19 bank leverage, and the current account balance in the year immediately prior to the crisis,Footnote 20 and thus I am able to ensure the crisis itself is not influencing these factors and that the effect of CBI retains its explanatory power. Notably, in Table 2 I also test for the possibility that CBI is reformed during crisis windows by splitting CBI into lagged and differenced parts. If large shocks generate CBI reforms, then this effect will be captured by the differenced CBI measure. We see in Table 2 that the effect of CBI (in lagged levels) is significant in all models, both parsimonious and fully controlled, and that the differenced CBI measure achieves significance in only the credit models (suggesting some, but only marginal, evidence of reverse causality).Footnote 21 The coefficients on CBI are also of comparable magnitude to the results from Table 1, offering encouragement regarding the consistency of the results. Importantly, we can see the result for CBI holds controlling for changes in government spending, exchange rate dynamics in terms of fixed exchange rates or currency depreciations, the level of financial development (another potential correlate with CBI), and whether there was a recent “credit boom,”Footnote 22 among other factors. Alternative estimations of Table 2 that instead held CBI at its precrisis level or controlled for the precrisis level of the dependent variables also yielded consistent results in significance and effect size and are available in the appendix.

Table 2. Models Subset to Banking Crises Years

Note: All models are subset to banking crisis years and use country clustered standard errors. All models use regional fixed effects. *p < 0.1, **p < 0.05, ***p < 0.01.

Results—Employment Mandates: Economic Outcomes and Policy Mechanisms

Having now established the strength of the evidence that CBI leads to worse economic consequences from banking crises, I now turn to the evidence regarding whether employment mandates are able to help dampen the severity of crises. Again I expect the variation on mandates to emerge mainly when the level of FCBI is high, given that political and operational independence allow mandates to generate distinctions in behavior and market expectations over the policy response. At lower levels of FCBI, these distinctions collapse to the preferences of the government, especially amidst a crisis. This is also an important test because prevailing theory suggests a high level of FCBI is optimal, but my argument here suggests that an employment mandate coupled with FCBI will yield less severe crisis outcomes compared with inflation mandates.

Table AT4 in the appendix reports the estimates from the employment mandate models, which takes the form of Table 1 using country fixed effects and varying sets of controls. For these models I test the triple interaction of banking crises with employment mandates and a dummy variable for high FCBI, and I present the marginal effects of banking crises across levels of the employment mandate index when the level of FCBI is high. Because I show the marginal effect of banking crises only for high levels of FCBI, the marginal effects appear as a conventional two-way interaction between banking crises and employment mandates. This eases interpretation of the results but is also the precise test of the theory.Footnote 23

Figure 3 plots these marginal effects.Footnote 24 As expected, when FCBI is high, the marginal effect of banking crises on the economic severity measures demonstrate that the most severe economic outcomes arise when central banks have inflation-centric mandates (approaching a 1 in the index). Here, we see the largest unemployment shocks and the largest declines in credit and stock market capitalization. This effect diminishes substantially as we get closer to a full value on the employment mandate index (approaching a 6). It should be emphasized how unlikely it is we would observe such a pattern due to randomness or by omitted variable correlations, as high levels of FCBI correlate negatively with employment mandates. Factors that correlate with classic or FCBI, and might be an omitted variable concern in the pure CBI models of Table 1, are therefore unlikely to explain the variation we see when the estimates are predicted at high FCBI. It is also important to note that the difference in the marginal effects between high and low FCBI is statistically significant for each model estimated.

Figure 3. Effect of Banking Crises across Employment Mandate Index at High Functional Independence

Results—Real Interest Rates

Although these results show the response of economic measures known to be directly consequential from the stance of monetary policy, central banks generally have more direct control over the interest rate environment and thus it would be beneficial to test for interest rate pathways. Table AT5 in the appendix shows the output from the same fixed effects triple interaction regression as shown in Figure 3, though now using real interest ratesFootnote 25 as the dependent variable. The marginal effect of banking crises on changes in real interest rates is depicted in Figure 4. Here we see additional corroborating evidence that the broader economic results we observe are in fact driven by central bank policy. Banking crises predict significantly larger (more strongly negative) reductions in the real interest rate when the bank has an employment mandate, exactly as we should expect if the central bank is doing more to stimulate the economy with aggressive easing.

