1. Introduction

Healthcare workers are no strangers to workplace injury. Many of these injuries result from accidental contexts, such as poorly maintained work environments or employee missteps. Researchers and policy makers are becoming increasingly concerned, however, with the substantial threat that intentional violence from patients poses to healthcare workers (Dressner & Kissinger, Reference Dressner and Kissinger2018). OSHA reports that healthcare workers face a disproportionate share of workplace violence injuries: healthcare workers incur less than 20% of workplace injuries but 50% of occupational assaults (OSHA, 2016).Footnote 1 This phenomenon has not waned during the COVID-19 pandemic. A survey from four international health organizations reported that roughly 60% of respondents believed that violence increased during the pandemic, with 10% of organizations reporting attacks specifically related to the pandemic (International Council of Nurses, 2022).

This increased attention to violence against healthcare workers has led to calls for government intervention. Representative Joe Courtney introduced the Workplace Violence Prevention for Health Care and Social Service Workers Act in the 116th and 117th congressional sessions,Footnote 2 calling for OSHA to issue an enforceable workplace violence prevention standard that would, in part, mandate that employers develop a violence prevention plan specific for their workplace (Courtney, Reference Courtney2021). While the legislation has not progressed further, OSHA has recently announced that it is developing a proposed rule, Prevention of Workplace Violence in Healthcare and Social Assistance. OSHA is currently convening a small business advocacy review panel to weigh in on the proposed standard. In developing the standard, OSHA is soliciting feedback on “workplace violence prevention programs,” “training,” “violent incident investigation and recordkeeping,” and “approaches to protecting workers without stigmatizing healthcare patients and social assistance clients” (OSHA, 2022).

In assessing the optimality of government regulation, we use the standard metric of the value of statistical injury (VSI), the marginal tradeoff rate between money and nonfatal injury risks. The phenomenon of violent attacks against nurses, however, raises two novel and fundamental issues in benefit assessment—whether intentionality should affect the level of the VSI and whether the training healthcare workers have received, which leads them to view intentional injuries as their responsibility, should diminish the intentionality premium.

Consider first how the nature of the context in which the injury occurs may affect valuation in benefit–cost analyses. The intentionality associated with the injury potentially changes the character of the risk, adding an additional level of dread and nonpecuniary harm, despite the same type of physical injury. These changes may, in turn, affect the amount that workers are willing to pay to reduce these risks. Are workers more averse to the risk of intentional violence—particularly from the people they have been tasked to treat—than comparable risks of accidental injury?

Rather than assuming that the VSI is uniform, this article permits the valuation of intentional and accidental injuries to differ. The results address whether the VSI for accidental harms can be used to value risks of intentional harms, testing the benefits-transfer assumption of whether a standard VSI for workplace accidents pertains to intentional injuries. Whether intentional harms will generate a larger VSI for any given risk level depends on whether the added dimension of intentionality makes workers more averse to these occupational risks. Intentional harms may be more fearsome; the prior literature has observed increased dread for risks that are accompanied by more pain and suffering or for unpleasant types of injuries (Hammitt & Liu, Reference Hammitt and Liu2004; Chilton et al., Reference Chilton, Jones-Lee, Kiraly, Metcalf and Pang2006; Gentry & Viscusi, Reference Gentry and Viscusi2016). On the other hand, health care professionals may consider it their responsibility to prevent such situations from occurring. Indeed, health care professionals may select into the industry based on their relative insensitivity to these types of risks. Identifying separate valuations for intentional and accidental harms will indicate whether there should be differential policy emphasis on intentional injuries.

Our findings suggesting that the magnitude of the harm may hinge on how the harm was inflicted, not just the physical injury profile of the harm, provide the first empirical evidence validating the differential legal treatment of intentional torts (relative to negligent actions). While recovery for negligent actions is greatly restricted when the harm is not physical, recovery for intentional torts can involve nominal damages. The recognition of the additional dignitary harm associated with intentional actions is supported by the premium for intentional risks demanded by non-healthcare workers. Moreover, the difference in valuation by occupation provides an interesting study of the aspects of intentionality that most require compensation. In order to establish intent for battery, most courts only require intent to make contact, rather than the intent to harm. This difference in these standards is particularly stark in the context of defendants with cognitive disabilities being held accountable for battery despite not being able to appreciate the nature of the harmful act. The discernible intentionality premium for non-healthcare workers—and the lack thereof for healthcare workers—have interesting implications for which aspect of intentionality inspires such dread.

The second benefit assessment issue raised by intentional harm concerns how the government should assess benefits in contexts where the people who are exposed to the risk are trained to believe that the risk is their responsibility. Health care professionals may not believe that a premium for intentional harms is warranted if they have been trained to consider it their responsibility to prevent such situations from occurring. However, if the public at large believes that a substantial intentionality premium is warranted, should OSHA adopt such a premium in its regulatory impact analyses? Are there reasons to substitute the general public’s assessment over that of the exposed population? There is a theoretical proximity between this idea and the current discussion surrounding the equity issues in VSL choice in benefit–cost analysis whereby equity concerns could lead to a higher VSL than is expressed by disadvantaged groups (Cecot, Reference Cecot2022, Reference Cecot2023; Kniesner et al., Reference Kniesner, Sullivan and Viscusi2022, Reference Kniesner, Sullivan and Viscusi2023; Kniesner & Viscusi, Reference Kniesner and Viscusi2023). This article analyzes the potential reasons that a healthcare worker’s valuation may differ from that of a lay person—including unobserved risk preferences, values imparted by medical education, and hedonic adaptation—and discusses in which contexts a lay person’s valuation should supersede a health care worker’s valuation.

In addition to the aforementioned questions involving the VSI, intentionality may also influence the preferred mechanism by which workers are shielded from occupational harm. There are two primary approaches. First, firms can compensate workers after injury through workers’ compensation, health insurance, and sick leave policies. Such “insurance”Footnote 3 programs shift the financial burden of economic harm from the worker to the company (and, potentially, to buyers and to workers through wage offsets). However, workers’ compensation provides only partial coverage of financial losses and does not address nonmonetary harms such as pain and suffering. Second, firms can modify the work environment to prevent the actualization of occupational harm. These “protection” interventions may be implemented in compliance with OSHA regulations or industry standards. Efforts to prevent harm not only prevent the medical and wage costs of injury, but also prevent the pain and suffering that a worker experiences during—and potentially after—the injury. Workers may value insurance and protection differently, based on how each intervention affects the probability of harm and the extent of the loss. Moreover, the relative value of protection and insurance may differ by type of harm. Insofar as the nonmonetary costs associated with intentional injuries are greater than those associated with a comparable accidental injury, workers may be more likely to value protection over insurance for intentional harms. This article explores the relative value to workers of protection and insurance as mechanisms to address the risks of intentional violence. The results inform the extent to which reform efforts should focus on promulgating additional occupational safety regulations to reduce the likelihood of the risk or on increasing the generosity of private insurance and extant workers’ compensation programs. It would be straightforward for OSHA to incorporate an intentional injury premium in benefit assessments. More generous insurance coverage would be a desirable fringe benefit for employers to provide in work situations in which intentional injuries are frequent.

This article presents the results of an incentivized choice experiment in which participants make pairwise decisions between job offers differing by wage, risk level, and out-of-pocket costs associated with injury. Asked to place themselves in the role of emergency room nurses, participants choose between jobs that offer one of two “Alternative” conditions—jobs that reduce occupational risk levels (“Protection” regimes) or jobs that compensate workers ex post for harm incurred (“Insurance” regimes)—and jobs that offer neither (“Traditional offers”). The experiment also randomly assigns the nature of harm: participants face the risk of either intentional or accidental injury. The experiment is run both on healthcare workers and nonhealthcare workers.

This design allows us to address the two questions introduced above. First, we use the choices of participants assigned to the Protection regimes to estimate the implied value of statistical injury for risks of intentional and accidental injury, providing a test of the benefits transfer assumption. The results indicate roughly a $40,000 VSI premium for intentional harm for non-healthcare participants. While an explicit VSI premium for intentional harms is not detectable for the subsample of healthcare workers, these workers do require extra compensation if they work in a clinical setting.

