Preface

There’s one thing that made Boeing really great all the way along. They always understood that they were an engineering-driven company, not a financially driven company. They were always thinking in terms of “What could we build?” not “What does it make sense to build?”

Rarely do newspaper headlines, academic research papers, and monthly reports of investment analysts agree so closely about the slow decline of Boeing as an iconic aerospace manufacturer. Recent newspaper articles with headlines like “Boeing Ditches Chicago Headquarters for Washington” and “Airbus Retains Crown over Boeing as Biggest Jetliner for Three Years in a Row” are examples. Tellingly, they highlight the internal dysfunctions at Boeing, a company that was once seen as an American engineering marvel and a technical innovator in all aspects of aerospace – including its history as a global export powerhouse, in addition to being the biggest exporter in America, with manufacturing sites in several states, plus factories in Winnipeg, Canada, and Nagoya, Japan.

Boeing’s evolution from the time of its founder, William Boeing, reflects the history of modern American capitalism, highlighting the role of private interests and firms who guide the invisible hand. Today’s modern global corporation is largely undeterred over time from participation in political events, dealing with government regulation and technological change with a portfolio of management tools, including the raising of capital. Capitalism in advanced countries comes in many forms, including state corporations. In the global growth of the airline transportation sector, original equipment manufacturers (OEMs) of passenger trains, buses, cars, and planes expanded their market reach, accelerated by government measures to promote but also regulate the sector. Today, the airline sector is the main customer for OEMs, with a record of safety and innovation far beyond the expectations of balloonists, hobby fliers, or planes for military purposes (i.e., reconnaissance, armed conflict, and fighting for air supremacy). It follows that aircraft production even from its earliest days has had both a commercial purpose and a defense role, with governments intimately involved as customers, financiers, technology backers, and defense procurers.

Management tools change with the times, and it is no coincidence that the Harvard Business Review recently (March–April 2023) published an article entitled “How Chinese Companies Are Reinventing Management” and another one on Western firms learning foreign practice, such as Japanese management innovations in just-in-time production, quality control, and precision engineering. American management innovation coincides with the strength and output of the American economy and the US stock markets, where today 60 percent of the world’s public shares are listed. In fact, the rise of conglomerate structures in the USA in the 1960s and 1970s, and the rapid spread of highly diversified corporations in the 1980s and 1990s has a resonance today in calls for fundamental changes in the rules of capitalism and forms of governance.

The rise of publicly listed firms first occurred in Europe, when entrepreneurs saw the stock market as a vehicle to raise money, and investors saw corporate performance and outcomes as a market signal to invest more money or divest. Traditionally, management employed the cash from annual profits to pay dividends but left a portion for new capital expenditures on new growth opportunities. Starting in the mid 1980s, as many firms used mergers and acquisitions to enhance corporate growth, rule changes allowed boards and senior management to pay out excess cash as dividends or use the cash for share buybacks (or share repurchases) or a combination of the two. Starting in 1997, the amount of share buybacks became greater than that of cash dividends. In fact, corporate America recently has spent an unprecedented amount for share buybacks ($1.26 trillion in 2022, see Figure 1).

Figure 1 Aggregate dividends and buybacks paid by US firms and percentage of firms with positive dividends and buybacks in the US.

Boeing’s investment policies followed this governance course. Despite its postwar history as an engineering marvel and a pioneer of the jet age with the Boeing 707 and its launch of the Boeing 747, the Queen of the Skies, in 1968, Boeing has paid over $43 billion in share buybacks since 2009, at a rate which accelerated from 2013 onwards. Underneath Boeing’s public relations umbrella, high development costs, fewer actual orders than expected, and investors unwilling to invest more, Boeing’s state of health was in jeopardy. In Boeing’s home state, Washington, posters showing “Boeing Bust” were common. But as the economy recovered and more travel customers took to the air, Boeing rebounded and in the mid 1990s it undertook the largest merger in airline history by acquiring McDonnell Douglas. With its acquisition of the aerospace division from Rockwell, Boeing created a mix of products, factories, and workers in many locations throughout the USA, but the cost of the merger put pressure on the stock price, as investors sought higher returns. Boeing’s C-suite and board spent up to $43 billion buying back its own shares, but many analysts worried that it needed this cash hoard to meet increasing competition from a new rival, Airbus. Even more worrisome was Boeing’s expensive launch of the new version of the 737, called the MAX.

This Element’s case study addresses the evolution of Boeing and the C-suite model of strategy making and core decisions that most firms must address, namely, the pressures from investors and shareholders on trade-offs between short-term returns and long-term growth. The academic debate about boards and senior managers seeking wealth creation via high financial returns and high executive compensation is juxtaposed with a view where firms have multiple stakeholders, a need for a more nuanced view of the trade-offs, including a focus on exploitation of existing assets and exploration of new assets, which influence a culture of learning and innovation. The complexity of commercial airplanes requires huge amounts of engineering expertise and understanding of design issues accompanied by an awareness that even the smallest error can lead to catastrophic consequences. Boeing’s design flaws led to two fatal crashes of the 737 MAX, with legal, organizational, and financial consequences that are still undetermined. Lawsuits from airlines that didn’t receive orders or who suffered delivery delays are estimated to have cost $8.2 billion, a case of a corporate culture allowing perverse incentives, or penny-wise and pound foolish.

[F]or a time, Boeing would even become a Wall Street darling, doubling down on stock buybacks that channeled cash to shareholders at the expense of other priorities, such as research and development. From 2013 to 2018, almost 80% of free cash went to buybacks, an innovation in financial engineering.—

1 Introduction

In the global growth of the airline transportation sector, the OEMs of passenger trains, buses, cars, and planes correspondingly expanded their market reach, accelerated by government measures to deregulate the sector in pricing and entry barriers, starting with the Carter administration in the late 1970s. Airplanes vary in size and type, from small, single-propellor, short-range planes to long-distance jet propulsion. Boeing became the technological pioneer with the 747, a wide-bodied design with more than 400 seats, ideal for long-haul flights. Growth in travel helped the airline industry, but its real competitive strength was with aircraft OEMs like Boeing, Lockheed Martin, and McDonnell Douglas. Starting with transportation reforms in the Carter administration in the late 1970s, American deregulation initiatives vastly reduced entry barriers for both passenger and cargo aircraft and allowed pricing to become a competitive tool. They also accelerated mergers and industry consolidations among smaller airlines, just as more countries began to privatize their national legacy carriers, such as British Airways and Air Canada.

Today, the airline sector is the main customer for the airline manufacturers, or OEMs, and from its earliest days it has had both a commercial purpose and a military role, with governments intimately involved as customers, financiers, technology backers, and weapons procurers. Orville and Wilbur Wright on December 17, 1903, not only made aviation history but also attracted interest worldwide. For 12 seconds the brothers flew their custom-made Flyer 1, made from spruce wood and powered by a new 12 hp four-cylinder engine with a sprocket-and-chain transmission unit that guided two pusher propellers. In 1909, Winston Churchill, then only a British MP and cabinet minister, and later First Lord of the Admiralty in both world wars, spoke before the Committee of Imperial Defense and suggested the Government make contact with Orville Wright “to avail ourselves of his knowledge.”

Churchill was an early advocate of air power and recognized its military application, not unlike another navy expert, Admiral Isoroku Yamamoto, who understood how air power could make large navy ships vulnerable in battle. Churchill’s restless mindset led him to take flying instructions to get a pilot’s license. At the Admiralty, he established the Royal Navy Air Service and the Royal Flying Corps, which evolved to become the Royal Air Force.

