In this book I argue for a radically1 new understanding of the ethics of business enterprises or “corporate responsibility” in the global and pluralistic context. This perspective is new in combining three crucial respects. First, business enterprises as primarily economic entities are called to pursue the creation of wealth in a comprehensive sense that is beyond maximizing profit or adding value. Second, business enterprises operate in an increasingly interconnected world. They consist of human beings and affect human beings from the local to the global level. To evaluate their impact, we have worldwide standards stipulated in international agreements: the human rights including civil, political, economic, social and cultural rights and the right to development. With the United Nations Framework (UN 2008a) and the United Nations Guiding Principles on Business and Human Rights (UN 2011), business enterprises – in addition to states – have become accountable in a new way for their impact on human rights. Third, in this interconnected world not only individual business people but also business enterprises as organizations2– independent of the duties of states – now carry moral obligations regarding human rights. This means that moral (and not only legal) obligations are attributed to organizations understood as moral actors (but not as moral persons). Based on this theoretical underpinning, moral responsibility can be attributed to corporations in a genuine sense.

In this new approach, the ethics of business enterprises can be summarized as “corporate responsibility for creating wealth and respecting human rights.” Creating wealth is conceived in a comprehensive sense with seven features. Moreover, it relates to all internationally recognized human rights. Before explicating this new understanding, I will outline the broader context in which the ethics of business enterprises should be situated today. It is characterized by three key terms: globalization, sustainability and financialization (see Chapter 2). As globalization is a main feature of our situation on the planet Earth today, sustainability proposes to us the direction in which we ought to move and financialization indicates a profound and challenging transformation of the economy with far-reaching consequences for society. All three perspectives underline the need for a new understanding of corporate responsibility that calls for an extensive variety of innovation at multiple levels.

“Corporate responsibility for creating wealth and respecting human rights” will be developed and explained in three parts. In Part I, I take a macro-perspective, applicable nationally and internationally, on the economy that is the primary interface between “business” and “society.” This economic approach is an “ethics-related approach” in the sense proposed by Amartya Sen (Reference Sen1987), which is broader than a “value-free” logistical (or “engineering”) approach, by including human motivation and the judgment of social achievements. It goes beyond the “creation of wealth” – in line with and beyond Adam Smith – by offering a broad and comprehensive definition of wealth and by revealing many dysfunctional features of the current economy. In Part II, I switch to a normative-ethical perspective by identifying internationally recognized human rights as minimal ethical standards. Given the globalizing economy, universal minimal ethical standards are indispensable for living and working together on Earth. They are conceived as global “public goods,” using the precise term developed in the first step. Although human rights are being violated in multiple ways, they are the only worldwide recognized standards and, in addition, provide space for a large diversity of acceptable ethical and cultural values. After arguing for wealth creation in a comprehensive sense and the relevance of human rights as global public goods, in Part III, I draw the implications of this broad view for corporate responsibility that pertains to all types of business enterprises worldwide. As primarily economic organizations, business enterprises are held responsible for creating wealth that includes seven features. And, consisting of and affecting human beings, businesses have to respect all human rights and, when faced with human rights violations, remedy them.