Figure 4. Marginal Effect of Banking Crisis on Real Interest Rates at High Functional Independence

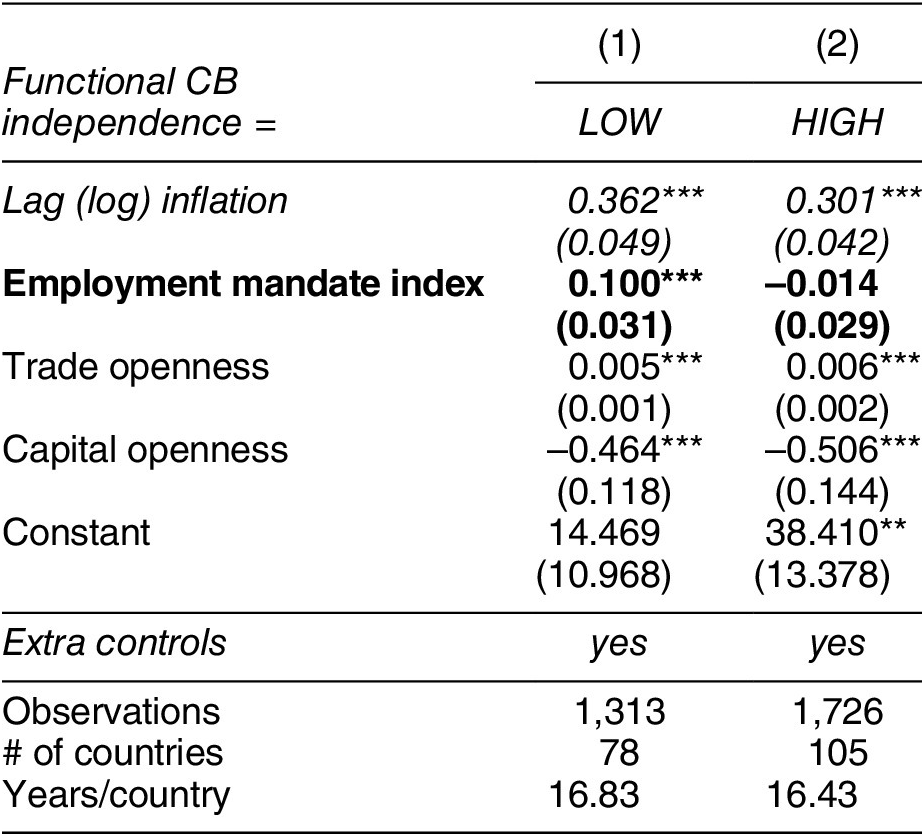

Lastly, a possible concern about employment mandates is that even if they stabilize outcomes in the face of banking crises, this success may come at the cost of higher inflation in the long run. However, I have argued that learning over time has led central bankers to implicitly understand and deeply prize their reputations as inflation fighters such that even with employment mandates it is unlikely that this would lead to high inflation. Given a high level of FCBI, therefore, employment mandates should not exhibit inflationary pressures. To the best of my knowledge no scholar has tested the conditional importance of inflation versus employment mandates in this way and this on its own is a notable contribution. Table 3 reports the results from a fixed effects regression employing common controls for inflation determinants, though most controls are suppressed here with the full model reported in the appendix. Here the evidence corroborates this expectation as well—the employment mandate index predicts higher inflation significantly but only when the level of FCBI is low (noted in column 1). At high levels of FCBI, we see that the coefficient drops from 0.1 to –0.01 and falls insignificant. It is also important to note this model controls for a temporal trend and lagged inflation such that this effect cannot be attributed to the evolution of employment mandate adoption over time.