A decade before Pearl Harbor, Admiral Isoroku Yamamoto, who was well-traveled (visits to six countries in Europe), knew details about plans by the American and British navies to employ their superiority in the size of their fleets. Other than size, the Japanese Imperial Navy replicated many aspects of the Royal Navy, including ranks and uniforms. In Japan, Yamamoto took charge of the new Aeronautics Department, which planned and developed aerial weapons, including naval aircraft models such as the Mitsubishi A6 M “Zero” fighter, the twin-engine Mitsubishi G4 M bomber, and the Nakajima B5 N torpedo attack plane. Fluent in English, he was an economics student at Harvard from 1919 to 1921. Like many Americans, including William Boeing, a young entrepreneur who made a fortune in his native state of Washington, Yamamoto brought his ambition and gambling instincts to aviation. He also spent time (1925–1927) in Washington as Naval Attaché in the Japanese Embassy and used that position to tour many American states, including the oil fields of Texas, as well as Cuba and its lucrative casinos in Havana. When he returned to Japan, like Churchill, he also took flying lessons. Yamamoto was open to new ideas and less interested in the traditional military concepts of the navy or the army acting alone. He saw how air power linked to other military units – ships, tanks, and ground-based forces – could operate from land bases, attacking naval targets, including aircraft carriers.Footnote 1

In America, the US Army showed renewed interest in air power, where the legacy of the Wright brothers attracted entrepreneurial copycats worldwide, given the centuries-old history of flight, from the first manmade kites and hot air balloons. In 1907, the Board of Ordnance and Fortification and the US Army Signal Corps issued a request for proposal, but the specifications ensured that only the Wright brothers would be the viable bidder. Two years later, the United States acquired its first airplane at a cost of $25,000, plus a bonus of $5,000, because the Wright brothers’ biplane exceeded 40 miles per hour. Air mail was a lucrative business, and federal contracts were messy, controversial, and politically charged patronage games. In the 1930s, various initiatives by Congress attempted to strike a balance between established companies, especially Transcontinental and Western Air (TWA) and smaller independent operators relying on income from mail contracts, costing taxpayers about $50 million over four years. The Postmaster General, Walter Folger Brown, held hearings known as “spoils conferences,” which reshaped the US commercial air map, dividing the major routes among the four largest carriers (United Aircraft and Transport Corporation, American Airways, Eastern Airways, and TWA).

In 1930, the McNary–Watres Act gave most of the airmail contracts to big, established companies, like American Airways, with the popular war hero Eddie Rickenbacker and a young Thomas Braniff lobbying for the independent airlines. Congress held hearings, and charges of corruption, monopoly, and bribery, mostly unfounded, added to the political rhetoric. President Franklin Roosevelt, first elected in 1932, directed the Postmaster General, James A. Farley, to cancel all airmail contracts and allowed the United States Army Air Service to deliver the mail.

As it turned out, the Army Air Corps was ill-equipped, with inferior machines which were poorly maintained. In fact, after several plane crashes and pilot fatalities, deemed by the media as a “fiasco,” public outrage forced Congress to take action, and the president suspended the operations of the Air Corps. One of the president’s harshest critics was Charles Lindbergh (the first pilot to make a nonstop flight across the Atlantic Ocean), who testified before Congress. The hearings on the so-called Air Mail scandal forced Congress to pass the Air Mail Act of 1934, giving most airmail routes to the airlines but allowing some routes for smaller airlines to promote competition. Regulation was divided among three groups, the Post Office, the Commerce Department, and the Interstate Commerce Commission. Perhaps more importantly, this measure forced a dissolution of aviation holding companies and separated airline firms from aircraft manufacturers.Footnote 2

Wartime put aircraft production at the top of the policy agenda. However, even before the United States joined the war effort after the 1941 attack on Pearl Harbor, President Roosevelt worked with his close ally, General George C. Marshall, on plans to produce 20,000 planes annually. The dour but highly informed Marshall knew that air power alone would need a wider measure of initiatives, like schools to train pilots, technicians to maintain planes, and factories to manufacture ammunition. Roosevelt’s views, influenced by Jean Monnet, head of the French government’s military purchasing department, led to a proposal for aircraft assembly plants in Canada to supply the French Air Force with parts and components shipped across the border, enough for production of up to 15,000 planes a year. When America declared war, aircraft production was only about 3,000; in 1945, it reached more than 300,000 planes, as factories producing consumer and industrial goods were retooled to meet the military’s air-power requirements.

After 1945, OEMs in America had global supremacy in large, commercial airline manufacturing, despite Britain’s limited success with its Comet jet airliner. In the Soviet Union,Footnote 3 manufacturers like Ilyushin, Tupolev, and Antonov sold planes to the state-owned monopoly airline, Aeroflot, with a fleet of 9,700 planes in 1991. Soviet OEMs exported to communist China, third-world countries, Vietnam, and North Korea, and added to the fleet of state-owned Air India. Soviet passenger planes manufactured in Russia and Ukraine never met the technical standards found in the West, including engines, advanced avionics, and the parts and components that make up the final product in the product line of firms like Boeing. Boeing was the pioneer in this new jet age environment.

Today, Boeing has a 100-year legacy in aircraft design and technological innovation,Footnote 4 and is the largest American manufacturer of commercial jetliners, with sales to 150 countries. Boeing’s design and production of the B-17 (Flying Fortress) and the B-29 (Superfortress)Footnote 5 vastly enhanced the firm’s critical mass of skills and internal competences in military and commercial aircraft. Two jet-powered aircraft, the B-47 Stratojet and the B-52 Stratofortress, set the stage for a new age of aircraft design. However, after 1945, in the vastly expanding commercial market, Douglas Aircraft Company and Lockheed were the leaders, while Boeing struggled to align its corporate strategy, starting with the idea of redeploying military design for commercial aircraft. For example, its redesigned model, the 377 Stratocruiser, was a market failure, despite export sales to BOAC. Only fifty-six planes were sold. By 1950, Boeing began a series of design tests for a suite of jet planes suitable for the US military and civilian markets (Figure 2).

Figure 2 Post-war development of large scale civilian aircraft programs 1950 and future developments.

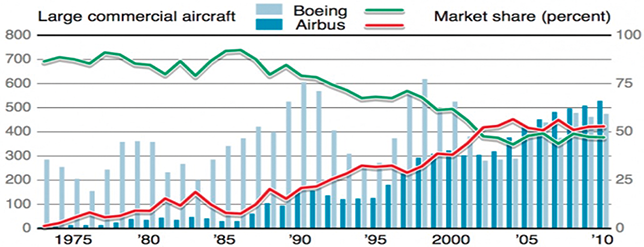

Cleverly, Boeing wanted to break from its past traditions by assigning the 300 series numbers to its propellor-driven models, so it chose the 700 series numbers for its jets (Boeing’s missile division had already adopted the 400–500 and 600 numbers). Five years later, Boeing launched the jet revolution in the airline sector with its 707, adding to its reputation as a design innovator, which dated from its sketches of a swept-wing jet airline in 1949. Jet airliners like Britain’s de Havilland Comet and work in Russia gave impetus to a new plane for long-distance flights at high altitudes, with lessons learned from military aircraft like the B-29 Superfortress and the B-47 Stratojet. By 1954, Boeing’s new prototype, called the 367-80 (or Dash 80), powered by Pratt & Whitney turbojets, became the B-52 Stratofortress. Pan-Am was the first customer, buying twenty in the first order, even though Pan-Am also ordered twenty-five aircraft from another new rival, Douglas Aircraft, whose DC-8 was slightly larger and wider than the Boeing 707 (Reference LombardiLombardi, 2008). Over two decades starting in 1958, Boeing produced 1,010 models of the 707 for commercial use and 800 for the military, far exceeding Douglas’s sales of 556 DC-8s.

However, the 707 program was never that profitable, despite giving Boeing a technological edge and a clear dominance in long-distance and international flights. In fact, Boeing had a 75 percent market share of all civil jet airliners. Jet aircraft also changed the economies of the airline sector, with the complementary alignment of plane design, advanced manufacturing, and short haul and long-distance flights (including pilots, crews, and navigation tools). Further, aircraft manufacturers, airlines, and airports had government support from the beginning, involving a mix of policy tools like direct ownership, tax policies, and R&D support, subsidies, procurement policies, and other forms of support, such as airport runways, and navigation tools, including weather reports. Aerospace programs today are global, innovative, and immensely complex (Reference SteklerSteckler, 1965; Reference Vander MeulenVander Meulen, 1991).