Seven Features of Wealth Creation

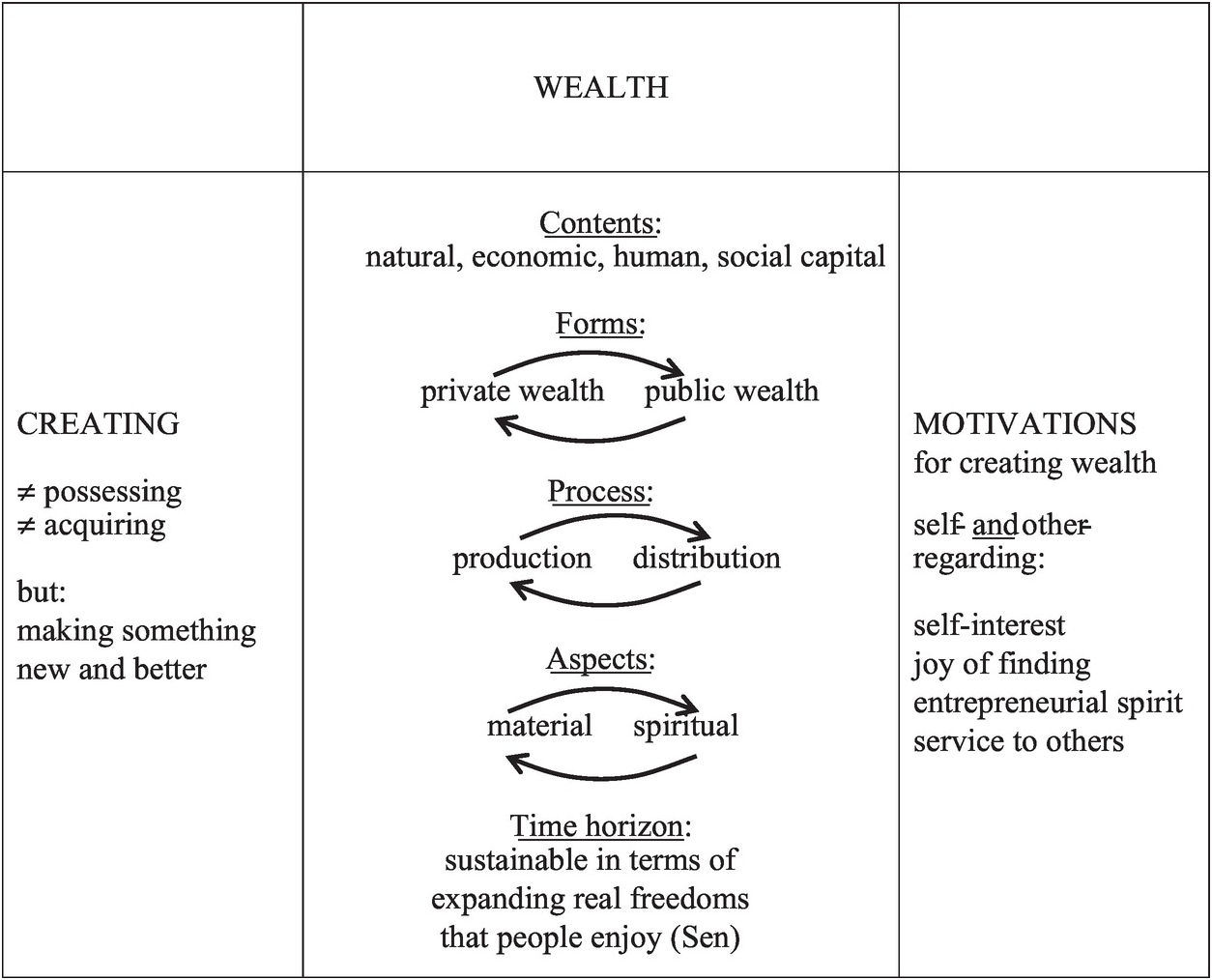

Part I presents and explains a comprehensive conception of wealth creation that includes seven features. This stands in stark contrast to the dysfunctional aspects of national and international economies. Anglo-American capitalism, with its far-reaching impact on the global economy, focuses heavily, if not exclusively, on the accumulation of financial wealth. As well articulated in the Encyclical On Care for Our Common Home by Pope Francis (2015), the dictates of maximizing shareholder value recklessly destroy the natural environment. Widespread corruption and bribery impair the economies of many countries. People still suffer from extensive illiteracy and the lack of appropriate training. They get sick and die from unhealthy working conditions, air and water pollution and other deleterious conditions and the lack of decent health care. Trust in the financial services industry and in consumer relations with banks has been seriously undermined and hampered. All these problems indicate the loss of natural capital, economic capital, human capital and social capital. Therefore, the comprehensive conception of wealth creation includes, as a first feature, all four types of capital, which form the substantive contents of wealth (see Chapter 4). Figure 1.1 provides an overview of this rich conception of wealth creation: the middle column shows the first five features, the left column indicates the sixth feature and the right column refers to the seventh feature.

Figure 1.1 Wealth creation – a rich conception

A second feature of wealth proposes different forms of capital, meaning formal as distinct from substantive aspects of capital (Chapter 5). It can be best understood when we look at the wealth of a nation. National wealth is not just an accumulation of private wealth, but also consists, in large part, of public wealth. Thus the wealth of a nation is a combination of private and public wealth. While private wealth is easily perceived and understood, public wealth is harder to discern and is often ignored, although it is essential for producing private wealth. For instance, we may remember how in the Great Recession in 2008–09, the instability of the financial system seriously hurt the global economy and societies around the world. Or we recall the positive impact of a country’s fair and effective rule of law on foreigners to invest in this country. Using the economic distinction of private and public goods, public wealth differs from private wealth by the characteristics of non-rivalry and non-excludability. It is noteworthy that this is a formal definition which applies to “good” and “bad” public goods and to wealth and the lack thereof, and therefore needs ethical evaluation (as, for example, climate change does). Wealth in a comprehensive sense includes both private and public wealth, which has far-reaching implications. Markets are powerful for producing private wealth, but fail to generate public wealth, and motivations for public wealth need to be other-regarding, not only self-regarding.

