This essay assesses and evaluates the extent to which the African Growth and Opportunity Act (AGOA) increased imports from AGOA eligible countries to the United States from 2001 to 2015. The essay then examines how African countries can make the most of the preferences granted under AGOA, arguing that AGOA national utilization strategies have proven successful. In the final part, the essay explores options for future U.S.-Africa trade relations after the AGOA expires in 2025, proposing approaches that would best support African development. In this regard, this essay argues that, since Congress is unlikely to renew AGOA in its current form and since AGOA will likely be replaced with an arrangement requiring some degree of reciprocity, it will be very important for (1) the African Union's Continental Free Trade Area (CFTA) to be implemented before any new U.S.-Africa trading arrangement comes into force and (2) for negotiations for any future U.S.-Africa trading arrangement not to mimic the negotiations conducted for the Economic Partnership Agreements with the European Union.

AGOA's Impact on Africa's Exports to the United States from 2001 to 2015

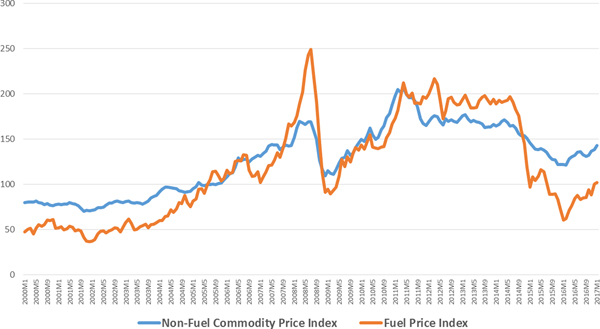

As Figure 1 demonstrates, AGOA stimulated Africa's exports until 2008. However, the trend in the value of Africa's exports to the United States has been downward since then, with a brief increase between 2009 and 2011. By 2015, U.S. imports from Africa had fallen to pre-AGOA levels. This is largely due to a sharp decline in the U.S. demand for fuel and falling fuel prices. Indeed, as Figure 1 shows, AGOA exports to the United States other than petroleum have remained relatively flat since 2001, when AGOA was first enacted.Footnote 1 Using United States International Trade Commission data, every year since AGOA was established, fuels have never accounted for less than 65 per cent of the United States's annual imports under AGOA from the current list of eligible countries. This is amply demonstrated in Figure 2 below, which traces the price index of fuel and nonfuel prices between 2000 and 2015.Footnote 2

Figure 1: Evolution of U.S. imports of AGOA-eligible products from AGOA-eligible countries, 2001–2015 (US$ billion)Footnote 3

Figure 2: Evolution of international fuel prices, 2000 to 2015

While Africa's nonpetroleum exports to the United States have not increased much under AGOA, eligible countries’ exports to the United States have become slightly more diversified and industrial in nature. The largest increase in exports was primarily in textiles and apparel, vehicles, and machinery. However, only a small subset of AGOA-eligible countries has benefitted from these increases. These include Ethiopia, Kenya, Lesotho, Malawi, Mauritius, Swaziland, and South Africa. AGOA-eligible countries’ exports of manufactures to the United States increased, from a very low base, by around US$1.6 billion in real terms (2015 dollars) between 2001 and 2015, an increase of around 40 percent.Footnote 5 From 2001 to 2014, eligible countries’ manufacturing value-added increased by around 75 percent, or US$62 billion (in 2015 dollars). These figures are based on the author's calculations from United Nations Conference on Trade and Development and Trade Law Centre data.Footnote 6 The fact that manufacturing output increased at a faster rate than exports of manufactures to the United States suggests that other factors may have been at work in increasing Africa's manufacturing competitiveness. A number of alternative explanations are possible, including the fact that many of these countries have pursued an aggressive program of investing in infrastructure and building industrial parks to support the development of their industrial sectors.

Underutilization of Preferences

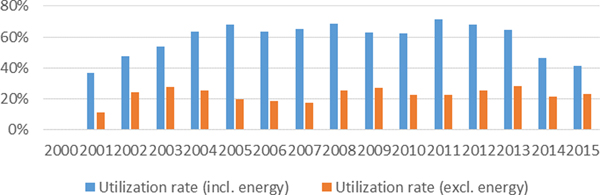

As shown in Figure 3, preferences under the AGOA have largely been underutilized. There are two primary reasons for this. First, capacity constraints, including limited productive capacities and infrastructural challenges in AGOA-eligible countries, have limited African countries’ ability to produce and export products eligible for preferences under AGOA. Second, U.S. market access requirements (such as product standards, sanitary and phytosanitary measures, and rules of origin) limit exports to the United States from Africa under AGOA, since African countries have had difficulty in ensuring that their products meet these requirements.