The American government undertook the initial development costs because the US military needed a higher-altitude plane with fuel tankers for its fighter jets. The 707’s development costs illustrated the well-known economics of large aircraft production, known as the experience curve of batch production, colloquially known as the 80–20 rule. In practical terms, when a firm received a contract, say for 100 planes, and then another order for 100 planes, the second order would show a decline in costs by 20 percent, and the same for the next contract, another 20 percent, so costs would decline from 100 to 80 percent and so on, but then stop per-unit declining because of high overhead costs. This experience curve effect comes from a cumulative order book and includes learning tools, so this approach to production planning, sometimes called progress cost curves, experience curves, or learning curves, actually dates to American aircraft production during World War II. In the postwar environment, Japanese firms applied this concept with brutal effect against their overseas rivals on products ranging from integrated circuits, color televisions, motorcycles, and auto components, but were hampered in commercial aircraft production by the geopolitics of US–Japan relationships (Reference McMillanMcMillan, 1985; Reference McGuireMcGuire, 2007; Reference MacPherson and PritchardMacPherson and Pritchard, 2007).

The expansion of the global tourist sector, transforming from a domestic leisure market to a global travel sector, provided opportunities for air travel and the demand for commercial aircraft (Reference RaeRae, 1968). However, until the late 1960s, the combined assets of the six largest aircraft companies were still smaller than Boeing’s. The founding of Airbus Industrie in 1970 as a commercial rival on the global stage was not seen as a direct threat to Boeing’s commercial aircraft dominance.Footnote 6 Airbus introduced its first commercial plane in 1972, the A-300, adopted by Air France in May 1974; but initial sales were sparse, despite pioneering innovations like composite materials, wing tips, electronic signaling, a two-person cockpit, fly-by-wire controls, and only a two-engine, wide-body design. In the early days of Airbus’s entry into the commercial plane sector, Boeing could dismiss this new entrant as another European project to create jobs, and for years failed to appreciate the impact of its new rival until it was too late. Today, Airbus outsells Boeing across the range of models in all key price points – small, medium, and large, long-haul jets – including penetration into America’s airline sector.

Long-term success comes from past failures, and high-reliability organizations (HROs) learn from failure, simple, complex, or catastrophic (Reference Starbuck, Hedberg, Dierkes, Berthoin, Antal and NonakaStarbuck and Hedberg, 2001; Reference McMillan and OverallMcMillan and Overall, 2017). Boeing faced catastrophic failure with the fatal crash of two Boeing 737 MAX planes only months apart – the first by Indonesia’s Lion Air in 2018, the second by Ethiopia Airlines in 2019 – causing a total of 346 fatal casualties. In a book exposing the events over several years, Flying Blind: The 737 Max Tragedy and the Fall of Boeing, Bloomberg journalist Peter Reference RobisonRobison (2019) catalogues the series of errors, misdeeds, and unintended consequences for Boeing, including the grounding of all Boeing 737 MAX planes – those in service, those completed but unsold, and those nearing final assembly. Boeing became the focus of unprecedented scrutiny by governments, pilot unions, investment analysts, Boeing’s unions and employees, airlines around the world, the TV and print media, and the traveling public. Financially, it was one of the biggest corporate disasters ever, with Boeing’s market capitalization falling by two-thirds, resulting in a balance sheet with a net worth of minus $50 billion,

This Element addresses the organizational and management evolution of the OEM duopoly, the Boeing–Airbus rivalry, the financial and governance practices at Airbus and Boeing, and the new risk profiles as the airline manufacturing business moves into the space age. Boeing’s iconic status in America came from the success of its first long-haul, jet-powered model, the 707, which launched the jet age for commercial aircraft, and new models like the 747 launched a new era of long-haul, wide-bodied plane models. The founding of Airbus in the late 1960s was more than just a direct competitive rival. Airbus, slowly at first, helped change the competitive dynamics of aircraft production, introduced new strategic and ambitious stretch goals, and impacted the geopolitics of this vital sector.

In response, Boeing’s response was as much reactive as proactive, more political than technical, in part owing to a series of governance practices affecting the chain of command, such as C-suite executive infighting, the search for CEO succession, and headquarters relocation to Chicago in 1986, before yet another move to Arlington, near Washington, DC. These steps impacted the firm’s collective memory system, a compilation of decision repertoires of routines, attention focus, and mental models that determined top-down and bottom-up decision making. The decision to move Boeing’s headquarters to Chicago, far away from the assembly plants in Seattle, was an organizational shift of Boeing’s organizational culture and added to growing internal inconsistencies between strategic intent and actual execution. The shift was transformational, especially since large institutional investor groups like Vanguard Group, BlackRock, and Newport Trust controlled about 60 percent of total shares outstanding.

Continued financial losses and rising debt raise many questions concerning Boeing’s future. Is Boeing a case study of organizational failure in the global aerospace, akin to the once unassailable industry position of General Motors? Are large conglomerate structures still viable when a core product line and technology become a financial burden, especially when the main customer, the airline sector, faces a volatile environment, depending on economic conditions, energy shortages, and price volatility and, as shown by the Covid 19 pandemic, a shutdown in airline traffic? In general, most people keep a nest egg for a rainy day. Boeing, with its faulty decision to spend $43 billion to buy its own shares, led to a cash crisis and an existential threat, from a failure to meet its delivery targets, a reputation risk to its own once famous brand, sale of product lines to forestall insolvency, and then potential bankruptcy.

Unfortunately, the technological fixes have frequently only enabled those who run the commercial airlines, the general aviation community, and the military to run greater risks in search of increased performance.

2 Theoretical Issues in Complex Organizations like Aircraft Production

As the world has shifted to a society of organizations, all aspects of the aviation sector – manufacturing of planes, airports, and airlines – face incredibly complex activities organizations that require hourly and daily interaction, based on weather, consumer demand, and the human desire to travel. This complex system of planes and air transport is one of the safest and lowest-risk human endeavors on the planet. Yet accidents, plane crashes, and the potential of airline failure do exist. The study of corporate strategy in today’s hypercompetitive global economy, where technological and knowledge innovation are the norm, requires an interdisciplinary approach and an understanding of how a firm’s strategy interacts with existing and potentially new rivals, with implications for customers, suppliers, and new rivals with multiple interactions.

To take a specific example, in less than a generation, the auto sector consisted of highly diversified firms like Mercedes in Germany or General Motors in America, employing the 100-year-old technology of the combustion engine, a mass production system involving a sequence of design, production in large batches, and then a complex distribution system to dealers who actually sold the cars. Today’s auto sector is unrecognizable, producing electronic and hybrid vehicles, and new startups from Europe, China, and Japan have a global reach. A leading brand, the Toyota Prius, is a hybrid, and Tesla is ranked number one in America, ahead of the so-called Big Three from Detroit. Autos illustrate this competitive disruption, and a range of sectors, including airlines and aerospace manufacturers, are experimenting with new fuels, like hydrogen, fuel cells, long-life batteries, as well as electricity.

The Boeing–Airbus duopoly is a timely case study for exploring a range of strategic concepts and theories about competition and the internal capabilities, resources, and tools needed to succeed. Constant innovation changes the competitive dynamics in a sector with high government regulation, legal requirements for certification, a complex system of plane certification, and the role, both direct and indirect, of national industrial policies that shape industry performance. Today’s commercial aircraft and their manufacture are incredibly complex, with the need to align parts and components into a single, overall system, where even the smallest defect or human error causes collateral damage, even more so if the plane is flying at 40,000 feet. The sequence of construction itself is very complex, involving assembly of up to five million parts and components, and using a modular system of subassemblies to manufacture a family of planes, based on size, weight, capacity, and common aspects like seats, fuel tanks, cockpit and cabin layout, and some elements of avionics.