Wealth creation is often conceived as a productive process that is separate from subsequent distribution, according to the saying that one has to bake the cake first before it can be shared. The third feature of wealth creation rejects this separation of production and distribution and claims that the productive and the distributive dimensions of wealth creation are intrinsically interrelated. In fact, the distributive dimension permeates all stages of production from the preconditions to the generation process, the outcome and the use for and allocation within consumption and investment. For too long, the separation between “producing the pie” and “sharing the pie” has marked the ideological struggle between “the right” and “the left,” despite its flawed economic underpinning. Therefore, wealth creation is about wealth distribution as much as about wealth production (see Chapter 6).

The fourth feature of wealth creation rejects a materialistic understanding of wealth that is excessively concerned with material possessions and making money, driven by consumerism, acquisitiveness and greed. Such a materialistic view is too narrow, if wealth consists not only of economic capital, but also of human, social and natural capital. It also cannot consider and account for other features of wealth creation to be introduced below: human capital conceived in terms of human capabilities of being healthy and educated persons; creating wealth understood as making something new and better; and other-regarding motivations for creating public wealth. While this proposed concept of wealth undoubtedly has a material aspect, it also includes a spiritual aspect by relating to the human spirit or soul (regardless of religious beliefs) and/or to religion and religious belief (Chapter 7).

Creating sustainable wealth accounts for the long-term time horizon conceptualized in terms of human capabilities or “expanding real freedoms that people enjoy” (Sen Reference Sen1999) – the fifth feature of wealth creation. Given the multitude of definitions of sustainability, I stick to the “old” proposition from the World Commission on Environment and Development which requires an intergenerational perspective, namely “to meet the needs of the present without compromising the ability of future generations to meet their own needs” (WCED 1987, 7). I further specify this perspective by using the Organisation for Economic Co-operation and Development (OECD’s) definition of sustainability of well-being over time in terms of natural, economic, human and social capital (OECD 2013a), which is congruous with the contents of wealth as defined in this book. This perspective of human capability not only substantiates the meaning of human capital; it also helps to measure the impact of natural, economic and social capital on human beings. Thus, creating sustainable wealth becomes a rich and concise purpose of economic life which transcends the growth of (material) resources by focusing on people and sustaining nature (Chapter 8).

The sixth feature specifies what we mean by the “creation” of wealth. Obviously, wealth creation is more than possessing wealth and differs from acquiring wealth. Possessing adds no value and acquiring only means a change of ownership, which may occur by legal or illegal and ethical or unethical means. In the course of history, colonial powers acquired a great deal of wealth, usually with no regard for legal and ethical concerns, which, by and large, amounted to a redistribution rather than a creation of wealth. In the capitalistic system, the “acquisitive spirit,” “the accumulation of capital,” and the “acquisition of companies” do not entail necessarily the creation of wealth, properly speaking. In a genuine sense, to create is to make something new and better. All three characteristics are essential: (a) It is about making, not only imagining, which is feasible and successful in economic and financial terms. (b) It has to be new, be it a gradual change or an innovation (that is, a radical change in technology, social organization or any other field). And (c) it must be ethical, which improves the well-being of people and sustains nature (Chapter 9).

Finally, concerning the motivations for creating wealth, self-regarding motivations can be powerful for creating private wealth. But they fail in creating public wealth, as sound economic theory tells us. Exclusively self-interested behaviors make collective action (for public wealth) impossible, generate free-rider problems and cannot be coordinated by an “invisible hand.” Rather, when economic activities clearly focus on the creation of wealth as a combination of private and public wealth, other-regarding motivations are equally necessary (though not sufficient). They may take a huge variety of forms such as selfless engagement for entrepreneurial success, love for the mother country, solidarity with the poor and the fight for any cause. In each case the other-regarding motivation transcends self-interest, be it for a good or for a bad cause. Still, like public goods or wealth, other-regarding motivations require ethical evaluation. To sum up the seventh feature, wealth creation needs not only self-regarding but also other-regarding motivations (Chapter 10).