Second, we directly estimate relative preferences between Protection and Insurance regimes. We do this by using pairwise choice behavior to impute the range of compensating differentials associated with the higher-risk offer that we designate as the Traditional offer, relative to a lower-risk offer that we designate as the Alternative offer. Having constructed the Protection and Insurance offers to be equivalent in terms of expected monetary harm, the regressions test whether the compensating differential is larger for Protection or Insurance regimes. Understanding that preference for Protection or Insurance may be affected by the nature of harm, we examine these preferences separately for intentional and accidental harms. The results indicate a general preference for Insurance over Protection for accidental risks, and no significant Insurance preference for intentional risks, which is consistent with a greater concern with preventing intentional harms rather than simply compensating the associated financial loss.

Section 2 further outlines the twin purposes of the experiment and its contribution to the prior literature. Section 3 summarizes the experimental design, and Section 4 provides an overview of the data. Section 5 discusses the empirical strategy that was implemented, and Section 6 presents the results of each analysis. Section 7 concludes the article.

2. Approaches to occupational risk

The phenomenon of intentional harm in the healthcare industry has received increasing attention in recent years. Scholars in the nursing field have voiced concerns over the physical and mental toll borne by workers (Gerberich et al., Reference Gerberich, Church, McGovern, Hansen, Nachreiner, Geisser, Ryan, Mongin and Watt2004; Gacki-Smith et al., Reference Gacki-Smith, Juarez, Boyett, Homeyer, Robinson and MacLean2009; Gates et al., Reference Gates, Gillespie and Succop2011) who frequently face intentional violence. The perpetrators of such violence fall into four categories: strangers unrelated to the business, clients, coworkers, and persons with whom the worker has a personal relationship (CDC, 2020). This paper will focus on the threat of violence from clients—patients—as a particularly problematic source of violence, since healthcare workers seek to protect themselves from the very population they are attempting to serve. These risks are heightened in patients with substance abuse or mental illness issues or those stuck in crowded emergency rooms. Attempts to address such violence can be separated into measures seeking to compensate victims for their financial losses and to prevent harm from occurring.

Litigation-based solutions to obtaining compensation by targeting the perpetrator are problematic. The prospect of suing violent patients for the physical and emotional damages they inflict is grim. Many of the patients who suffer from substance abuse or mental illness are essentially judgment proof and unable to pay any award amount. Filing criminal charges risks the danger of further alienating an already-vulnerable population. In terms of employer liability, workers’ compensation is available for workplace violence, provided the attack was motivated by a work situation. Patient-initiated attacks seem to fall neatly into this category. The primary weakness of workers’ compensation in this context is simply the generosity of workers’ compensation programs, which is limited to partial remuneration of financial costs (Grabell & Berkes, Reference Grabell and Berkes2015).

There are several options to reduce the risks of intentional harm. While hiring additional security guards may seem like a common-sense approach to such danger, there may be a counterproductive effect. Because the patient perpetrators are often agitated, the appearance of security may cause further stress to patients, resulting in additional violence. Modifying the environment in other ways may be effective, however. Some hospitals have modified the layout of their emergency rooms to reduce congestion that may agitate patients. Moreover, organizations have advocated for the use of de-escalation training to prevent violent outbursts (Joint Commission, 2019; Shulman, Reference Shulman2020). By educating staff on the process by which patient aggression builds, the training seeks to calm patients well before violence results. The evidence on the efficacy of de-escalation efforts on violent outcomes is weak, however, and merits further study (Shulman, Reference Shulman2020).

The interaction of workplace violence with hospital administration may limit these efforts. Worried that reputational effects of suing patients would disproportionally harm business, hospital administration may prefer that staff members not pursue tort or criminal remedies against their attackers. Such pressures may even cause hospital administrations to discourage reporting of such events. A survey of registered nurses found that respondents who reported experiencing frequent physical violence or verbal abuse did not feel supported by hospital administration in reporting such events (Gacki-Smith et al., Reference Gacki-Smith, Juarez, Boyett, Homeyer, Robinson and MacLean2009).

The legislation that Representative Courtney introduced would require the Occupational Safety and Health Administration (OSHA) to issue a standard for workplace violence prevention for workers in the health care and social service industries. This standard would require employers to develop a plan to protect employees from workplace violence. The plan would include some features of both compensatory measures and prevention, each of which is examined in the choice experiment. The plan can include features that may reduce the risk level in a given work environment, such as “security, staffing, and training on de-escalation techniques, and environmental controls such as personal alarm devices, adequate exist routes, surveillance monitoring systems, barrier protection, entry procedures, and weapons detector” (Courtney, Reference Courtney2018). It would also require procedures for reporting and investigating such events as they occur, which might lead to more workers’ compensation claims.

The experiment developed for this article will examine two related questions concerning different policy approaches to occupational risks of violence. The first question relates to the willingness to accept a higher injury risk and identifies heterogeneity in such valuations depending on whether the risk is intentional or accidental. The second question compares the relative value of Protection and Insurance. To what extent should the policy emphasis be on reducing the likelihood of the threat rather than ameliorating or eliminating the financial harm? While the underlying economic frameworks overlap, with the nature of harm potentially influencing the relative value of Protection over Insurance, each concept is addressed in turn.

2.1. Accidental versus intentional harm

For each of the Protection and Insurance groups, participants face the risk of either accidental or intentional harm. While the subsequent section notes the potential significance of the nature of harm in influencing the relative value of Protection or Insurance, focusing on the Protection treatment alone provides a straightforward measure of the VSI. In doing so, we contribute to the literature on heterogeneity in VSI based on the nature of the harm.

Researchers have calculated VSIs using both wage-based revealed preference evidence (Viscusi & Aldy, Reference Viscusi and Aldy2003; Viscusi & Gentry, Reference Viscusi and Gentry2015; Gentry & Viscusi, Reference Gentry and Viscusi2016) and stated preference surveys (Chilton et al., Reference Chilton, Jones-Lee, Kiraly, Metcalf and Pang2006; Lindhjem et al., Reference Lindhjem, Navrud, Braathen and Biausque2011; McDonald et al., Reference McDonald, Chilton, Jones-Lee and Metcalf2016; Hammitt et al., Reference Hammitt, Geng, Guo and Nielsen2019). In our experimental design, participants’ choices between hospitals that provide neither protection nor insurance and hospitals providing protection allow us to estimate the implied VSI at different initial risk thresholds. The experiment provides a concrete measure of the monetary loss and any nonmonetary impact of the injury. The tradeoff rate between wage and risk yields the implied VSI.

Prior literature has highlighted important differences in estimated values of the VSI. One source of such heterogeneity is the level of risk. Prior work suggests that consumers are willing to pay more per unit of risk reduction to completely eliminate the risk (Viscusi et al., Reference Viscusi, Magat and Joel1987). While this phenomenon might be influenced by the overestimation of low-probability risks, it also may reflect rational preferences. Eliminating a risk removes a potential source of dread that would otherwise be an ongoing concern to workers and be welfare-reducing. Our experimental set-up allows us to test for such a “certainty premium.” By exposing participants to a variety of initial risk levels over the course of the experiments, some rounds allow participants the opportunity to sacrifice wages to achieve a zero-risk environment. This type of phenomenon reflects the influence of behavioral economics factors in market valuations of risks (Kniesner, Reference Kniesner2019).

Another important source of heterogeneity for VSI is the nature of harm. The VSI for accidental harm and intentional violence need not be the same. Even if the health outcomes from accidental and intentional harms are identical, the infliction of harm through an intentional act may generate an additional loss in welfare as well as anxiety regarding future risks of such threats.

Given the potential dread associated with threats of intentional violence, relative to risks of accidental injury, we expect there will be significant heterogeneity in the VSI based on the manner in which injury occurs. By examining such heterogeneity for the VSI, we add to the existing literature examining the heterogeneity of risk valuations. While some work has assessed such heterogeneity in the context of nonfatal injury risks (Robinson et al., Reference Robinson, Eber and Hammitt2022), much of the literature has focused primarily on fatality risks (Hammitt & Liu, Reference Hammitt and Liu2004; Kochi & Taylor, Reference Kochi and Taylor2011; Scotton & Taylor, Reference Scotton and Taylor2011; Viscusi & Gentry, Reference Viscusi and Gentry2015; Gentry & Viscusi, Reference Gentry and Viscusi2016). Both Kochi and Taylor (Reference Kochi and Taylor2011) and Scotton and Taylor (Reference Scotton and Taylor2011) compare the VSL for occupational homicide to other types of risks and report a significantly larger VSL associated with homicide relative to other traditional or accidental fatality risks. This project contributes to this literature by focusing on the intentional/accidental distinction for nonfatal injuries in healthcare. As Viscusi and Gentry (Reference Viscusi and Gentry2015) test the benefits-transfer assumption on VSL based on the source of the injury (transportation versus non-transportation), this project similarly tests the benefits-transfer assumption across the nature of risk.