Commercial aircraft take off and land in airports – almost 20,000 in America alone – in varying weather conditions, and each flight requires a bundling of activities to assure high occupancy, service for customers (food and beverages, potential first aid, and luggage) plus cargo, fuel, passport control, and security clearance. For the OEMs, special skills and capabilities require engineering and human decisions for highly dependable, error-free organizational features, where there is a potential for large-scale risk of danger and even catastrophe. Facing recurrent risk, HROs cultivate organizational tools and incentive structures to recruit well-trained personnel, institutional processes of redundancy and regular feedback, and tightly coupled decision systems. In subsystems like research, design, manufacturing, and assembly, for instance, there are differing forms and times of direct feedback, individual incentives, sequential or mutual forms of dependency and uncertainty, with short-term or long-term horizons.

The pioneering study of truly complex organizations owes much to the prominent Yale University scholar, Charles Perrow and his pioneering work,Footnote 7 Normal Accidents. Large commercial aircraft production, and related systems like airport navigation and control, illustrate the combination of hardware equipment, software, and human interaction, which operate in real time. Their intricate characteristics, as set out in Normal Accidents, include interactions that can display unfamiliar, unplanned, or unexpected sequences and which are not visible or immediately comprehensible. They have design features like branching and feedback loops, but opportunities for failures may occur across subsystem boundaries. The second feature is tight coupling, with time-dependent processes which cannot wait; rigidly ordered processes (as in sequence A must follow B); and only one path to a successful outcome, plus very little slack, thus requiring precise quantities of specific resources – skills, timing, specialized equipment – for successful completion.

Regular feedback and constant learning have become a watchword of HROs. High-reliability organizations often are defined not by the absolute number of errors or defects, but by the organizational mechanisms used to mitigate risks and errors, including redundancy and fail-safe measures embedded into the production system. High-reliability organizations, in short, require organizational characteristics such as high social interaction, expert management skills, and teams that structure activities to assure a corporate culture for safety, reliability, and defect-free underpinnings of decision activities.Footnote 8

In advanced economies, publicly listed firms are assessed by results, usually expressed in financial terms like sales revenues, profitability, rise and fall of share price, and overall market capitalization, and now intellectual capital from R&D investments. In fact, despite a vast empirical literature in economics and business where performance is viewed as a dependent variable,Footnote 9 few studies view performance with itself as a different causal variable, where performance itself – high or low – impacts corporate strategy, learning, aspiration levels, and future performance. It is evident that the competitive dynamics of the industry and growth prospects with new technologies can be decisive. For some winning companies, the prospect of immense profits is real. In the United States, for instance, studies show stark changes in the allocation of capital within the firm, especially with the rise of conglomerate corporate firms in multiple industries, technologies, and product lines. More American firms are diversified into unrelated products and technologies, often with a financial arm like GE Capital at General Electric or GMAC at General Motors. Operational risk in executing overall strategy-making can be extraordinarily high.

In response to structural change in these diversified firms, C-suite executives introduced internal measures of rationalization by plant closings, cost-cutting, and offshoring to countries with cheap labor costs, notably China, thus vastly changing the employment and labor market, with consequences like high income inequality. The C-suite increasingly allocated capital with free cash flow for distribution to shareholders, with an ethos of “maximum shareholder value.” To quote one study (Reference LazonickLazonick, 2022a, p. 15):Footnote 10

defining superior corporate performance as ever-higher quarterly earnings per share, companies turned to massive open market stock repurchases to “manage” their own corporate stock prices. Trillions of dollars that could have been spent on investment in productive capabilities in the US economy since the mid-1980s have been used instead to buy back corporate shares for the purpose of manipulating stock prices. In 1997, buybacks first surpassed dividends in the US corporate economy … these distributions to shareholders came at the expense of rewards to employees in the form of higher pay, superior benefits, and more secure jobs as well as corporate investments in new products and processes.

America’s airlines really do compare badly with foreign ones. European carriers are the best point of reference … air fares are higher per seat mile in America … (and) standards of service are worse …

3 The Evolution of the Airline Sector

For centuries, flying was an obsession for balloonists, kite flyers, and inspired writers, taking cues from the designs of the ultimate Renaissance man, Leonardo da Vinci. He was proficient in many fields, including mathematics, architecture, astronomy, and botany, so his early designs followed the anatomy of birds – their size, weight, wingspan, movement in high winds, and their capacity to land on a tree or open land. His helicopter model with its aerial screw, a flying machine, and a light hang glider provided lessons that are current even today, including ideas about production from wood, paper, reeds, or taffeta (see Figure 3). Da Vinci’s illustrations show the aeronautical changes of a plane’s weight, wingspan, length, cargo, and capacity to lift off the ground, and he also understood elements of the scientific method, with its need for trial and error, and the potential for failure.

Figure 3 Leonardo Da Vinci’s hang glider.

On December 17, 1903, two brothers in America took flight in their piloted plane called the Flyer 1, with a wingspan of 40 feet, length of nine feet, and a weight of 750 pounds, and powered by a handmade 12 hp cylinder engine. Orville and Wilbur Wright received headline news around the world. This feat started a new form of transportation that would lead billions of customers to fly to distant destinations from their own communities. All aspects of flying would encompass innovation – small and incremental or large and pathbreaking - from clothing and eye protection of pilots to the shift of dual controls for pilot training, to new landing gears by which planes could land on snow or water, to new instrumentation, giving planes and pilots a capacity to fly higher, longer, and with improved benchmarks of safety.

During the following decades, airlines were in their infancy. All planes flew at low altitudes, because weather conditions like high winds, rain, and snow, and air sickness, common even among seasoned pilots, were travel barriers. The arrival of automobiles in North America and Europe, as well as trains, made air travel an expensive proposition, with fewer than 6,000 passengers in 1929, but over a million a decade later in America. Perhaps the first scheduled commercial flight took place in Florida on the 23-minute run from St. Petersburg to Tampa beginning in 1914, with planes flying at altitudes as low as 50 feet over Tampa Bay. In 1925, the Dutch airline, KLM, flew the 8–12-seater Fokker F.VII, manufactured in Holland, on an inaugural flight from Amsterdam to the Dutch East Indies. In 1927, Pan American introduced its first international flight schedule, from Key West, Florida to Havana, with the same aircraft, the Fokker F.VII.

The history of aviation parallels the story of engineering innovation, whether small and incremental at first, like the deicing tools and fluids needed to prevent ice accumulation on plane wings, or bold and transformative later on, like powerful jet engines or large, double-aisle models for long flights. The entrepreneurial bent of designers, pilots, and financial backers enhanced the innovative atmosphere and culture of their time, a trait that continues in the twenty-first century. Consider the lessons of a key benchmark that took place in Paris almost two decades before the Wright brothers flight in America, when two French flyers, Jacques Charles and Nicolas-Louis Robert, flew their hydrogen balloon to an altitude of 1,800 feet, and traveled more than 22 miles. Daring pilots wanted to fly longer distances, at higher altitudes, including over water. In 1919, two British pilots, John Alcock and Arthur Brown, flew their twin-engine Vickers Vimy, carrying a small amount of mail, across the Atlantic from Newfoundland to Galway, and were awarded a prize by Winston Churchill.

However, more long-distance flying gave concerns to governments who worried about the danger if a plane had engine failure or ran out of fuel. In 1936, the US Bureau of Air Commerce, a precursor of the FAA, introduced a rule known as ETOP, an acronym for Extended-range Twin-engine Operations Performance Standards, where aircraft had to fly within 100 miles of the nearest airport. Changes made in 1950 extended the rule to a 90-minute diversion to the nearest airport. The introduction of jet engines allowed Boeing also to change the rule so that jet aircraft could fly across the Atlantic or the Pacific Ocean. Today, air travel has three legs – the planes in the air, the airlines who operate them, and the airports with several passenger terminals, runways, and state-of-the-art navigation systems.