In developing the seven features of wealth creation as an “ethics-related” approach to economics, wealth creation turns out to be not only compatible but also relatable to normative-ethical demands. This macro-economic approach pertains to the entire economy, nationally and internationally, including, but not limited, to business. It is not a “value-free” or “engineering” approach which limits itself to the logistics of end-means relations. Rather, it contains numerous connecting features to ethical demands. Four types of capital provide the relevant contents of wealth and two forms of wealth (public and private) require different institutions and motivations. Social achievements involve material and spiritual aspects and are captured in terms of sustainable human capabilities. Two kinds of motivations – other-regarding as well as self-regarding – are necessary for wealth creation, and ethical evaluation is indispensable to identify good vs. bad public wealth, making something not only new but better, and distinguishing good from bad other-regarding motivations.

Human Rights as Public Goods in Wealth Creation

As indicated at the beginning of this chapter, to develop a rich and differentiated concept of wealth creation is the first step in elaborating an ethics of business enterprises or corporate responsibility. In addition to this descriptive-analytical dimension, we investigate, in a second step, the normative-ethical dimension in order to establish, in a third step, a balanced concept of corporate responsibility that “walks on two legs,” including a descriptive-analytical as well as a normative-ethical side.

I propose to define the normative-ethical dimension in terms of human rights particularly for three reasons (see Part II, Introduction). In the process of globalization, economies and businesses have expanded far beyond national borders and have increasingly been connected internationally in multiple ways. With this expansion comes a growing need for universal normative standards, not only for countries but for businesses and economies as well. Since the Universal Declaration of Human Rights in 1948 the ethical framework of human rights has developed to a widely accepted, though not undisputed, universal ethical framework. Although violated in countless instances around the world, it has no comparable alternatives. Moreover, in the new millennium, the global concern for business and human rights has strengthened considerably. The United Nations Global Compact (UNGC 2000) calls on business to play an active role to help address worldwide challenges, including human and labor rights. The United Nations Framework (UN 2008a) and Guiding Principles on Business and Human Rights (UN 2011) declare all human rights relevant for business: civil, political, economic, social and cultural rights, including the right to development. And the Sustainable Development Goals (SDGs 2015) are shaped, to a large extent, by human rights demands.

In order to relate human rights to wealth creation in a comprehensive sense, we may begin with clarifying four important components of the underlying human rights conception: (1) the scope, (2) the binding nature, (3) the function and (4) the qualification of human rights as public goods, discussed in Chapters 11–14.

First, in common talks about human rights the scope is often limited to civil and political rights (such as the right to freedom of thought, conscience and religion and the right to freedom of association) or to economic, social and cultural rights (such as the right to health and the right to an adequate standard of living) and, furthermore, often excludes certain groups of people.

Easily overlooked is the powerful idea that people have a right to be treated with dignity in all spheres of life and regardless of their nationality, place of residence, sex, national or ethnic origin, color, religion, language or any other status. It matters therefore to emphasize that the International Bill of Rights and the International Labor Organization’s core conventions contain all these rights without discrimination. They apply globally and define the underlying conception of human rights in this book (see Chapter 11).

Second, given the wide range of human rights, one might think this term “human rights” would encompass all ethical norms and values relevant for economies and businesses. However, it commonly constitutes only minimal ethical requirements, distinct from social obligations beyond the minimum and aspirations for ethical ideals (De George Reference De George1993, 184–93). In pluralistic societies, nationally and internationally, human rights constitute the necessary common ethical ground for living and working together and are “the minimum reference point for what the Guiding Principles [on Business and Human Rights] describe as internationally recognized rights” (UN 2012a, 10). As minimal requirements, however, they can open and guarantee a wide space for an immense diversity of cultural and ethical values and norms. Grounded in human dignity and specifying its basic contents, they are all interrelated, interdependent and indivisible and thus do not allow for trade-offs between particular rights. This stipulated conception of human rights draws on philosophical reflections and supports – but is not identical to – the legal conception incorporated in the International Bill of Rights and the International Labor Organization’s core conventions. It goes without saying that to date this universal ethical conception is not legally enforceable internationally; however, it provides guidance for voluntary action and soft law agreements, which may become legal requirements later on (see Chapter 12).