Finally, this article discusses the choice of VSI when the same risk is valued differently across populations. Prior work has examined the equity issues in VSL choice, particularly in the context of distributional impacts on traditionally disadvantaged groups (Cecot, Reference Cecot2022, Reference Cecot2023; Kniesner & Viscusi, Reference Kniesner and Viscusi2023). Others have considered whether the VSL applied to senior deaths from COVID should be the average VSL or be a value adjusted by age or dread (Kniesner et al., Reference Kniesner, Sullivan and Viscusi2022). Other studies have focused on distinct VSL estimates for particular occupations, as compared to average values. The VSL associated with military servicemembers has been in dispute, with Greenberg et al. (Reference Greenberg, Greenstone, Ryan and Yankovich2021) estimating a significantly lower VSL between $500,000 and $900,000, and Kniesner et al. (Reference Kniesner, Sullivan and Viscusi2023) estimating a bias-adjusted military VSL of $11.8 million. This paper considers a related question, considering the difference in valuation by workers who select into a particular occupation. Depending on whether the difference in valuation is based on unobserved risk preferences which affect selection into occupation, occupational norms that constrain expression of valuations, or merely increasing familiarity with the risk, the government may prioritize the average VSI over the occupation-specific VSI.

2.2. Protection versus insurance

In comparing the value of interventions designed to reduce the probability of harm (“protection”) to interventions that reduce the magnitude of monetary loss, conditional on injury (“insurance”), this experiment contributes to the line of research of Ehrlich and Becker (Reference Ehrlich and Becker1972), Shogren (Reference Shogren1990), and Shogren and Crocker (Reference Shogren and Crocker1991). Protection and insurance interventions are not mutually exclusive; indeed, in many contexts, obligations to cost-share may lead to greater investments in protection (e.g., Gentry & Viscusi, Reference Gentry and Viscusi2019). In this article, however, we examine these two concepts separately for theoretical clarity. The comparison of protection and insurance makes explicit the tradeoffs inherent in a person’s utility calculation. In a gamble between a healthy and injured state, for an equivalent level of expected monetary harm, a person may prefer to mitigate the severity of harm (through insurance) rather than to reduce the likelihood of harm (through protection).

The factors informing this decision are at least twofold. First, risk perceptions may affect the relative preference between increasing insurance or protection. Indeed, Boyer and Dionne (Reference Boyer and Dionne1983) find that risk-averse individuals prefer an increase in self-insurance to an equivalent increase in self-protection in the context of a purely monetary loss.Footnote 4 While this paper focuses on a firm’s provision of protection or insurance to workers for occupational harms, rather than a worker’s willingness to self-insure or self-protect, the intuition is the same.Footnote 5 Second, the presence of nonmonetary harms may be relevant. Some injuries associated with larger nonmonetary harms may alter the structure of utility functions and decrease the relative attractiveness of monetary compensation, boosting the relative preference for protection (Viscusi, Reference Viscusi2019). Moreover, some remedies are better able to estimate and address nonmonetary harms. While monetary harms—such as medical costs and lost wages—are often addressed by both protection and insurance schemes (the former by preventing the injury, the latter by quantifying and compensating the harm), nonmonetary costs are better addressed by only protection.Footnote 6 Indeed, pain and suffering damages are difficult to quantify and largely uncompensated by current workers’ compensation regimes. While litigation (which, again, may be disallowed through a workers’ compensation scheme, which prohibits recoveries from the employer) allows for pain and suffering damages, the awards are highly variable. Moreover, the legal definition of pain and suffering is woefully vague, particularly in jury instructions (Geistfeld, Reference Geistfeld1995). This experiment compares regimes that provide equivalent levels of expected monetary costs (such as medical costs and lost wages), either through protection or insurance, but which explicitly do not cover the nonpecuniary harms of experiencing the injury.Footnote 7 For injuries with higher nonmonetary costs, we expect a relative preference for protection.

Finally, the implications of a preference for either protection or insurance regimes are practically significant. If workers prefer insurance interventions, society may be better off providing supplementary coverage to enhance existing workers’ compensation cost-sharing. Conversely, if workers prefer protection, the type of intervention might look different based on the type of risk: for intentional harms, hospitals may need to reduce the patient congestion in waiting rooms, hire additional security, or train workers in de-escalation techniques. For accidental harms, hospitals may need to reduce the risk of injury by instituting safety protocols, better-securing equipment, and training. Based on the strength of the preference, and its interaction with nature of harm, the policy implications vary.

3. Experimental methodology

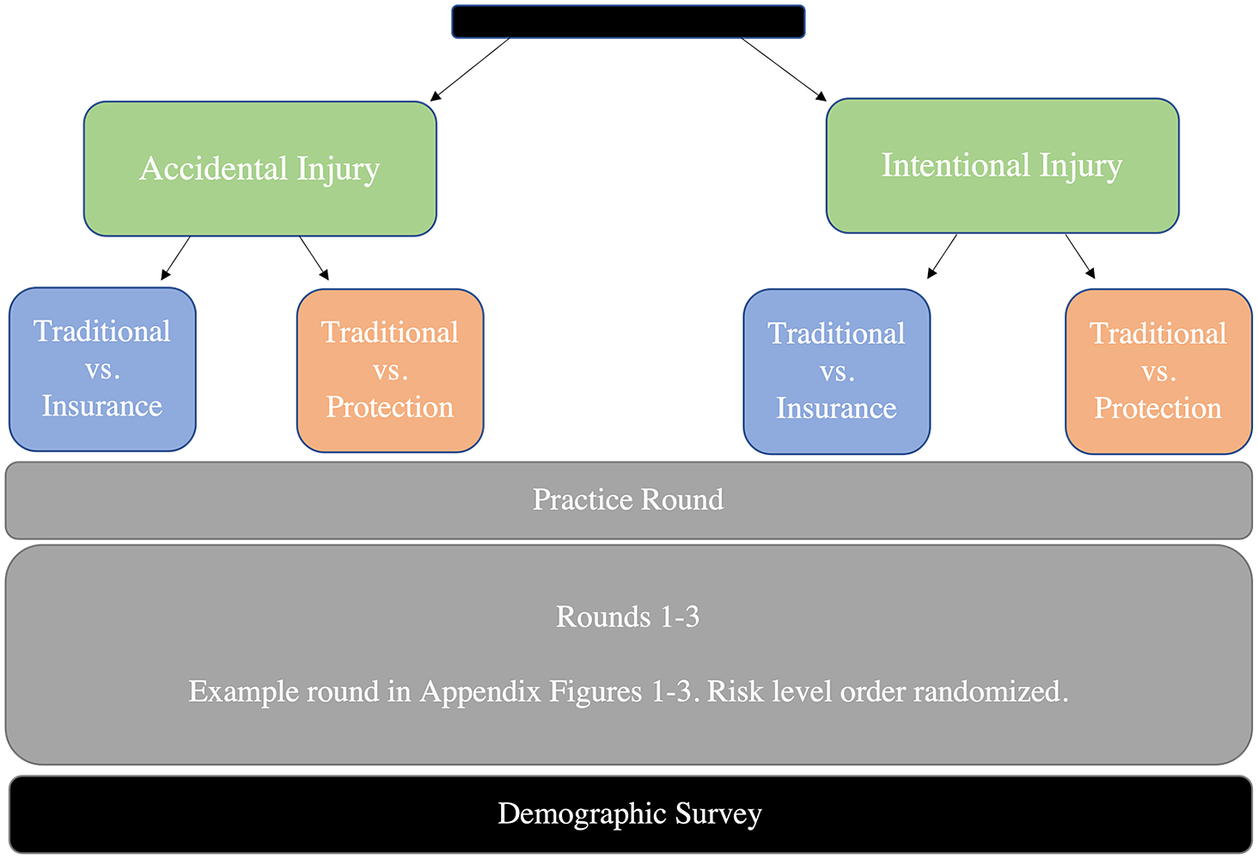

Participants complete a 10-minute survey, administered through Amazon Mechanical Turk (MTURK) via Qualtrics.Footnote 8 Participants are asked to place themselves in the position of an emergency room nurse. A general overview of the experimental design is displayed in Figure 1. The survey begins with an introduction to the risks associated with working in an emergency room. Participants are assigned to one of four treatment groups in a 2 × 2 design: type of injury risk (accidental versus intentional) and intervention (Protection vs. Insurance). Both injury risk types result in the same actual injuries: lacerations on arms, back strain, and head injuries. The source of such injuries, however, differs.