Airline Models and Design

Like oceangoing ships, airplane design and productions require an understanding of the intricate physics of weight, height, distance, and the speed of the plane itself. These engineering challenges required design systems for takeoff and landing at different speeds with a heavy payload in all sorts of weather. Air travel was once short-distance flights, limited mainly to the social and political elite. Today, billions of customers are regular fliers on long-distance flights, thanks to innovations like Boeing’s 707, its first commercial jet airplane, launched in 1958.

From the days of the earliest fliers in America, Europe, and Japan, and during trench warfare in World War One, small biplanes and other forms of propeller-driven aircraft were developed and tested. Initially the crew was a single pilot, but later, planes had dual controls for military purposes like reconnaissance and attaching skis to land on snow or water. In the postwar environment after 1918, interest in the technology advances of small airplanes, including production of zeppelins and glider planes, became more advanced. As military establishments built their own planes, entrepreneurs saw the advantages of air travel for speed and distance. In fact, in Europe and Canada, governments established their own national airline carriers, a pattern followed by most countries across the globe. In America, OEMs and airlines led the expansion of air travel, especially when governments issued contracts to deliver the mail – a historic replay of the steady growth of the Cunard Line, started by a Canadian, Samuel Cunard, to transport mail by ships from London and Liverpool to Halifax and Boston in the 1880s.

World War Two had a profound impact on all aspects of aviation technology, from smaller aircraft, like Japan’s Zero fighter and British spitfires, to heavy long-range bombers like the Lancaster, to high-speed rockets. In America, firms like Douglas Aircraft designed the famous DC-3, a low-wing, twin-engine aircraft first flown in 1935, and later produced in massive volumes (13,000 by 1945 when production ceased). The DC-3 was easy to fly, could land or take off on a short runway, and had a cruising range of 2,100 miles. The DC-3 saw action in both Europe and the Pacific theatre, and was also licensed to the Soviet Union. The plane was used for transport, paratrooper action, medical aid for wounded troops, and cargo of all descriptions, and was easily adapted in the Normandy invasion to become a flying glider flying at a speed of 290 miles per hour. Many DC-3s are still flying today.

The transition to commercial jet aircraft was a bold financial risk when Boeing took the lead against American rivals like Douglas Aircraft. The 707 became the basis of the firm’s jet product suite of fourteen models with five “families” of planes, sharing many design features, like cockpits, landing gear, avionics, and in-service facilities. Before the beginning of the deregulation phase, Boeing’s market share expanded with a production of 60–80 planes delivered, plus service work for planes in use with a life span of 25 years. In total, Boeing employed almost 200,000 people, with annual sales steadily climbing to reach $52 billion in 2000 and a market cap of $58 billion.

By the end of the 1960s, America’s consumer spending was slowing, in part because the United States was now more enmeshed with troops and air power in the Vietnam War. In Washington, Congress and the White House faced the classic spending choice – guns or butter. As the cost of defense spending climbed, the government in Washington looked for cuts elsewhere. The United States’ Supersonic Transport ((SST) program, initiated and funded by the FAA, had an aim to build an aircraft with 2,000 passengers that could fly at Mach 2, twice the speed of sound, on long-distance flights across the United States or across the Atlantic. The manufacture of supersonic aircraft was a technological challenge, requiring advanced materials for the airframe, fuel-efficient engines for high speed, and new forms of avionics and instrumentation. Congress provided research money for firms like Boeing, and the cancelation led to massive work layoffs. Interest in SST high-speed travel came from the very top. President John F. Kennedy had issued a call to land a man on the moon and bring him back, and so he introduced the United States’ Supersonic Transport program in 1963, with the Federal Aviation Administration in charge. This initiative prompted firms like Boeing to reconsider their own plans, including feasibility studies of supersonic air transport. Other countries had their own programs, led by a European consortium with the Concorde, and the USSR with the Tupelov Tu-144 program.

The US military remained skeptical, and so did many members of Congress. One senator, William Proxmire from Wisconsin, was an outspoken critic, with a reputation for exposing wasteful military spending, and he opposed supersonic transport as well as space exploration, and called for cuts to NASA (for background, see Reference BrumbergBrumberg, 1999). When the program was canceled, Boeing and its partners had yet to produce a working prototype. In Seattle, the layoffs – which locals called the Boeing Bust – had severe consequences, with no orders from domestic airlines, and only a few from foreign airlines. Boeing had borrowed a billion dollars to initiate work on the 747 model, but no bankers would provide additional funding. Commitments made to the SST program had drained the firm’s cash flow, and layoff costs were high – hourly workers went from 40,000 to 15,000, engineers and scientists from 15,000 to 7,500, office staff from 24,000 to 9,000, plus managerial cuts. Top executives had pay cuts of 25 percent. Unemployment in Seattle soared to 13.8 percent against a national average of 4.5 percent. As house prices fell in value, two real estate agents rented a space on a billboard near the Seattle airport with a telling notice: “Will the last person leaving SEATTLE – Turn out the lights.”

However, even before Boeing had taken a leadership position with its suite of commercial jets, the airline industry had its own forum to discuss future planning. Started initially by the CEO of TWA in 1937, a group consisting of the top executives from leading American airlines, OEM manufacturers, and defense contractors and known as the Conquistadores del Cielo – conquerors of the sky (Reference PetzingerPetzengi, 1996). Senior executives met in an all-male gathering at A Bar A Ranch, a 100,000-acre spread in southern Wyoming. It was a fitting name for those in attendance, an informal gathering to relax, spending time on innocuous pastimes like trapshooting, horseback riding, and poker, while feasting on buffalo burgers, prime rib, trout pâté, and smoked bacon.

It was also a secretive gathering, a place to share experiences, propose alliances and mergers, and assess technological advances and government policies. Contrary to public understanding, airlines were never that profitable, and one of the reasons airlines had public ownership was that for social reasons, airlines served small, local communities. In financial circles, there was a running joke: the way to make a million dollars is to start an airline capitalized at $100 million. For executives who crave winning and hate losing, the gathering was a convenient way to collect insights into the future of the aviation industry.

The Paths to Deregulation

Around the world, airlines operate like many capital-intensive utility sectors, for example electricity-generating stations, railroads, telecommunications, the post office, and subways. In America, many utility sectors are privately owned, but government regulation is extensive, particularly on prices. Regulation can take many forms, given public concerns about public safety (airlines and nuclear power plants, or monopoly telecommunications firms), cost (pricing of postal stamps), nationalist policies to force cargo operators to use American workers to ship cargo between American ports (the Jones Act, still in existence), and business cycle issues leading to market fluctuation and price volatility (subsidies for dairy farmers).

The 1970s was a period where market solutions, not government regulation, converged with action to improve airline travel. The academic field of industrial organization came into its own as a subfield of microeconomics, with models like S-C-P (structure, conduct, performance) and the impact of industry regulation on firm performance. A celebrated article by George Reference StiglerStigler (1971), a Nobel laureate at the University of Chicago, entitled “A Theory of Reregulation” sets out the potential of regulatory capture, a process by which leading firms in a sector help formulate terms of the regulatory regime that favor incumbents. A succession of books and papers, informed by data beyond financial issues, such as accidents, takeoff and arrival delays, and canceled flights, focused on the airline sectorFootnote 11 and provided insights to Congress, led by the forceful leadership of US Senator Ted Kennedy from Massachusetts. The Congressional appointment of a strong deregulation advocate, Alfred Kahn, the new Chairman of the Civil Aeronautics Board (CAB) with government powers to award “certificates of public convenience and necessity,” was a signal of massive disruption.

Congress passed the Airline Deregulation Act, which then was signed into law by President Jimmy Carter in October 1978, and it removed CAB authority over fares, entry, and exit. After a short transition, the CAB was sunsetted in December 1984 and approvals for authority over mergers and acquisitions went to the Department of Transport (and since 1989, to the Department of Justice). America was not alone in the deregulating path, but it was the first. Canada, Britain, and some European countries followed, but these countries also deregulated other sectors such as financial services and telecommunications. In Britain, deregulation was a disruptive change for a state-owned airline, where a merger of domestic airline firms, such as British Airways, formed in 1974 from British Overseas Airways Corporation and British European Airways, plus two regional carriers, Cambrian Airways and Northeast Airlines. The impact was dramatic, immediate, and a game changer. Many airline executives had deep misgivings about this new policy, and in America, the only strong advocate was United Airlines.