Third, from an economic perspective the fulfillment of human rights (for example, the rights to health and to an adequate standard of living) has often been considered a cost that might be too expensive to bear. On the other hand, the violation of human rights can be also very damaging. Undoubtedly, it is legitimate to ask the question of what costs human rights fulfillments and violations may incur. But a serious cost analysis has to account for all costs, in financial and non-financial terms, imposed on all affected people and entities. Moreover, not only costs, but also benefits should be accounted for, again in their entirety and in their distributional impact. Though not easy to conduct, one may argue that such comprehensive cost-benefit analyses of human rights would likely show beneficial results. Beyond cost-benefit analysis, human rights may be recognized as external constraints or boundaries which should not be crossed. While such recognition is commendable from the human rights perspective, it still can be interpreted as an engineering approach to economics that stipulates a value-free economic calculus of ends and means within these constraints. In contrast, the ethics-related approach in this book proposes the fulfillment of human rights as ends to be achieved by public policies and corporate strategies whereas violations signify failing policies and strategies. Moreover, human rights are also understood as means to pursue these and other ends. For example, the implemented right to education is instrumental and a strong way for creating an innovative and more productive work force (see Chapter 13).

Fourth, in order to link human rights to wealth creation, we define these rights as ethically demanded public goods or public wealth. As public goods, they are characterized by non-excludability and non-rivalry, needing ethical qualification, that is to be ethically demanded. Applied to human rights, non-excludability means that no human being should be excluded from the enjoyment of any human right (that is no discrimination). Non-rivalry implies that the enjoyment of any human right by any person should not diminish the enjoyment of any other human right by oneself or any other person. In other words, no trade-offs between human rights for anybody are acceptable. For example, the right to participate in public life should not impair the right to freedom of thought, conscience and religion, nor vice versa; or the freedom of association should not negatively affect the right to non-discrimination, nor vice versa. Beyond the exclusion of any negative impact, one can argue that the enjoyment of one right may even reinforce the enjoyment of another right. For instance, the implemented right to an adequate standard of living (including food, clothing and housing) can strengthen the fulfillment of the rights to work and education, and vice versa (see Chapters 14 and 18).

The definition of human rights as ethically demanded public goods, obviously, has far-reaching implications. Their establishment and fulfillment cannot be achieved by market institutions; rather, they need collective actions at multiple levels of society beyond the price mechanism of supply and demand. Moreover, the motivations must be other-regarding because self-regarding motivations would fail to fulfill human rights as public goods.

Implications for Corporate Responsibility

Having outlined – in Parts I and II – the purpose of the economy as creating wealth in a comprehensive sense within the normative-ethical framework of human rights, I then apply – in Part III – this broad conception to the ethics of business enterprises. Since the early 1980s, a variety of terms have been used in English and other languages to express what the ethics of business firms may mean: business ethics (in a narrow sense), corporate ethics, corporate citizenship, corporate social responsibility (CSR), called in Romance languages éthique de l’entreprise, etica degli affari and ética de los negocios, in German Unternehmensethik and in Chinese qiye lunli, qiye shehui zeren and shangye lunli. In this book I propose the term “corporate responsibility.” Widely used in theory and practice, it points to a key and complex feature of morality and ethics, is easily translatable into other languages and figures prominently in the UN Framework and UN Guiding Principles on Business and Human Rights (“corporate responsibility” as distinct from the “duty of the state”).

In Chapter 15, drawing on work of the German philosopher Walter Schulz, I define responsibility as “self-commitment originating from freedom in worldly relationships” (Schulz Reference Schulz1972). It contains a bi-polarity full of tension. On the one hand, the inner pole emphasizes the relevance of inner decisions. On the other hand, self-commitment out of freedom has its point of departure and its point of destination in worldly relationships (that is, the outer pole). Responsibility as a relational concept is always “anchored” in one or more actors (who is responsible?), concerns a concrete matter of for what one is responsible and relates to an authority or addressee3 to whom one is responsible (for example, stakeholders, tribunal, spouse or one’s conscience).

This tripartite concept helps to clearly identify the essential components of responsibility. First of all, responsibility is not a free-standing ethical principle (like “Do not harm!”), but must be related to an actor. As actors, we include – as do the UN Guiding Principles – all business enterprises ranging from gigantic global corporations and large publicly listed companies to limited liability companies, state-owned enterprises, family businesses, medium, small and micro enterprises. The world of business is immense. The enterprises not only pursue an enormous variety of activities; they also show extreme differences in size, structure, legal form and corporate strategies. Hence the question: Does it make sense – and if so, how – to expect enterprises to be ethically responsible actors and to speak of corporate responsibility in an authentic sense?