Figure 1. Experimental design. Note: The above figure indicates how participants are randomized into four treatment groups and the progression of the experimental design.

Similarly, the Protection and Insurance regimes result in an equivalent level of monetary harm reduction. “Protection” hospitals manipulate the workplace environment to reduce the risk of injury by 2 percentage points. “Insurance” hospitals commit to covering a portion (or the entirety) of the medical costs and lost wages associated with being injured. This effectively reduces the out-of-pocket costs to an injured employee. This reduction is equivalent to the monetary expected harm reduction afforded by Protection hospitals.

Participants in the “accidental” injury treatment are told that these injuries are accidentally caused by contact with patients, while participants in the “intentional” injury treatment are told that these injuries occur from violence initiated by their patients. The difference in the injury type is described as attributable in part to control, in line with our understanding about the nature of intentional injuries: the intent on the part of the instigator further attenuates control over injury.

Intentional Treatment Prompt: Emergency room nurses face unique risks. Patients who are stressed, coming down from substance abuse highs, or suffering from mental illness can intentionally harm nurses. A nurse’s risk of injury depends on their patients’ characteristics and the way such patients react to the emergency room environment. Patients can aggressively tackle nurses, causing back pain. Patients can attack nurses with sharp objects, like sterile needles, causing hand lacerations. Agitated patients can punch nurses, causing head injuries.

Accidental Treatment Prompt: Emergency room nurses face unique risks. In the course of providing urgent care to patients, accidental acute injuries are a reality. A nurse’s risk of injury depends on their level of skill and the degree of care taken on the job. Nurses can experience back pain from lifting shaky patients. Nurses can lacerate their hands removing sutures from unsteady patients. Nurses can sustain head injuries while stabilizing convulsing patients.

Participants are then instructed on the costs of such injuries. Participants are told that such injuries result in $25,000 in monetary costs, including lost wages (after paid sick leave) and medical costs associated with care (after health insurance). These costs cannot be covered by workers’ compensation or by suing employers. Participants are then told that one chain of hospitals, “Traditional” Footnote 9 hospitals, “rel[y] solely on wages to compensate workers and do[] not provide risk-reduction measures or event-specific cost-sharing.” Participants are then instructed that “Alternative” hospitals do something different. If assigned to the Protection group, participants are told that Alternative hospitals “modif[y] their environment to reduce the likelihood of injury. This modification reduces the injury rate by 2 out of 100 injuries annually. If you are injured, however, you face the full cost of the injury.” Participants assigned to the Insurance group are told that Alternative hospitals “provide[] event-specific cost-sharing for injured workers. This reduces the burden of medical costs and lost wages but does not lessen the pain and suffering of the event.”

After these instructions, participants proceed to a practice round. The practice round instructs them that each round will ask three questions: “One choice between [Traditional] and [Alternative] hospitals that will be eligible for payment” and “[t]wo follow-up questions exploring your preferences that will not be eligible for payment.” Participants are told that the practice round will explain “the structure of the job offers and demonstrate[] how bonuses are awarded.” In the practice round, participants are asked to make a pairwise decision between hypothetical (Traditional and Alternative) job offers which differ based on wage and Protection/Insurance intervention (which affects risk of injury and out-of-pocket costs). Participants are instructed on what each offer entails and are shown the potential payoffs (and probabilities of each payoff) for the offer they chose.

After the practice round, each participant completes three rounds corresponding to three levels of average county risk: 2 out of 100, 5 out of 100, and 10 out of 100 healthcare workers injured in a year.Footnote 10 The round proceeds as follows: participants are faced with two job offers, a Traditional offer (i.e., from a hospital that offers neither protection nor insurance) and an Alternative offer (from either a Protection or Insurance hospital). The participant is asked which offer they prefer, considering only the monetary costs of injury. This choice is eligible to be chosen for payment, so participants are incentivized to report their true preferences.

After submitting their preference, participants receive a prompt describing the pain and suffering associated with such injury (modifications for intentional risk treatments in brackets).

Accidental [Intentional] injuries can be unpleasant to experience. In addition to monetary costs associated with injury, enduring the injury can involve pain and suffering from the accident, along with any lasting emotional distress. Strained muscles are extremely painful; in addition to tenderness, head injuries can make a person feel dizzy and cloudy. Lacerations can be sensitive for days as they heal. [Violent patient attacks can be emotionally traumatic and make it difficult to continue to treat patients.] These nonmonetary costs are incurred only in the event of injury.

After this prompt, the participant is asked two questions. First, participants are asked whether—considering this pain and suffering—they still prefer their prior chosen offer. After participants answer this question, wages change in one of two ways: (i) the wage of the chosen offer decreases or (ii) the wage of the declined offer increases, both by a random amount. After this change, the participant is then asked whether they still prefer the chosen offer or would like to switch. Examples of these screens are presented in Figures 2–4.Footnote 11 The difference in wages between the Traditional and Alternative hospitals’ offers is noted on the screen for participants’ benefit.

Figure 2. Example Round: Screen 1.

Figure 3. Example Round: Screen 2 after Pain and Suffering Instruction, After Choosing Alpha.

Figure 4. Example Round: Screen 3, After Choosing Omega.

Because the program chooses a random interval for the wage variations, sometimes dominated options occur. Since the Traditional offer has a higher level of expected harm, accepting it at an equal or lower wage than that of a Protection or Insurance offer constitutes a dominated option. When a participant chooses the Traditional offer even if it does not offer a higher wage than the Alternative offer, they receive a prompt asking them if they want to change their answer.Footnote 12 Participants who still chose dominated options were flagged as distracted survey takers and dropped from the sample.Footnote 13

The purpose of the second and third questions is to isolate wages at which the participant is indifferent between the two offers. While we do not observe the actual indifference point, we see the interval in which the indifference point lies. If participants end up switching offers, we observe the interval within which their indifference point falls. If participants do not switch, the indifference interval is censored in one direction. We can address this—as well as the point identification of the indifference point for uncensored rounds—through interval regressions.

At the end of the survey, participants answer questions about demographics, behavioral biases, and risk preferences. Participants report their age, gender, race, occupation, education, and income. To understand whether a participant considered themselves to be exposed to less risk than an average person, we ask them about their subjective risk perception in a hypothetical county with an average injury risk of 10 out of 100.Footnote 14 Moreover, given the literature on internal locus of control, we use the Levenson Multidimensional Locus of Control Scale and ask participants to what extent they agree with the following statement: “To a great extent my life is controlled by accidental happenings.”

We take several measures to ensure that participants understand the relevant risks and honestly report their true preferences. To ensure that participants honestly reported their preferences, participants are told that the first question in each round is eligible for payment. At the end of the survey, one of these three choices is randomly chosen. We simulate the participant’s annual experience with the offer’s characteristics. Based on the regime, the monetary cost of the injury would be deducted from their indicated wage and participants would receive $1 for each $60,000 they earned in the experiment. In addition to the base feeFootnote 15, incentivized payouts averaged $0.99, with a range from $0.57 to $1.04.Footnote 16 Based on this setup, participants’ dominant strategy is to pick the offer they believe gives them a higher expected monetary payout. After they have chosen based on monetary payoffs, they are asked about how pain and suffering would change their decision.