Three changes quickly followed from deregulation: new startups, horizontal mergers, and consolidations. As many executives of top airlines privately predicted, the ten incumbents (American, Braniff, Continental, Delta, Eastern, Northwest, Pan Am, TWA, United, and Western) lost market share, declining from 87 percent to 75 percent, with new competitive rivalry coming from smaller, regional airlines like Frontier, Ozark, Piedmont, Republic, and US Air; intrastate airlines like Air California, Air Florida, Pacific Southwest, and Southwest; and charter airlines like American Trans-Air (ATA), Capitol Airlines, and World Airways. New airline startups included America West, Jet America, Midway, Midwest Express, Muse, New York Air, and People Express. According to Jordon’s (1987) analysis, between 1978 and 1985, the number of airlines using jet aircraft increased from 27 to 62, while Rose and Dahl (1989) saw the second wave increase the number of airlines to 200. (For background, see Reference Goetz and DempseyGoetz and Dempsey, 1989.)

By the end of the 1990s, more competition led to a new period of industry consolidation, with eight airlines having 80 percent market share. Among the bigger players, Braniff, Eastern, and Pan Am ceased operations, and Delta took over Western, leaving a dominant market position for American, Continental, Delta, Northwest, United, and US Air. The third wave coincided with the terrorist attack on the World Trade Center on September 11, 2001, in which two planes from American Airlines and two from United were highjacked and crashed at the World Trade Center, the Pentagon, and a farmer’s field in Pennsylvania. Air travel slowed down precipitously, thus impacting the output of firms like Airbus and Boeing. Terrorism became a new watchword, as airline security around the world meant longer check-in times for boarding, changes to passenger’s luggage and carry-on baggage, and careful security alerts by immigration authorities at destinations.

Elsewhere, state-owned airlines like Japan Airlines and Air Canada negotiated new bilateral agreements to fly to foreign countries in a cooperative system known as “Bilateral Air Services Agreements” (BASA). The skies, both domestic and international, were historically controlled by the governments of the world where this system, focusing on safety, was highly regulated, usually limiting the number of flights, their frequencies, and fares, which could be changed only with the approval of governments.

Two other related but separate technology advances impacted the airlines. Since the early 1960s, computer software and large mainframe computers allowed collection, assortment, and assessment of huge amounts of data on flights, new and repeat customers, and regular routes on a daily basis. Cyrus Rowlett “C. R.” Smith, CEO of American Airlines, was a pioneering thought leader on new forms of data analytics and data mining, including using computers as a new tool to compile an inventory of seats available for each flight. He began a working relationship with IBM to design an airlines reservation system.Footnote 12 Technicians at IBM began work on a system called SABRE (Semi-Automated Business Research Environment), a name conveying a sense of speed and accuracy, with other airlines like Delta and United participating (Reference Copeland and McKenneyCopeland and McKenney,1988). American Airlines was more aggressive, seeing a reservation system as a tool to provide a competitive edge. Other airlines adopted the American SABRE system, which later became more valuable than the company’s net worth.

In Europe, a consortium of airlines led by Air France and Lufthansa developed a reservation system called Amadeus, which was quickly adopted by national airlines across the continent. Other reservation systems emerged, such as Worldspan in 1990, based on joint work by Northwest, Delta, and Transworld Airlines. In 1993, Galileo GDS, a reservation system competing with Amadeus, was financed by British Airways, The Netherlands’ KLM, and United Airlines. With more personal computers accessing the internet, more bookings allowed individual travelers to make their own travel plans, thus vastly reducing the need for travel agents and resulting in a cost savings of about 5 percent for each ticket price. Many airlines upgraded their internal skills and capacities, thus assuring each flight had high high-capacity utilization for passengers and cargo, and better links between estimated demand and pricing tactics, including discounting for flights outside peak hours.

New route structures and global expansion led to another change, alliances among airlines. Perhaps the first occurred in the 1930s when Pan America allied with Panair do Brazil. In 1989, Northwest Airlines, based in Chicago, agreed to a code-sharing agreement with the Netherlands’ national carrier, KLM Royal Dutch Airlines, a privately owned carrier but with a 20 percent minority share held by the Dutch government. Code sharing meant each airline could share passenger reservations on either airline. In 1992, when the United States and the Netherlands signed an open skies agreement, the two airlines, not their governments, could decide the number of flights, their arrival and destination points, and pricing strategies. In January 1993, the US government granted this alliance antitrust immunity – a signal for other airlines to follow novel airline alliances.

Star Alliance, founded in May 1997, would become the biggest, starting with five airlines on three continents: United and Air Canada from North America, Scandinavian Airlines and Lufthansa from Europe, and Thai Airways International from Asia. The five stars represented the five founding members with the new slogan, “The Airline Network for Earth.” It soon expanded to 720 destinations in 100 countries. Rival alliances quickly emerged, like Oneworld and Skyteam. Mergers and bankruptcies impacted the membership of alliances, but so too did strategic and operational issues, fleet configuration, and cooperative agreements, such as cost-saving measures to share maintenance, refueling, and repairs among the membership carriers.

As more customers booked flights for long distances, each airline had to negotiate agreements with its own government to reach treaty agreements with foreign governments to fly into its territory. For airlines in advanced countries like Europe, Canada, the United States, and Japan, the approach was not a contentious issue. Most Western governments in Europe, North America, and Japan cooperated on many bilateral and multilateral issues, including defense and security, ocean shipping and all aspects of transportation, and trade agreements. Bilateral aviation agreements originated at a meeting in Chicago in 1944, one of several agreements for the postwar settlement, when delegates from fifty-four countries signed a convention or treaty. The Convention on International Civil Aviation, known as the Chicago Convention, set the rules for international operation. Aside from establishing the International Civil Aviation Organization (ICAO), an agency of the United Nations, it established two rules that guide aviation across the globe.Footnote 13 The first, called Freedoms of the Air, determined the right of any nation to determine who could fly over or into a contracting state. When the Soviet Union joined, the Kremlin allowed only certain airlines to fly over its vast land territory, including planes from Soviet-occupied states in Europe, China, Cuba, and North Korea but expressly excluded airplanes from Europe, Canada and the United States, Japan, and South Korea.

More countries joined the ICAO, and these bilateral agreements govern the practices of their airlines for flight schedules, cargo, and all aspects of flight operations, such as frequency, pricing, capacity, and customs arrangements. In time, several countries expanded the bilateral conventions to multilateral arrangements, often becoming part of trade agreements, including open skies agreements, such as the treaty between Canada and the United States. Economic growth and rising discretionary income meant a remarkable increase in the number of passengers, and new business models for low-cost airlines, an increase in the number of routes, and expansion of airport terminals, despite new trade tensions over air space.Footnote 14

However, other factors influenced the airlines sector, including the ever-rising cost of fuel, consumer worries about foreign wars in Iraq and Afghanistan, and the pricing for long-distance tickets. Financial losses rose steadily, reaching an accumulated $35 billion by 2005, and six airlines went into bankruptcy protection. The low-cost carriers thrived, led by Southwest and later Jet Blue, unencumbered by the high-cost structure of legacy incumbents, and remained profitable. For example, in the period from 2009 to 2017, based on financial data from annual reports, net margins of United, Delta, and American averaged 4.6, 5.8, and 2.8 percent, and often negative for some years, while Southwest’s net margins averaged 8.4 percent, but much higher for the years 2015–2017, at 11.0, 11.1, and 16.5 percent. They became a model of new startups elsewhere, like Ryan Air and EasyJet in Europe and WestJet in Canada, thereby increasing global seat capacity to 500 million, often concentrated in the peak travel months of summer, December holidays, and school breaks in the spring.