The question has been debated for decades and will be discussed in Chapter 16. I propose to use James Coleman’s sociological definition of actors, that is, to have “control over resources and events, interests in resources and events, and the capability of taking actions to realize those interests through that control” (Coleman Reference Coleman1990, 542). These essential properties call for responsible action and can be attributed to corporate as well as personal actors. In the first case, large, well-structured and powerful business enterprises are conceived as corporate actors that differ from many economic definitions of firms such as production functions, nexuses of contracts, pieces of property or economic mechanisms. Corporate actors can take the forms of communities of people, agents, providers of goods and services or as corporate citizens, that is of collective entities with a primarily (though not exclusively) economic purpose. In contrast, when enterprises lack relatively free-standing formal structures – as micro, small and medium enterprises commonly do – they are not corporate actors, properly speaking, but basically shaped by personal actors such as individual business leaders.

Understanding business enterprises with relatively free-standing formal structures as corporate actors, I ask for their moral status. On the one hand, they are not moral persons who have a conscience and are ends in themselves. On the other hand, they are not amoral actors without the capability of taking actions. Hence we may define them as moral actors in an analogous sense to moral persons: They form collective entities that are distinct but not separated from individual members, having certain spaces of freedom, acting with intention (or at least exhibiting intentional behavior) to achieve their goals and impacting people and nature. As moral actors, they bear “corporate responsibility” and can be held responsible for their conduct in an ethical sense. They qualify as actors at the meso-level of action – as distinct from the macro (or systemic) and the micro (or individual) level. If, however, enterprises (of smaller size) are not corporate actors and hence not moral actors, corporate responsibility pertains to individual persons and groups (that is, at the micro level) who carry this responsibility.

The second component of responsibility concerns its contents or “to be responsible for what,” discussed in Chapter 17. It draws from the macro-perspective developed as wealth creation and human rights and applies to business enterprises in a specific sense. Responsibility for wealth creation pertains primarily to the core activities of the enterprise, while responsibility for human rights consists of “respecting” human rights and “remedying” violations as defined by the UN Guiding Principles on Business and Human Rights (UN 2011).

All seven features of wealth creation matter for corporate responsibility. Regarding the contents of wealth (that is natural, economic, human and social capital), each enterprise has its special focus and must meet at least a minimal level of each capital. For example, increases of economic capital cannot be compensated for by losses of natural capital beneath the minimum. In other words, trade-offs between changes of capital are acceptable only above these minimums (the definitions of which will be discussed in Chapter 18). As for the forms of wealth, enterprises are supposed to create private wealth. However, benefiting from public wealth in many ways, they also should “give back” and contribute to the creation of public wealth, which can occur in multiple fashions and to various extents. As the generation of wealth is assumed to be an interrelated productive and distributive process, enterprises are accountable not only for their production but also for their interrelated distribution – for example, for income inequality in their organizations. Because wealth creation includes not only material but also spiritual aspects, the culture of enterprises should not be dominated by money making and greed. Rather, through creating natural, economic, human and social capital, wealth creation aims at a noble goal that addresses both material and spiritual needs of employees, customers and other stakeholders. Sustainable enterprises adopt a long-term perspective by focusing on strengthening human capabilities – not merely material resources – and sustaining the natural environment. As creating means “making new and better,” enterprises strive for both gradual changes and groundbreaking innovations while considering the ethical implications and respecting the ethical demands, being well aware that innovation by itself can be ethically praiseworthy or repugnant. Finally, the driving motivation of enterprises cannot be exclusively self-regarding because they have to help create public wealth. Other-regarding motivations are required, for public wealth and for human rights.

To further explore the contents of corporate responsibility, we draw on the widely accepted universal ethical framework of human rights and apply, with an ethical underpinning, the UN Framework and UN Guiding Principles on Business and Human Rights. In line with Henry Shue (Reference Shue1996, 35–64), the UN Framework distinguishes three types of obligations to secure human rights: “To protect, to respect and to remedy.” To protect human rights – the duty of states – means to demand recognition of the obligation to avoid violations of human rights and to establish “institutional” provisions that prevent, as much as possible, the violation of this obligation through appropriate incentive and punishment systems. To respect human rights – the responsibility of business enterprises – indicates the obligation to avoid violations of human rights. And to remedy – the obligation of both states and enterprises – refers to the obligation to provide the victims of human rights violations access to the remedy of their rights. In other words, “corporate responsibility” is clearly identified with, and limited to, “respect” and “remedy” without including the states’ duty to “protect.”