4. Data

We collected data during February and March 2021 on MTURK.Footnote 17 In recruiting, we sampled adults located in the United States in two groups. First, we used MTURK’s industry filter system to request adults working in the healthcare industry. This sample restriction provides external validity to our estimates, as we elicit preferences over health occupational risk to workers who have personal experience with this risk. While we cannot guarantee that each has had personal experience with the type of occupational risk specified (i.e., being injured by one’s patients), significant connection to the healthcare industry does raise the same fears. Our sample may contain administrative staff or maintenance workers who work in medical facilities, but the risk of being injured by patients is still salient, and cultural values may be shared. Additionally, by asking about their specific occupation, we can identify which participants were more likely to have experience treating patients (i.e., nurses, nurse practitioners, physicians’ assistants, physicians, etc.). Second, we ran the survey on a sample of MTURK Masters. MTURK workers attain the distinction of Masters when they “consistently demonstrate[] a high degree of success in performing a wide range of [Human Intelligence Tasks] across a large number of Requesters.”Footnote 18 We do not have an industry qualification for these workers; though it is possible that some of them could have worked in healthcare, they will be referred to as “non-healthcare respondents” for the remainder of the paper.

We received 201 Mturk Masters non-healthcare completed responses. We ran the survey on workers in the healthcare industry, collecting a total of 92 completed responses in February and 98 in March.Footnote 19 After dropping two observations that could not be matched to a valid confirmation code and participants who made strictly dominated choices, we are left with 165 healthcare participants and 191 non-healthcare participants.

Table 1 displays descriptive statistics per treatment group. Our non-healthcare population is relatively evenly split across gender and age but is about 86% white. Our healthcare population is 30% male—a higher percentage of males than the 9.4% in the general registered nurse population, based on a recent national study of the nursing workforce (Smiley et al., Reference Smiley, Ruttinger, Oliveira, Hudson, Allgeyer, Reneau, Silvestre and Alexander2021). Moreover, the racial split is comparable to the registered nurse population (roughly 80%). More than half the healthcare sample report having a bachelor’s or master’s degree, though this amount is less than the national registered nurse population (65% receiving a bachelor’s degree). Our healthcare sample is also a bit younger than the average registered nurse, whose median age is 52. In addition to demographic factors, we ask participants about how they would classify their occupation. We then classify any participants reporting to be a physician, pharmacist, nurse practitioner, physician assistant, nurse, pharmacy tech, nurse assistant/nurse aide/healthcare assistant/operations assistant as “clinical” staff. Clinical workers constitute roughly 50% of the healthcare sample (with 12 of the 191 non-healthcare participants reporting clinical occupations). While the comparisons to the registered nurse population are not perfect (and indeed, not all respondents are clinical workers), the spread seems plausible, and we control for such demographic characteristics in the following analyses.

Table 1. Descriptive statistics, by treatment group.

Note: The above table lists the summary statistics for the four treatment groups and two populations.

5. Estimating compensating differentials from interval data

The first step in processing our raw data is to ascertain intervals of compensating differentials from the observational data, which will then be used to estimate tradeoff rates. The raw data we observe are a series of job profiles and decisions preferring one over the other. If participants switch offers, we observe the interval of wages over which participants experience indifference. If participants do not switch offers, the indifference interval is censored on the left or right. From these series of choices, we infer intervals of wages for which the participant is indifferent. An example is given below:

In this first example, after the participant chooses the Alternative offer, the Traditional offer’s wage increases.Footnote 20 Because the participant switched their answer in choice 2, we know that there is a Traditional wage between $61,000 and $62,000 for which the participant is indifferent between the Traditional offer and the Alternative offer at $58,000.

This next table shows what happens when a participant does not switch choices. In this case, she chooses the Alternative offer each time, even though the Traditional offer’s wage increases. From this pattern of decisions, we can tell that there is some Traditional wage above $62,000 at which she will be indifferent between the Traditional offer and the Alternative offer at wage $58,000. This interval is censored on the right above $62,000.Footnote 21

Based on participant choice, the wage over which indifference is interval-identified could be either the Alternative or Traditional wage. In order for our predictors to have the same interpretation, we transform our estimated intervals of either the Alternative or Traditional wage into intervals of difference between the Traditional and Alternative wage. Accordingly, the intervals entering the interval regression are the bounds on the difference in wages between Traditional hospitals and Alternative hospitals at indifference. For notational simplicity, we will call the dependent variable the bounds on the compensating differential associated with risk. This difference can be directly transformed into the VSI and used to compare profiles.

To identify the compensating differential from these intervals, we use an interval regression. The interval regression models the difference in Traditional and Alternative wages at the point of indifference as a latent variable

$$ {y}^{\ast }={\mathbf{X}}^{\prime}\beta +\varepsilon, \varepsilon \sim N\left(0,\sigma \right), $$

$$ {y}^{\ast }={\mathbf{X}}^{\prime}\beta +\varepsilon, \varepsilon \sim N\left(0,\sigma \right), $$

where X is a vector of individual characteristics (e.g., gender, race, education, income, age, and whether the survey was confusing), round-specific features (e.g., risk level, nature of harm, wave of survey), and measures of risk preferences (subjective risk measure and measure of internal control). For our healthcare population, we also include an indicator variable indicating whether the participant reports being a physician, pharmacist, nurse practitioner, physician assistant, nurse, pharmacy technician, or nurse assistant/nurse aide/healthcare assistant/operations assistant.

From this analysis, we can estimate the predictive value of each factor on the magnitude of the wage difference between the Traditional and Alternative offers. In particular, we are most interested in the effect of Protection/Insurance and nature of harm on compensating differentials.

6. Results

6.1. Value of statistical injury

The first issue this experiment examines is the heterogeneity in VSI by nature of the harm. Using the interval regressions, we identify the components of the compensating differential attributable to nature of the harm. The results reveal sensitivity to risk level and risk perceptions for both healthcare and non-healthcare participants. The results also document a VSI premium for intentional harms of roughly $40,000 for non-healthcare participants; a comparable premium for healthcare workers, however, is not detectable.

The dependent variable in the following interval regressions is the interval of the difference between the Traditional wage and Alternative wage at indifference.Footnote 22 For participants assigned to the Protection group, the experiment identifies intervals of the difference in wages at which the participant is indifferent between Traditional and Protection hospital offers. The coefficients correspond to the marginal effect on this compensating differential attributable to a given variable. The following conversion can place these values into differences in VSI:Footnote 23