Figure 3: Evolution of AGOA utilization rate (all AGOA-eligible countries)

In addition, a few products that are economically important for Africa are not eligible to be exported to the United States under AGOA. Only US$1.3 billion of imports of the products that are not eligible for duty-free quota free entry from Africa was reported in 2016. These include apparel (for which the United States has not extended AGOA preferences to all African countries); cane and beet sugar (at least US$88 million of exports of this was reported worldwide as imported from Africa in 2016); some silicon products; some manganese products; tobacco (at least US$7.5 million reported so far); and groundnuts, among others.Footnote 8

AGOA 2015 to 2025, or: How Can States Improve the Utilization of Preferences Under AGOA?

To maximize the use of AGOA market access to the United States, eligible countries must engage in the type of AGOA national utilization strategies that countries such as Ethiopia have successfully pursued. Utilization strategies identify and resolve the barriers that are currently holding back Africa's exports to the United States, often referred to as “binding constraints,” by offering targeted policy options to address constraints both on capacity and on production inputs for selected sectors. The Economic Commission on Africa (ECA) has developed guidelines that provide a framework for National Utilization Strategies. So far, Burundi, Ethiopia, Kenya, Lesotho, Madagascar, Mali, Mauritius, Nigeria, Rwanda, the United Republic of Tanzania, and Zambia have developed such strategies.Footnote 9 Because many of these strategies were published in 2016, there is insufficient quantitative data to examine their impact. However, such an examination is possible for those countries that adopted the utilization strategies before then.Footnote 10 Four of these countries—Ethiopia, Kenya, Madagascar, and Mauritius—experienced export growth to the United States that outstripped the trend in overall exports.Footnote 11 Exports to the United States increased 50 percent from Ethiopia, 35 percent from Kenya, and 131 percent from Madagascar, while imports from Mauritius to the United States remained constant. By contrast, countries that did not adopt such preference utilization strategies experienced a decline in their exports to the United States in the same time period.Footnote 12

Ethiopia has been particularly successful in increasing its exports to the United States under AGOA since it launched its AGOA national utilization strategy. This strategy identifies five priority areas (textiles and garments, leather and leather products, horticulture, handcrafts, and agroprocessing), sector-specific constraints, and interventions to overcome them. Ethiopian authorities also established an AGOA Centre, a one-stop technical and information hub on AGOA to assist these priority sectors in increasing exports to the United States. It is notable that from 2015—when Ethiopia opened its AGOA Centre—to 2016, U.S. imports of AGOA-eligible products from Ethiopia increased in value by 50 percent, from US$44 million to US$66 million. This compares with the total increase of U.S. imports from AGOA-eligible countries of 19 percent over the same period.Footnote 13 The apparent increase in AGOA exports to the United States from countries with a national utilization strategy (where data is available), above exports from those without one, suggests that rolling out such strategies within more countries may be an effective method for increasing African countries’ utilization of AGOA preferences.

It is not just African states that can improve how the AGOA functions. The United States does and ought to have a role in increasing the use by African states of AGOA preferences, given the bipartisan support the statute has received in the past. Two reforms could support utilization of AGOA preferences. First, the United States should streamline its Aid for Trade to Africa programs by developing AGOA compacts that support the implementation of national utilization strategies. Second, the United States should provide incentives to American companies to invest in Africa. This could include a zero tax rate on repatriated earnings for American companies that invest in nonextractive sectors in AGOA-eligible countries.Footnote 14

The Future of Trade Relations Between the United States of America and Africa after AGOA

Both a 2016 report from the United States Trade RepresentativeFootnote 15 and the reported statements of U.S. President Trump Footnote 16 suggest that AGOA is unlikely to be renewed in its current form and that the new administration is likely considering whether some degree of reciprocity should be required in a post-2025 U.S.-Africa trade relationship.