As deregulation became the established policy framework, airlines had to adjust their business models, which in turn impacted Boeing and other OEMs. It took time to see the impact on industry structures, such as the size and number of firms, their product offerings (short-distance and long-haul flights), and the competitive dynamics within national markets. In the United States, American Airlines pioneered a hub-and-spoke model, using smaller planes like the 737 from smaller cities to the main airport in Dallas/Fort Worth in order to fill bigger planes like the 747 for long-distance routes to Europe. American was the first to create loyalty programs, where customers would gain points for future flights. Today, frequent flier programs are standard in the airline sector, and copying is occurring in other sectors like retailers. For each airline, a network of routes is key to their business model, which includes the choice of OEM models to fly (short haul vs. long distance, narrow-bodied or wide-bodied aircraft). In fact, some major airliners don’t carry passengers. Instead, they fly cargo, like FedEx’s large fleet of over 700 dedicated cargo planes like Airbus’s A-380, Boeing’s 757, 767, and 777, and smaller aircraft like the Cessna and the French–Italian plane, the ATR-72.

In America, many airlines became complacent, knowing they could raise money in the capital markets to purchase planes, often via leasing. Yet not all investors were impressed, including Berkshire Hathaway’s Warren Buffett.Footnote 15 However, as many foreign governments began to privatize government-owned airlines despite fierce domestic opposition, legitimate concerns arose about safety, customer service, and foreign ownership. So, governments also strengthened their regulatory authority on issues of direct concern to the public, such as aircraft safety. Further, they also changed their approach to designing, managing, and operating their airports, including using more runways, passenger terminals, and navigation systems. After the 9/11 terrorist attack, airlines outside the United States upgraded their security systems, including items not allowed in carry-on baggage and luggage – guns, firearms, drugs, and certain foods. Major airports around the world set up a trade association in 1991, called the Airports Council International,Footnote 16 to learn best practices and exchange policy ideas on safety, environment issues, and security.

Novel business models forced the main OEMs, Boeing and Airbus, to reconsider their product-market strategies. Boeing had already opened the door to jet service with its 707, followed soon after by Douglas Aircraft’s new model, the DC-8, inaugurated after FAA certification by Delta Airways in September 1959. Boeing’s commitment to devoting huge time and resources for the 747 design, with more than double the number of seats of the 707 or DC-8, was a strategic bet on the future, with a large, wide-bodied model carrying more passenger seats and cargo. Rivals quickly followed, like Lockheed Martin’s L-1011 Tri-Star, but there were also consequences for airports, which varied by size (number of passengers), location (near built-up areas in major cities), capacity, and international navigation systems (Figure 4).

Figure 4 Strategic mapping: business model in the global airline industry.

Ironically, the biggest impact was in Europe, not America, where both airlines and transport policies led to lower fares, more competition, and high levels of service (including other transportation options, like high-speed rail). Deregulation had changed the calculation to manage a fleet for long-haul flights and short-distance, combining high utilization per plane and high occupancy per flight. The emergence of new, low-cost airlines exacerbated management issues for larger companies with larger fleets using wide-bodied aircraft, smaller and more fuel-efficient planes like Boeing’s 737 or Airbus’s A-319, or even smaller models (fifty to ninety seats) made by Embraer in Brazil and Bombardier in Canada. Measured by performance benchmarks such as fares per seat mile and profits per passenger, America’s airline sector remained an oligopoly; despite mergers and consolidation, four airlines accounted for 80 percent domestic market share – with higher fares and higher margins and profitability than Europe, more than double by comparison. Further, despite the deregulatory environment, US laws on foreign ownership remain more restrictive, allowing only 25 percent foreign ownership compared to 49 percent in the EU.

For each airline, a network of routes is key to their business model,Footnote 17 which included the choice of OEM models to fly (short haul vs. long-distance, narrow-bodied or wide-bodied aircraft). For each airline, the business model included the calculationFootnote 18 of estimated passenger (and cargo) demand, per month and per year, and a sequential series of activities for the airline, the plane manufacturer, and the local airport. In the post–9-11 travel environment, airport security provides more passenger safety, but also more delays (enhanced by the COVID-19 pandemic), thus interrupting route networks, based on arrivals and departures. As International Air Transport Association (IATA) predicted, domestic flights declined by 70 percent and passenger revenue declined by $314 billion once the COVID-19 virus spread worldwide. Airline travel declined precipitously and set off a cascade for fewer delivery orders, fewer production requirements, and less work for subcontractors.

Deregulation accelerated the time for new designs of planes, thus reconfiguring the third leg of the industry, airports. Airports consist of four features: land and real estate, runways, terminals for passengers and cargo, and maintenance facilities, including fuel storage. Airports face new challenges, such as 24/7 security, customs clearance, and facilities for emergency equipment for weather conditions. These factors impact the landing fees and cost per plane. In many cities, airports faced governance challenges, such as the NIMBY problem of local citizens not wanting expansion, with public fears of traffic congestion and high decibel count or noise of jet engines. Revenues come from landing fees charged to airlines, and the rents as a landlord for bars, restaurants, and other amenities. In the end, airlines face a range of costs even when the planes are sitting on the ground, and they asked, as they reconfigured their high-cost fleets, could they afford the capital cost of fleet expansion?

The Sales Commitment and Dawn of Leasing

For airlines in America, whose shares were listed in a public exchange, raising capital to expand their fleets was only one strategic factor in their growth strategy, as were new destinations, often to foreign countries. However, for new startups, or legacy government-owned carriers, fleet expansion also presented a strategic challenge – the need to replace aging airplanes, such as the 727, with new planes at a cost of about $150–200 million per plane (and even more if spare engines were included).

In the decade after US deregulation, aircraft production increased to about 392 per year, up from 315, while airlines retired 285 planes per year. Aircraft leasing became a financial tool widely employed by the auto OEMs, such as GM’s leasing division, General Motors Acceptance Corporation. The growing airline sector was a novel customer base in the new highly deregulated banking sector and provided aggressive financial service firms like GE Capital and many others an opportunity, often with many tax advantages. It was a new era in global financial services and the dawn of a new asset class, aircraft leasing. Other firms emerged, such as Aerolease International, Polaris Aircraft Leasing, General Electric Capital Corp (GECC), and Guinness Peat Aviation (GPA), which offer airlines an easier form of financing for the full life cycle of each plane model.

The emergence of so many new airlines led to a steady expansion of plane leasing and forced negotiation of a new international agreement, the Cape Town Treaty, which now involves 73 countries including the European Union. The Cape Town Treaty refers to the Convention on International Interests in Mobile Equipment, and its Protocol on Matters Specific to Aircraft Equipment. It established an international registry for airplanes and helicopters, as well as a civil aviation registry as the authorizing entry point for requests to change ownership and to record engines and aircraft as collateral for unsecured payments. (Russia’s invasion of Ukraine had many secondary consequences. Many planes operating in Russia with leasing contracts with Western firms became subject to seizure as part of the sanctions package imposed on the Russian government, Russian firms and oligarchs, and their offshore holding companies.)

Starting in the 1980s, leading airlines worked closely for a three-way cooperation of the ecosystem of airports – airline manufacturers, airlines, and airport authorities – plus the flying public to confront the politics of infrastructure, the NIMBY effect against charges of traffic congestion, noise levels, related costs like subway extension, and acquiring more land for new, longer runways – see Figure 5. Often municipalities prefer expansion, with hopes for a multiplier effect on tax revenues, but overstate the benefits and underestimate the costs. Airlines want the extra services of airports, such as more and better runways and equipment for adverse weather conditions, while demanding lower landing fees.

Figure 5 Two models addressing the politics of infrastructure like airports.

In reality, airports and the larger ecosystem organization have grown immensely in most advanced countries. Their sheer complexity based on 24/7 flights and numbers of passengers parallels the technical complexity of the aircraft, and the need to manage so many activities concurrently. These competencies include navigation aids, fuel storage, and weather-related equipment for cold temperatures, with some dedicated to passengers-only, cargo-only, and, rarely, military flights (e.g., Frankfurt in Germany). Yet airline safety worldwide is remarkably high. The number of fatalities per billion passenger miles for automobiles is 7.3 and for train facilities is 0.43, but for airlines only 0.07, with accidents happening on the ground, not in the air.