$$ \mathrm{VSI}=\frac{\Delta {\mathrm{Wages}}_i}{\Delta {\mathrm{Risk}}_i}. $$

$$ \mathrm{VSI}=\frac{\Delta {\mathrm{Wages}}_i}{\Delta {\mathrm{Risk}}_i}. $$

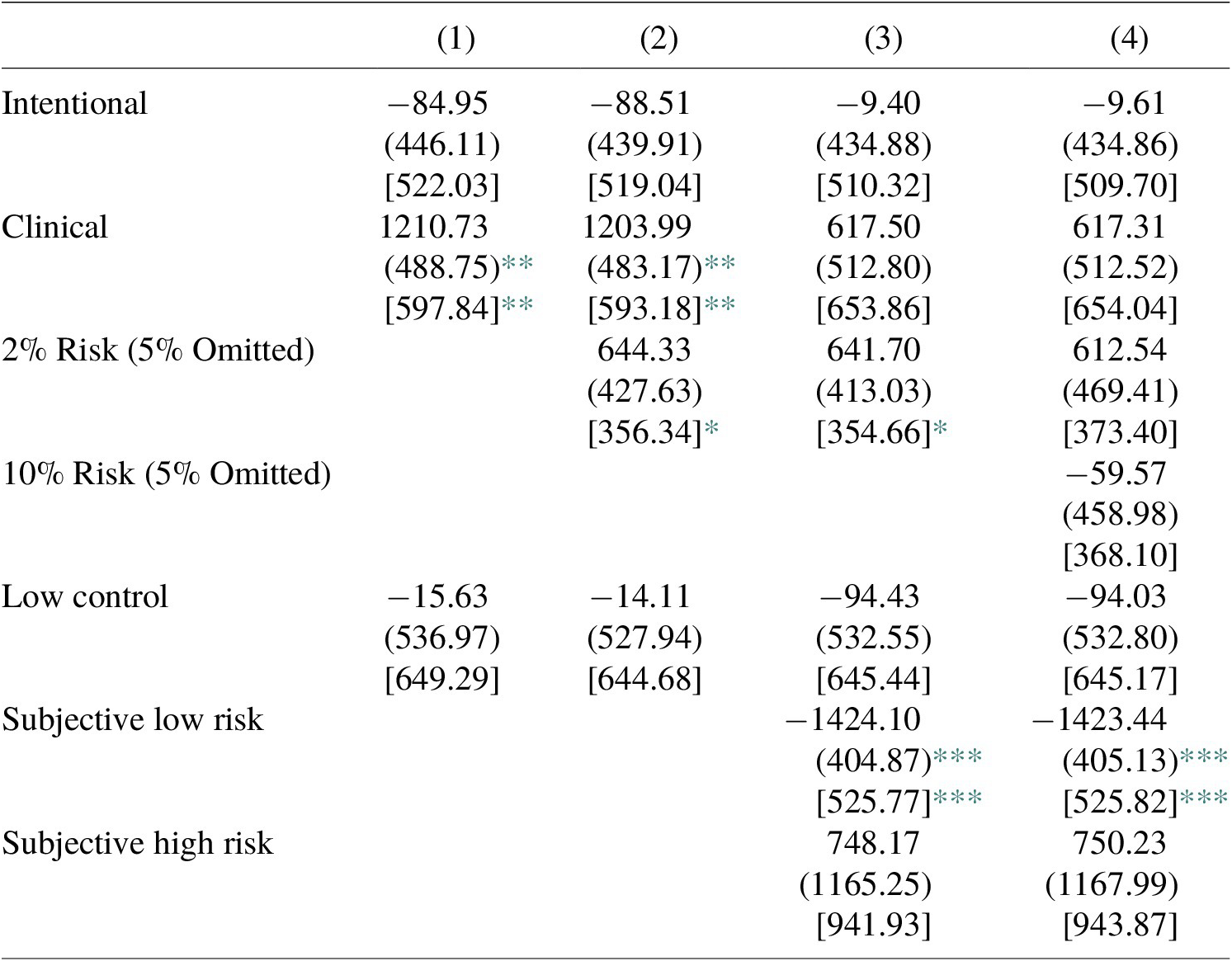

We estimate separate VSI regressions for our healthcare and non-healthcare samples.Footnote 24 In addition to the variables listed in the table, each regression controls for other variables, including income, age, race, gender, education, wave of sample, and perceived clarity of the survey.Footnote 25 The results of the interval regressions for non-healthcare participants are reported in Table 2. Tables report robust standard errors in parentheses and fractional random-weight bootstrapped standard errors, keeping weights per treatment group proportional to group size and clustering by individual, in brackets. Our discussion below is in terms of the latter errors.

Table 2. Interval regression: determinants of wage difference, non-health care workers.

Notes: Each column represents the results of a separate interval regression, containing 285 observations. Variables included but not reported are categorical variables for income, age, race, gender, education, wave of sample, and whether the survey was clear. Robust standard errors are in parentheses, and fractional random weight bootstrapped standard errors, keeping weights per treatment group proportional to group size and clustering by individual, are reported in brackets.

*** p < 0.01;

** p < 0.05;

* p < 0.1.

Based on the coefficients calculated in column (1) of Table 2, the average VSI for the non-healthcare sample is roughly $187,732.Footnote 26 The discussion below concentrates on the marginal effects of the reported variables.

Intentional takes the value of one if the worker was assigned to the intentional treatment group. Under the hypothesis that workers would pay more to avoid intentional harms than accidental harms, we expect that intentional harms are associated with a higher VSI. Table 2 supports this hypothesis. Relative to the comparable decision for participants in the accidental treatment, those in the intentional treatment are willing to accept roughly $800–900 less in order to lower their risk by 2 percentage points. In other words, the estimated compensating differential (the difference in wages at indifference between the riskier Traditional and safer Alternative offers) is $800 to $900 greater for intentional harms than for accidental harms. This translates to a VSI premium of roughly $43,000 associated with intentional harms. This effect is significant at the 5% level in columns (1) and (2) and just misses significance at the 5% level in columns (3) and (4)Footnote 27 upon inclusion of subjective risk beliefs.Footnote 28

In addition to the nature of harm, the results suggest that risk level is a significant determinant of VSI. As noted above, each participant answers questions for three levels of risk: 2%, 5%, and 10% (5% omitted in the regression). Columns (2)–(3) include indicator variables for 2% risk, relative to higher levels of risk. Since the sample is restricted to the Protection group, this means that participants chose between the Traditional hospital’s risk of 2% and the Alternative hospital’s risk of 0%. Consistent with prior literature, this results in a certainty premium. This premium corresponds to an increase in the VSI of roughly $32,500, significant at the 5% level for columns (2)–(3). In Column (4), when we add an indicator variable for 10% risk (such that both coefficients should be interpreted relative to the omitted 5% category), the difference in wage premium between 10% and 5% risk is not statistically significant.

Risk beliefs play a key role in determining VSI. Low Control takes the value of one when participants agree that their life is controlled by accidental happenings to a great extent. Low Control is associated with a consistent and large VSI premium (roughly $50,000), significant at the 10% level. Intuitively, this makes sense, as feeling subject to random events would prompt a person to require more compensation for risk. Conversely, if participants believed that they have control over risks, they may require less compensation. Subjective Low Risk takes the value of one when a participant indicates that they believe they would face a lower than average risk as a healthcare provider. Subjective Low Risk is negative, as hypothesized, but not statistically significant.

Table 3 displays the results of comparable interval regressions for healthcare workers. As above, demographic information is included in all regressions but not reported. Using the same method as above--and the coefficients calculated in Table 3 column (1)--the average VSI for the healthcare sample is roughly $201,371.Footnote 29 As before, the discussion below concentrates on the marginal effects of the reported variables.

Table 3. Interval regression: Determinants of wage difference, health care workers.

Notes: Each column represents the results of a separate interval regression, containing 237 observations. Variables included but not reported are categorical variables for income, age, race, gender, education, wave of sample, and whether the survey was clear. Robust standard errors are in parentheses, and fractional random weight bootstrapped standard errors, keeping weights per treatment group proportional to group size and clustering by individual, are reported in brackets.

*** p < 0.01;

** p < 0.05;

* p < 0.1.

Importantly, healthcare participants are not associated with a significant wage premium for intentional harms. Indeed, the point estimates are often negative, although the implied test scores are close to zero. The contrast of these results, relative to the results for non-healthcare participants, is stark. It suggests that healthcare workers do not differentiate between accidental and intentional harms, although people outside the healthcare market do.

Clinical status, however, is associated with a VSI premium. Participants who report working in a clinical setting are associated with a $60,000 VSI premium in columns (1) and (2), significant at the 5% level. Inclusion of subjective risk beliefs, however, cuts the magnitude of this effect by half. The results are consistent with clinical workers understanding the risks associated with patient care and demanding more compensation. The more pessimistic beliefs of clinical workers reduce the effect of clinical status once risk beliefs are explicitly introduced.

As in Table 2, Table 3 displays evidence of a certainty premium. The magnitude of this effect is comparable to those for non-healthcare participants, but noisier (only significant at the 10% level in columns (2) and (3)). In column (4), when an indicator variable for 10% risk is included (such that the effects are relative to a 5% risk level), both risk level coefficients become insignificant.

As hypothesized, subjective risk perceptions, included in columns (3) and (4), have the expected signs. Subjective Low Risk is associated with a statistically significant VSI penalty of $70,000, while Subjective High Risk is associated with an insignificant premium. Low Control, a significant predictor for non-healthcare participants, is not statistically significant and is close to zero throughout.

As noted above, the estimated VSIs—using the specification from Tables 2 and 3 column (1)—range from roughly $187,732 for nonhealthcare workers and $201,371 for healthcare workers. Prior wage-based revealed preference studies have calculated VSIs within the range of $20,000–$160,000 (Viscusi & Aldy, Reference Viscusi and Aldy2003). Viscusi and Gentry (Reference Viscusi and Gentry2015) find a VSI of around $80,000 and Gentry and Viscusi (Reference Gentry and Viscusi2016) find a VSI of roughly $150,000, both using rates involving injuries requiring days away from work. VSIs do vary with severity, however, and the injury described within this study is not minor. The lost wages and medical costs outside of paid leave and insurance total $25,000. On an annual salary of around $60,000, this is a nontrivial percentage of income and likely implies a relatively severe injury. As noted above, the patterns for non-healthcare and healthcare workers are striking.