In theory, the introduction of reciprocity in terms of market access could result in negative terms-of-trade effects on Africa, or negative dynamic effects on the continent's industries. These effects are likely to adversely impact the livelihoods of many individuals in Africa who directly or indirectly rely on jobs that produce exports to the United States under AGOA. In order to forestall such negative effects on Africa, it will be important for Africa to ensure that the CFTA currently being negotiated among African states under the auspices of the African Union is in force before 2025.Footnote 17

Indeed, the CFTA would not only help to forestall negative effects on Africa of a possible termination of AGOA; it would also benefit the United States. Harmonized rules of origin and disciplines on (or coordination of) African countries’ nontariff measures such as sanitary and phytosanitary measures under the CFTA may make it easier for American firms to trade with African countries. A single African market would make the continent a more attractive investment destination for American market-seeking foreign direct investment, since the CFTA would mean that an investor in one African country would potentially be able to sell to or invest in the entire African market. Such benefits would accrue where a U.S. investor met the requirements for benefiting from the CFTA.Footnote 18 In addition, the increases in Africa's GDP expected to result from the CFTA would further increase the attractiveness of the African market for American market-seeking foreign direct investment.Footnote 19

A primary impetus for the CFTA is to prepare African Union member states to more effectively trade with their external partners, including the United States. From this perspective, completing the negotiations of the CFTA is an imperative for African countries as it will lay the basis for a new Africa-U.S. trade and investment relationship after 2025. In addition, the CFTA is necessitated by the rapidly evolving global trade landscape. The CFTA could also serve as an important counterweight/corrective to other new trade instruments, including the one that will govern the U.S.-Africa trade relationship beyond 2025.

For example, ongoing negotiations of megaregional trade agreements such as the Regional Comprehensive Economic Partnership (RCEP), the Trans-Pacific Partnership (TPP), and the Transatlantic Trade and Investment Partnership (TTIP) could reshape world trade. While the future of both the TPP and the TTIP remain uncertain, momentum appears to be building towards the RCEP.

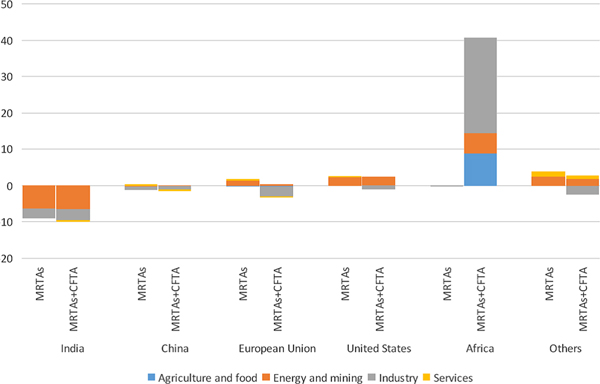

Significantly, these megaregionals are expected to have significant negative effects on Africa due to preference erosion and increased competition from firms based in the states parties to these agreements, as outlined in a computable general equilibrium model of their impacts.Footnote 20 This is particularly the case for the RCEP. What makes the CFTA important to Africa is that if it is successfully negotiated and it comes into force, it would more than offset the possible negative impact brought about by these megaregionals on the continent.Footnote 21

Figure 4: Predicted changes in Africa's exports following Megaregionals alone vs. Megaregionals + CFTA—2040—US$ billion

In any case, if and when Africa negotiates a free trade agreement with the United States, it will be in the interest of both sides to avoid, as far as possible, replicating the particularly cumbersome process that the European Union has followed in negotiating Economic Partnership Agreements with African states and regional groups. Those negotiations have already taken over a decade and most African countries have declined to sign the agreements for a variety of reasons, not least because these agreements have failed to fully incorporate Africa's development concerns.Footnote 23 It will be important for both Africa and the United States to take into account that the United States is no longer Africa's most important export market, having fallen to fourth behind China, the European Union, and India. This means that the trade-off for Africa between retaining full access to the U.S. market, on the one hand, and ensuring that strategic “infant industries” are protected from competition from American firms, on the other, will have shifted towards the latter compared to the past. Indeed, deepening integration between Africa and its Southern partners, particularly from Asia and the Middle East, shows the greatest potential to support Africa's much needed diversification and structural transformation, which will be essential to support more inclusive and job-rich growth on the continent.Footnote 24

Conclusion

Whatever settlement is pursued beyond 2025 for trade between the United States and Africa, it is important for African countries to expeditiously conclude negotiations of the CFTA and begin implementing it as soon as possible—but certainly before 2025. This will be particularly important if post-2025 U.S.-Africa trade relations are anchored in reciprocity rather than the current approach of unilateral preferences.

It also seems clear that a continent-wide market would be good for facilitating Africa's engagement with the United States beyond 2025. In any case, Africa and the United States should try to avoid repeating the process of negotiation between the European Union and African countries on the Economic Partnership Agreements. Hopefully, as Africa gains other trading partners, its negotiating position with the United States will be strengthened as the United States seeks to regain its foothold in Africa as an export market.

Open access

Open access