If America wishes to close the technology gap with Europe, all she needs to do is erect 51 different sets of customs barriers, tax systems, space and defence programs, science policies, and public buying arrangements: the gap will be gone in a year!

4 The Boeing and Airbus Duopoly

Duopolies, where two firms dominate a sector, represent a challenge for economists, policymakers, and politicians who face voters’ wrath due to bad service, high prices, and lack of health and public safety. The vast literature in academic journals focuses on markets that are oligopolistic (a few firms) and closer to the ideal of perfect competition with many firms.Footnote 19 Duopolies provide a test case for antitrust, collusive behavior, such as setting prices above average costs and using a range of nonprice rivalry activities like advertising, brand building, and others. Well-known duopoly examples include GE and Westinghouse in advanced turbine engines, Kodak and Polaroid in cameras, and Matsushita and Sony in consumer products. Clearly, a duopoly exists in many local markets (two gas stations or two pharmacies, for example), but customers and local governments accept such conditions because their presence shows the limits of small market size.

However, the presence of duopolies in some sectors raises questions about market performance and market structure. The celebrated duopoly case study is the carbonated beverage sector between two American firms, Coca-Cola and PepsiCo Inc. which together control about 75 percent of the market using advertising, product-like extensions, and a focus on demographic segments. A more complicated duopoly is the case of Boeing and Airbus, which dominate the manufacture of commercial planes, with each offering a “family” of models based on price, seat and aisle architecture, overall size and mileage range, and number of engines (Reference SimonsonSimonson, 1968).

Mainframe aircraft production involves a complex organizational process, similar to other HROs like nuclear power plants, submarines, teaching hospitals, and space aircraft. By definition, HROs operate in a complex internal environment where human, technical, and organizational features interact and where accidents from defects and misjudgments might be expected to occur frequently. Complex and intricate tools of prevention, redundancy, and defect-free quality can help minimize failures, simple or complex, but occasionally can still lead to catastrophic failure. In aircraft production, complications arise from the need for tightly coordinated alignment of different airframes, avionics and guidance systems, and on-board facilities including seating and cargo arrangements. Such alignment requires demanding and precision work procedures undertaken by a very competent and well-trained workforce with more engineers, scientists, and highly skilled technicians.

Today’s generation of jet aircraft illustrates the centuries-old lessons gleaned from oceangoing ships. Several socio-technical units work together concurrently, dealing with the body of the plane and its strength and safety at high altitude, plus the stresses of landing and takeoff where the engines and fuel supply have the power to carry a heavy load over vast distances with little chance of a stall; landing and braking equipment to control the plane’s takeoff and landing; and technologically sophisticated avionics for pilot control of the plane’s multiple functions in threatening weather conditions.

The rivalry between Boeing and Airbus comprises the extent of aerospace supremacy around the world, personal animosity between rival executives, and the divided loyalties of leading subcontractors like engine manufacturers who want to serve both companies (Reference NewhouseNewhouse, 2007). These competitive dynamics, exacerbated by the long lead times from product design to completed manufacturing and certification, extend to the airlines’ demand for certain aircraft models that provide market power to the OEM manufacturers on price, date of delivery, and price discounts for large orders. Both firms also face China–US geopolitical tensions and China’s desire to enter the aerospace sector. In some respects, airlines had shifting preferences for certain models, giving these airlines a temporary advantage in serving high-volume routes for passengers and cargo.

For Boeing, which once had a commanding market position, internal dysfunctions and relocation of corporate headquarters twice have tested the firm’s competitive position. In 1990, when Airbus announced plans to design an aircraft model of 600 seats or more, the A-380–100, in part because of high congestion at airports like Narita in Tokyo or Heathrow in London, Boeing’s tactics took several turns – as a partnership, as a direct rival, but also to thwart Airbus’s development project. Thirty years later, Airbus was no longer a publicly supported national champion, or a job-creation subsidy machine decried by many Americans, including those in Congress and US airlines.

Boeing and Airbus and other OEMs like Embraer, Mitsubishi, Bombardier (acquired by Airbus), and China’s COMAC, addressing customer demands, have dramatically improved the design systems for each plane model, thanks to the wonders of computer systems (for simulation, forecasting, and stress testing of materials), digitization, and multidisciplinary teams. New models are no longer the effort of the firm’s diverse engineering team acting alone. Even small OEMs must apply a collaborative effort with airline customers, leading experts in airports and terminal operations, the regulatory bodies, and financial teams who understand the very long lead times for design, actual production, and the certification process before delivery to the airlines.Footnote 20

Each plane model has a minimum life span of twenty-five years and is designed to meet safety standards of no-risk flight expectations and to fly in adverse weather conditions.Footnote 21 Jet-powered aircraft require a manufacturing alignment of some five million parts and components and software, for the mainframe body structure, the wings containing fuel tanks, powerful engines, advanced avionics for instrumentation, braking systems, landing gear, and takeoff tools that guide the pilot, and all aspects of fuel, storage, and fuel consumption. The plane cockpit is a technologist’s dream – an assembly of dials and mechanisms to control all aspects of the plane on the ground, in the air, and ready to land, and is fitted for all sorts of emergencies, including landing on water.

For Boeing, the 747 jumbo model was a game changer; a reinforcement of the firm’s technological edge, it became a movie star, serving as the setting for over 300 films, as well as the model for the US presidential plane, Air Force One. However, as documented in several historical accounts, the 747 was truly a “bet the firm” gamble for the company. The 747 began with some specifications from Pan American Airlines, with a length more than twice the size of the 707 to allow scale effects of lower costs per passenger. The plane’s design was revolutionary, with its overall size, its four-engine thrust, and its customized components like the cockpit, the sixteen-wheel landing gear, and the wing span containing the fuel tanks all specifically designed for long-distance flights – New York to Tokyo or Singapore to London. Its sheer scale would require new designs for emergency evacuation doors and chutes, fuel tanks, and powerful engines, for a takeoff weight of 378 tons (833,000 pounds), with an unheard-of range of 4,620 to 6,560 nautical miles (8,560 to 12,150 km).

Airline safety was a concern of both passengers and the airlines, so Boeing engineers and technicians worked on manufacturing tools for reliability, redundancy, and fail-safe mechanisms on everything for landing gears, maintaining flight with an engine failure, and all aspects of the hydraulic systems. New design features also include measures for redundant hydraulic systems, a quadruple main landing gear, and dual control surfaces. The 747 forced Boeing engineers and technicians to introduce novel methodologies and techniques first applied to military aircraft, such as integrated systems for fault-tree analysis to determine where the failure of one part could impact the total system.

Fault-tree analysis (FTA), developed in 1962 at Bell Laboratories and supported financially by the US Air Force, was adopted for intercontinental ballistic missiles and applied by Boeing in its Minuteman missile program in 1963. The system became widespread in civil aviation and other sectors, like nuclear reactors, pharmaceuticals, and civil engineering, which apply failure probability criteria for risk management. By 1970, the FAA had brought in new regulations on air worthiness which adopted failure probability criteria for aircraft production and certification, and later were extended to air traffic control and the US National Airspace System.

As planning for the 747 was underway, it soon became obvious that existing plants couldn’t accommodate the sheer size of the plane. After a feasibility study of fifty locations, Boeing used its own supervisory team to oversee the construction of the Everett plant, one of the world’s largest, on a 780-acre plot located near a military base at Paine Field, thirty miles north of Seattle. Boeing’s design team, getting constant advice from Pan American Airlines, knew the 747 would be more than a passenger model, so its raised cockpit could allow a forward cargo door for conversion to freighter use. During its lifetime, the Boeing 747 was constantly upgraded and had various combinations – passengers-only, cargo-only, or a combination usually set by the airline customer.