6.2. Relative value of protection and insurance

Given the construction of the Protection and Insurance Alternative groups, direct comparisons of the compensating differentials between groups are themselves informative. The survey explains that Protection hospitals reduce the risk of injury by 2 out of 100. Given that monetary harm is $25,000, Protection hospitals have an expected monetary harm of $500 less than their traditional counterparts. In order to create a comparison between Protection and Insurance in which the financial consequences of the policies are equivalent, we choose insurance amounts to make Insurance profiles have the same expected monetary harm as Protection hospitals. As a result, the nominal amount of insurance changes with each risk profile, but the Insurance and Protection profiles have the same expected monetary harm for each level of risk.Footnote 30 Because of this construction, a straightforward comparison of the compensating differential associated with participants choosing between Traditional-Insurance offers and those choosing between Traditional-Protection offers provides a measure of the relative value on Protection versus Insurance. While protection and insurance can be considered substitutes for each other, each function in a distinct way. As stated above, a preference for one regime over another depends on both the utility of wealth in the injured state (based on pure monetary loss) and the value of avoiding the experience of harm (pain and suffering).

Table 4 displays the components of the compensating differentials for both accidental and intentional harms. The coefficients should be interpreted as the effect of a variable on the willingness to accept the higher-harm Traditional offer over the lower-harm Alternative offer. As before, each column contains demographic variables not included in the table, including income, age, race, gender, education, and perceived clarity of the survey. Columns (1)–(4) include participants assigned to the accidental harm groups while columns (5)–(8) include participants assigned to the intentional harm groups.

Table 4. Interval regression: Wage difference by type of harm, all participants.

Notes: Each column represents the results of a separate interval regression. Variables included but not reported are categorical variables for income, age, race, gender, education, wave of sample, and whether the survey was clear. Robust standard errors are in parentheses, and fractional random-weight bootstrapped standard errors, keeping weights per treatment group proportional to group size and clustering by individual, are reported in brackets (Xu et al., Reference Xu, Gotwalt, Hong, King and Meeker2020).

*** p < 0.01;

** p < 0.05;

* p < 0.1.

For all columns in Table 4, Protection is associated with a smaller compensating differential than Insurance, as reflected in the negative coefficient for Protection. The negative coefficient indicates that participants are willing to sacrifice more wages to secure an Insurance offer than they would for a Protection offer. Essentially, participants are willing to accept a lower wage in exchange for cost-sharing than for risk reduction, resulting in a smaller compensating differential for Protection groups. This result is consistent with prioritizing liquidity over nonmonetary costs of harm. Given that the out-of-pocket cost for this injury ($25,000) constitutes a large percentage of the average annual income (roughly $60,000), this is not an unexpected result. For columns (1)–(4), this effect is statistically significant at the 10% level, suggesting that participants have a higher value of cost-sharing than risk reduction for accidental harms. For intentional harms, however, the comparable effect is smaller (29% smaller than the effect for accidental harms) and never statistically significant. The pattern is consistent with a more muted effect for the risk associated with more nonmonetary costs.

Risk level is consistently statistically significant. Columns (2)–(3) and (6)–(7) show that participants are willing to accept lower wages for profiles that have a baseline risk of 2%, such that Alternative offers reduced monetary harm to zero (either through a zero probability or through zero out-of-pocket costs), relative to profiles that do not eliminate monetary harm. This effect ranges from $1,000 to $1,300 for both accidental and intentional harms. This result indicates an increase in the willingness to reduce the risk to zero monetary harm, regardless of whether that is achieved through cost-sharing or risk reduction. When all risk levels are included (omitting 5%) in columns (4) and (8), a clear pattern emerges. Relative to a 5% level of risk, the compensating differential is higher for profiles with 2% risk; conversely, profiles with 10% risk level command a lower compensating differential than at the 5% level ($557 less for accidental harms and $718 less for intentional harms). One reason for this difference in valuation may be the fact that while each Alternative reduces expected harm by the same amount, the difference in expected harm constitutes a higher percentage of total expected harm for lower levels of risk. Either through cost-sharing or risk reduction, Alternative offers reduce expected harm by 100% at the 2% risk level, 40% at the 5% risk level, and 20% at the 10% risk level. Completely eliminating the risk for the 2% baseline case provides an additional benefit beyond the change in the risk level since the worker does not need to be concerned with a continued threat of intentional harm. The lower sensitivity to the same nominal reduction at higher levels of risk may be a function of valuing risk relative to its baseline.

Finally, the results suggest that beliefs about relative personal risks are important. As anticipated, Subjective Low Risk corresponds to a significantly lower compensating differential for accidental harms, as participants require less compensation if they believe themselves to be subjectively exposed to lower risk. Conversely, Subjective High Risk is associated with a positive effect, though this is never statistically significant in any of the columns. We hypothesize that Low Control would be associated with a higher compensating differential, but this effect is not statistically significant in any of the columns in Table 4.

While the above analysis does not explicitly compare preferences over Protection/Insurance by nature of risk, some differences between columns (1)–(4) and columns (5)–(8) are worth noting. While the risk level effects seem comparable, the relative preference for insurance is insignificant for intentional harms. Similarly, while the Subjective Low Risk factor is statistically significant (and in the expected direction) for accidental harms, this factor is less predictive for intentional harms.

The results in general portray a slight preference for insurance in our experimental context. This ordering is consistent with Boyer and Dionne’s (Reference Boyer and Dionne1983) and Briys and Schlesinger’s (Reference Briys and Schlesinger1990) theoretical results for the marginal consumption habits of risk-averse individuals. This ordering is true for both accidental and intentional harms, though the effect is smaller and not statistically significant for intentional harms. Insofar as the intentional harm incorporates more nonmonetary harms, this pattern is also consistent with our hypothesis.

6.3. Discussion

This experimental design provided an opportunity to understand how participants value occupational injury risks, their preferences over risk-reduction or cost-mitigation interventions, and how these differences depend on the nature of the harm. Given the policy relevance of the topic, it is instructive to review the implications of the results.

Contributing to the literature on heterogeneity in valuation of fatal and nonfatal injury risks, the results imply an average VSI in the range of $200,000, varying by population and nature of harm. By using only participants assigned to the Protection regime, we estimate VSI in each context. We calculate the marginal effect of risk perceptions, risk level, and nature of harm on the VSI level. For both non-healthcare and healthcare workers, the effect of risk perceptions is consistent with theory. A sense of low control over external events is associated with a significantly higher VSI for non-healthcare participants. Healthcare workers expressing a lower than average subjective risk perception were associated with a significantly lower VSI, as their beliefs reduced the personal threat that they perceived in the risk experiment. In a similar way, the results replicate the certainty premium found in the prior stated preference literature: eliminating entirely the risk of harm is associated with a significantly higher VSI, on the order of around $32,500.

Regarding the nature of harm, non-healthcare participants demand a higher compensating differential for harms that are intentional rather than accidental. This intentionality premium, on the order of $40,000, is consistent with the idea that the intentional aspect of the injury is an additional undesirable attribute of the harm that makes workers even more averse to these risks. While injuries in both contexts designate the patient as the cause of the injury, the experiment described intentional harms as being associated with more emotional harm stemming from the fact that a patient intended to inflict the injury. Non-healthcare participants imagining themselves in this position would require additional compensation, relative to accidental harms, to take on this risk. The presence of an intentionality premium suggests that the dread associated with an intentional harm is significantly different than that of accidental harms. This result is consistent with the literature on the heterogeneity in valuations of fatal and nonfatal risks depending on the nature of the risk. As prior scholars have found that avoiding homicides are associated with a higher valuation than avoiding fatalities from more accidental harms, our results replicate this difference in the nonfatal injury context for non-healthcare participants.

This intentionality effect, however, is not evident in our healthcare worker sample. The reason for this difference may lie in the culture of medical providers. For healthcare workers, it may be that intentional harm by patients is inherent in the treatment relationship. OSHA acknowledges that there are unique cultural factors influencing the response to intentional violence against nurses and lists 3 main reasons (OSHA, 2015). First, part of the professional obligation is the duty to do no harm, and professionals may want to protect their patients. By reporting patient-related violence, providers may feel that they are betraying their duty to put the patient’s care first. Second, many workers in the healthcare industry consider the risk of violence to be part of the job. Given that this violence generally occurs due to underlying medical conditions (for which the patients are often seeking treatment), it may be difficult to separate patient violence from other occupational hazards. Third, because providers are aware that patients are under the stressor conditions, they may not see the injuries caused by patients as volitional. Indeed, in some cases, patient violence may not have the same emotional valence. This torn loyalty and idea of professional ethics may undercut the general population’s inherent dread of intentional harm.