Table 3. Mandate Inflation Models

Note: DV = (log) inflation. Model (1) is subset to countries with LOW functional CB Independence; Model (2) is subset to HIGH Independence. Models suppress some controls for ease of visualization. Full models reported in the appendix. Models exclude countries with polity 2 < –5. Models include country fixed effects and clustered standard errors. *p < 0.1, **p < 0.05, ***p < 0.01.

Robustness

There remain several concerns regarding the robustness of the results that merit attention. First is that there may yet be unobserved confounders driving the results. Consequently, I have implemented an instrumental variables approach to examine the concern of omitted variables bias. Leveraging the literature on CBI diffusion (Bodea and Hicks Reference Bodea and Hicks2015; Maxfield Reference Maxfield1998), which argues that CBI often diffuses via peer competition and networks, to generate instruments I created categorical variables characterizing a country’s level of democracy (via polity scores), economic level of globalizationFootnote 26 (policy based), and level of GDP per capita. These groupings should map onto economic and mimetic diffusion effects by which CBI could predict other countries’ CB laws. I then calculated the average level of CBI in these peer groupings (excluding each countries’ own value). Each of these indicators is a strong predictor of CBI, both individually and collectively, and clearly cannot dictate the policy responses of central banks during crises, therefore satisfying the exclusion restriction. Additionally, the models control for international flows, changes in exchange rates, and regional exchange-rate volatility, all of which guard against the potential for economic spillovers. However, within a fixed effects specification these predictors individually did not attain sufficient instrument strength. This is not surprising given the significant between-country variation that exists for CBI levels that are ignored in fixed effects estimation. To deal with this issue, I then used principal components analysis to collapse these three individual instruments into their first principal component. This measure significantly outperforms any measure in isolation and exceeds an F test of 10 in the first stage of the fixed effects 2SLS estimation. When relaxing the fixed effects to a general regional fixed effects strategy, leveraging more variation, the F test jumps to nearly 22.

In Table AT1 in the appendix, I present the results from both the country and regional fixed effects models, and we observe significant interactive effectsFootnote 27 across both sets of models. I present the results from the regional fixed effects in Figure 5 because of the superiority of the instrument strength,Footnote 28 though the marginal effects plots are virtually identical. We clearly see that even with an instrumental variables approach the significance of the effect of CBI in predicting more severe banking crisis outcomes holds.Footnote 29

Figure 5. CBI Instrumental Variables Models: Marginal Effect of Banking Crises

Additionally, out of concern that nonrandomness in the incidence of banking crises is somehow biasing the results, notwithstanding CBI’s lack of predictive power in explaining onset, I follow Creamer and Simmons (Reference Creamer and Simmons2019) and Blackwell (Reference Blackwell2014) in estimating an inverse probability of treatment weighting (IPTW) estimator. The advantage of the IPTW estimator is that it better accounts for potential dynamic biases in the occurrence of the “event,” especially in the context when time-varying confounders may be both pre- and posttreatment measures. The first stage of IPTW involves estimation of the onset of banking crises with a full set of controls (including CBI) and then weighting the regression model (as it appears in Table 1) by the inverse of this crisis probability.Footnote 30 The results are reported in appendix table AT6, and we see highly consistent results such that I can argue the CBI results hold even when down-weighting factors that make crises more likely to occur.

Finally, other robustness measures include accounting for potential contemporaneous error correlation. Table AT1.5 reestimates the main fixed effects CBI models with Driscoll–Kraay standard errors, which account for contemporaneous shocks to panels and are also better suited for large-n panels than are PCSE estimates. Further, I have reestimated the instrumental variables models incorporating Driscoll–Kraay standard errors as well, and the results hold.Footnote 31 Additionally, I also report, in Figures AF6 and AF7, models excluding North America and Western Europe, as well as marginal effects from a seemingly unrelated regression model, accounting for potential cross-equation error correlation. The results are strikingly similar to the baseline fixed effects models. Finally, although recent research suggests that most financial crises are demand rather than supply shocks (Benguria and Taylor Reference Benguria and Taylor2020), it nonetheless is not fully clear the extent to which these results bear on the relative weight between supply and demand factors, and future research may seek to disentangle these effects more clearly.

