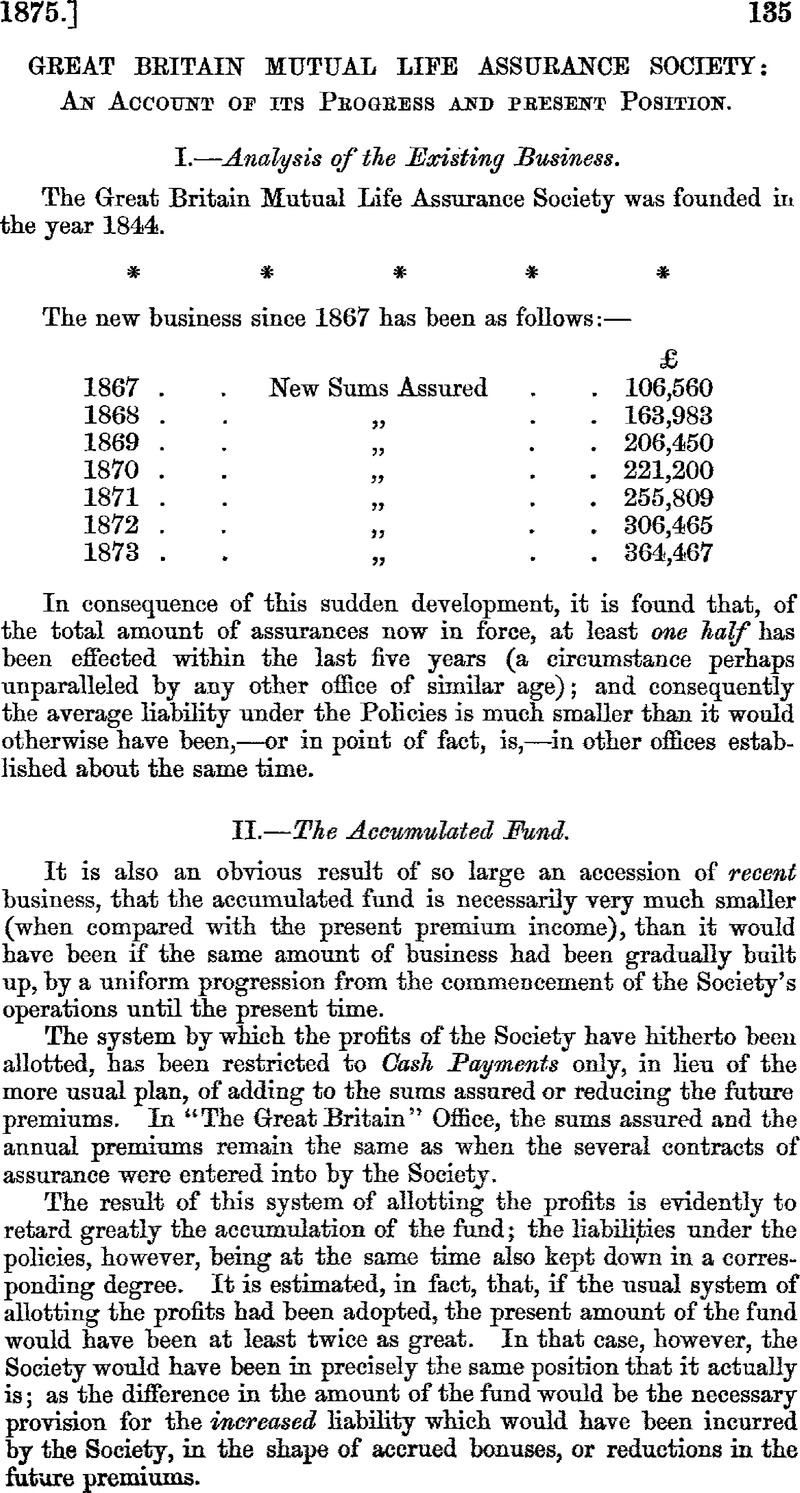

No CrossRef data available.

Published online by Cambridge University Press: 18 August 2016

page 137 note * In determining the “Reserved Surplus Fund” a deduction of 2½ per-cent s i made from the future premiums, as a provision for management in the event of the transaction of new business being discontinued.

page 138 note * The proper mode of treating the expenditure of an assurance company has been correctly explained by Mr. T. B. Sprague, in a letter to the “Times” newspaper, dated the 4th December last. “The expenditure of an office in respect of “its new business” (Mr. Sprague says) “must be held to include the whole expense incurred by the office, beyond that which would be necessary to administer its” affairs, if it ceased to transact new business and confined itself to working out “the existing business.” It is scarcely necessary to remark that, in the case supposed, arrangements might be made by which the expense of working out the existing business would be reduced to a merely nominal amount.