Indeed, the ambiguity in the concept of intentionality illustrates the potential divide between healthcare and non-healthcare participants. Legal definitions of intentionality in battery fall into two broad categories. Dual intent requires that the assailant intend both to make contact with the plaintiff and to inflict harm, while single intent merely requires that the assailant intend the contact. Indeed, in a famous torts case, Wagner v. State,Footnote 31 a person with a cognitive disability in the care of the state attacked a person at the supermarket. The court held that, despite the inability to appreciate the nature of the harm, the assailant’s actions satisfied the element of intentionality for battery. The healthcare results may imply that—either due to unobserved risk preferences or to medical training making them believe that controlling violence is their responsibility—healthcare workers perceive a lack of intent to harm. If healthcare participants’ dread corresponds mainly to a patient’s intent to harm, healthcare participants may not assign additional dread to actions that intend to make contact but not to do harm and accordingly see the injury as less distinct from other occupational hazards. If intent to harm is the aspect of intentionality that is violative of personal dignity, there may be implications for how tort law treats cognitive disability in battery intent in specific contexts.

While participants in the healthcare sample were not required to attain Masters certification through MTURK, the results do not seem to be driven by a difference in willingness to pay attention. Our rationality checks already screen out distracted participants, ensuring that remaining participants do not make dominated choices. Moreover, the premia associated with clinical experience and risk beliefs follow our hypothesized effects, adding to the credibility of the results. Interestingly, healthcare workers working in a clinical context do seem to command a higher VSI than those who do not, an effect that seems to be channeled through their risk perceptions.Footnote 32

Based on these results, incorporation of a nature-of-harm-specific VSI may or may not be warranted for healthcare workers. If the lack of demonstrable intentionality premium for healthcare workers reflects the sorting of workers with compatible risk preferences into the healthcare field, a premium is not justified. People who are more comfortable handling patient outbursts, despite the violence, may be drawn to the healthcare field, explaining the gap in valuation between healthcare workers and non-healthcare participants. Similarly, the results may reflect hedonic adaptation: the utility of workers who experience such harm declines less than anticipated.Footnote 33 Under either explanation, the intentionality premium should not be applied to healthcare occupational risks.

If instead, the lack of an intentionality premium reflects not a difference in true valuation but in professed valuation due to cultural pressures, use of the non-healthcare intentionality premium would instead be warranted. The use of medical education—and administrative pressures—may make healthcare workers feel responsible for the risk of violence. If the professional culture of healthcare creates difficulty in admitting that intentional harms are associated with more dread than accidental harms, imputing the non-healthcare intentionality premium may be more accurate. The premium accorded to working in a clinical setting may reflect in part a desire for compensation for such hazards. Similarly, insofar as workers do not incorporate the latent effects of being subject to intentional harms in their valuations, such as the higher likelihood of exiting the healthcare market (Pearson, Reference Pearson2023), using the non-healthcare valuation would be more appropriate.

Finally, in interpreting participants’ relative valuation of Insurance and Protection, our results indicate a preference for the former for accidental risks, though this effect is insignificant for intentional harms where intentionality comprises an additional nonmonetary component of the harm. The high valuation of insurance is consistent with the prior literature on preferences over monetary losses in the presence of risk aversion. The higher willingness to accept Insurance (relative to Protection), bodes well for policy interventions such as workers’ compensation and supplementary private insurance. For sufficiently severe injuries, workers may prefer event-specific cost-sharing to ameliorate the severity of the harm more than investments into reducing the incidence of such injury. This may be an optimistic result, insofar as policies to reduce risk in the healthcare setting sacrifice patient care. The statistically insignificant, and more muted, effect suggests that this preference is not as marked for intentional harms. While de-escalation remains an interesting intervention for reducing the likelihood of violent outbursts, the lack of real-world evidence surrounding its efficacy may cause policymakers to engage in more studies prior to mandating it.

7. Conclusion

Intentional violence on the job has become increasingly recognized as a severe problem for healthcare workers. Current legal and regulatory remedies, however, are inadequate to control this phenomenon. Nurses seldom file suits against patients, and government safety regulations have not addressed the shortfall. OSHA’s failure to regulate these risks has stimulated a legislative proposal to require the agency to regulate intentional violence. OSHA has initiated a proposed rule to begin regulating intentional violence. The fact that the injuries arise from intentional acts rather than random accidents does not imply that these injuries are less deserving of regulatory scrutiny.

The incentivized choice experiment in this article explored workers’ valuation of risks of intentional and accidental harms and of the different strategies that the firm might take to address such risks in a healthcare setting. By considering only the Protection regimes in our incentivized choice experiment, we examine the determinants of VSI, which is the main measure for monetizing nonfatal accident risks. We find evidence that relative to the VSI for an accidental injury, non-healthcare participants require a $40,000 VSI premium for intentional harms. This differential is consistent with prior literature suggesting that the value of different occupational risks varies by nature of harm, particularly for dreaded risks. The premium for intentional harms provides empirical support for the legal system’s different treatment of intentional torts, as opposed to injuries that arise from random accidents.

The presence of an intentionality premium may also depend on how workers have been socialized regarding their responsibility for the risk. This intentional violence premium is not discernible for healthcare workers, though healthcare workers in clinical settings do require a risk premium more generally. Healthcare workers may not differentiate between the two types of risk, potentially due to the professional ethic of healthcare whereby workers believe that they are responsible for patients’ behavior.

In assessing the benefits of an OSHA standard to regulate workplace violence, a policymaker must decide whether to use the intentionality premium of the healthcare sample or non-healthcare sample. The lack of an intentionality premium for the healthcare sample may stem from the perception that articulating such preferences is antithetical to their duty to patients. Healthcare workers may have been trained to view patient violence as their responsibility or as potentially not intentional due to its association with an unstable mental state due to substance abuse or illness. It also may be the case that workers who are more comfortable with intentional harms have sorted themselves into the field, in which case an intentionality premium would not be required. However, regardless of the reasons for healthcare workers’ expressed attitudes toward intentional violence, they currently do require a compensating differential when having to work in a clinical setting, and workers at large believe that an intentional violence premium would be required to make such positions attractive.

The estimated VSI is similarly dependent on risk beliefs and risk level. Consistent with prior behavioral economics literature, policies that could totally eliminate injury are especially attractive, no doubt due in part to the diminished anxiety and dread that would be provided by no longer having to be concerned about occupational injury. Participants who believe that they are safer than average require a smaller VSI since the perceived risk that they assess in the stated preference study is lower. Those who believe they have little control over their circumstances are associated with a higher VSI, a result consistent with perceiving a greater risk level.

Given that firms have the option to invest in risk-reduction policies or cost-sharing policies, which regime is valued more highly by workers? Our results suggest that for a severe injury, participants valued Insurance regimes over Protection regimes, consistent with aversion to injuries imposing large monetary losses. This effect is statistically significant for accidental harms but not for intentional harms. Because there are nonmonetary losses arising from the intentional nature of the injury, financial compensation may be less effective in addressing this injury dimension.

Based on these results, the question remains as to what policies are most desirable for addressing intentional violence risks. Legislative solutions often incorporate elements of insurance and protection. The results suggest that expanding workers’ compensation payments and expanding supplementary private insurance may be sufficient, and indeed preferable, for accidental harms. Insofar as such reforms are associated with lower administrative costs, relative to environment modification or de-escalation training, this may be both better for workers and cheaper to implement. For intentional harms, though, this preference may be less strong.

This experiment sheds light on an underexamined aspect of occupational risk: the value to healthcare workers of reducing the risk of intentional violence. As this issue continues to garner more attention, our results present a crucial foundation for further research. In addition to the academic contribution of identifying the heterogeneity in risk valuation by type of injury, our results also have significant practical significance. Not only do the results provide initial suggestions for policy recommendations, but they identify areas in which further research can shed additional light, such as the potential barriers to frank acknowledgment of dread. Further attention to this issue is nothing less than what healthcare workers deserve.

Acknowledgements

Thanks to participants in Conference on Empirical Legal Studies, Southern Economic Association, American Society of Health Economics, and Society for Benefit-Cost Analysis meetings for invaluable comments. Special thanks to Matthew Gentry for computational assistance with fractional random-weight bootstrapped errors.

Funding statement

Funding for this project was available through Florida State University.

Competing interest

The authors declare none.

Open access

Open access