Conclusion

CBI has long been regarded as a centerpiece to proper economic governance, eliminating some of the worst economic experiences’ while providing for stable outcomes including investment, credit access, and potentially growth. Among these outcomes should be—according to theory—that CBI leads to better management of economic shocks, given that the banks’ inherent anti-inflation fighting credibility gives wider scope for monetary easing and stimulus. I show that this prediction is decidedly not the case—central bankers not only fail to use this credibility to fully respond to crises; this lack of responsiveness leads to significantly worse outcomes. While the literature has classically argued that inflation-centric or “hierarchical” mandates would be superior to alternative forms, I show that such mandates are the driving force in the failure to adequately respond to crises. Furthermore, while they induce inflation myopia and monetary rigidity in the face of financial disturbances, I also provide evidence that such mandates do not yield any gains to inflation performance. Therefore, the return on investment for inflation-centric mandates does not appear very strong. This has significant implications, given that banking crises are such destabilizing events, giving rise to extreme populism, antigovernment activism, and recent events (at least in part) such as Brexit. The reverberations of such failures are likely to last for years to come, and it is questionable whether the European Monetary Union can persist in this fashion.

Worldwide inflation is now at historic lows, at levels not experienced since the time of the Bretton Woods monetary regime in the 1960s. Inflation crises, too, have become increasingly infrequent, and yet banking crises have become common enough even to strike at the heart of developed economies. Skeptics of CBI have increasingly harbored doubts and yet have had difficulty in pinpointing pathways by which it generates economic harm, and even then options such as completely disbanding CBI do not seem particularly advantageous. This analysis both pinpoints significant negative consequences and postulates a method to thread the needle in designing credible but flexible central banks. Preserving functional CBI, while elevating employment goals in the mandate, seems to render central banks more adaptable in the face of financial turbulence. The present analysis therefore shows that one need not trade off valuable independence and the inherent inflation gains it implies in order to accomplish needed flexibility. Without understanding this nuance, there may be significant risks to the legitimacy of independent central banks, and central banking reform—which may be needed—could go too far in reverse, undermining political independence as well as in other areas.

It is additionally important to recognize the limitations of this study in being able to project this as an optimal solution for all countries. While the analysis suggests it would be beneficial in the aggregate, without generating significant inflationary harm, there may be other contextual factors that indicate some countries would still benefit from inflation-centric approaches. Future research needs to carefully assess whether employment mandates affect the credibility of the bank in specific contexts (e.g., with large openness or financial sectors) or in other specific ways. For instance, employment mandates could make the bank less credible when a country has populist leaders, or affect credibility by complicating central bank communication and signaling, or lead to longer time lags in monetary transmission. For now, however, a shift in the conversation toward examinations of which countries do not benefit from flexibility would represent a significant shift and a welcome one.

Supplementary Materials

To view supplementary material for this article, please visit http://doi.org/10.1017/S0003055421001325.

Data Availability Statement

Full replication materials including data and codes are available at the American Political Science Review Dataverse: https://doi.org/10.7910/DVN/9QSQIW.

Acknowledgments

I am deeply grateful to Cristina Bodea for her incredibly helpful insights and encouragement throughout the life of this project. Additionally, I would like to offer a sincere and special thank you to Ben Appel, Jakana Thomas, Ani Sarkissian, Erica Frantz, and others at MSU’s WoC workshop whose comments proved farsighted and very influential. I am further indebted to participants at the Carnegie Mellon PSRW workshop, including Daniel Silverman, Dani Nedal, John Chin, and Ignacio Arana, all of whom gave very meaningful comments early in this project. Alex Mardon, Lora DiBlasi, Hyunwoo Kim, and Kangwook Han were also very generous and helpful with their time and comments. Comrade Tolgahan Dilgin and Peter Penar have also been terrific sources of support. Finally, I am very thankful to the editors and three anonymous reviewers who enhanced the quality of the paper by a significant margin.

Conflict of Interest

The author declares no ethical issues or conflicts of interest in this research.

Ethical Standards

The author affirms this research did not involve human subjects.

Open access

Open access

Comments

No Comments have been published for this article.