What “respect” and “remedy” mean for corporate responsibility is explicated in five foundational principles (FP; see Table 1.1) and eleven operational principles (UN 2012a). These (principles) state that [business enterprises] “should avoid infringing on the human rights of others and should address adverse human rights impacts with which they are involved” (FP #11). The set of human rights includes all human rights, civil, political, economic, social and cultural rights, including the right to development – “understood, at a minimum, as those expressed in the International Bill of Rights, and the principles concerning fundamental rights set out in the International Labour Organization’s Declaration on Fundamental Principles and Rights at Work” (FP #12). Foundational Principle #13 explains the responsibility of enterprises for their direct adverse impact on human rights, namely, to “(a) [A]void causing or contributing to adverse human rights impacts through their own activities and address such impacts when they occur; (b) [S]eek to prevent or mitigate adverse human rights impacts that are directly linked to their operations, products or services by their business relationships, even if they have not contributed to those impacts.” Corporate responsibility “applies to all enterprises regardless of their size, sector, operational context, ownership and structure (FP #14). And “business enterprises should have in place policies and processes appropriate to their size and circumstances” (FP #15).

Table 1.1 Foundational principles on business and human rights (UN 2012a)

| #11 | Business enterprises should respect human rights. This means that they should avoid infringing on the human rights of others and should address adverse human rights impacts with which they are involved. |

| #12 | The responsibility of business enterprises to respect human rights refers to internationally recognized human rights – understood, at a minimum, as those expressed in the International Bill of Human Rights and the principles concerning fundamental rights set out in the International Labour Organization’s Declaration on Fundamental Principles and Rights at Work. |

| #13 | The responsibility to respect human rights requires that business enterprises: (a) Avoid causing or contributing to adverse human rights impacts through their own activities, and address such impacts when they occur; (b) Seek to prevent or mitigate adverse human rights impacts that are directly linked to their operations, products or services by their business relationships, even if they have not contributed to those impacts. |

| #14 | The responsibility of business enterprises to respect human rights applies to all enterprises regardless of their size, sector, operational context, ownership and structure. Nevertheless, the scale and complexity of the means through which enterprises meet that responsibility may vary according to these factors and with the severity of the enterprise’s adverse human rights impacts. |

| #15 | In order to meet their responsibility to respect human rights, business enterprises should have in place policies and processes appropriate to their size and circumstances, including: (a) A policy commitment to meet their responsibility to respect human rights; (b) A human rights due diligence process to identify, prevent, mitigate and account for how they address their impacts on human rights; (c) Processes to enable the remediation of any adverse human rights impacts they cause or to which they contribute. |

This brief overview of the UN Guiding Principles on Business and Human Rights may suffice for the time being because they will be discussed more extensively in Chapter 17. Still, it is noteworthy that they include many important ethical implications to be addressed as well. The terms such as “corporate responsibility,” “due diligence” and “policy commitment” clearly have an ethical meaning, in addition to their legal and social-psychological significance. However, these implications are barely articulated in the UN Framework and Guiding Principles and most often remain hidden, perhaps in order to avoid philosophical controversies that might divert attention from the urgent need of taking action against gross human rights abuses.

Having explored the actors and contents of corporate responsibility, we now turn to the third component: to which authorities or addressees business enterprises are supposed to be responsible, also discussed in Chapter 17. A first answer is given by free-market economists who claim that business executives as the “agents” are solely responsible to the shareholders of the enterprise (as the “principals”) for maximizing shareholder value. This widespread view – particularly in Anglo-Saxon countries – was strongly influenced by Milton Friedman (Reference Friedman1970) and Michael Jensen and William Meckling (Reference Jensen and Meckling1976) and is still dominant among business practitioners, professors and students and many people in other fields. However, more recently, it has been sharply criticized by, among others, Joseph Bower and Lynn Paine (Reference Bower and Paine2017) in a Harvard Business Review article.

In fact, the critique of the sole focus on shareholders has a long history going back to the early twentieth century and was thoroughly developed and expanded by Edward Freeman’s seminal contribution (Reference Freeman1984) and numerous scholars in philosophy and social sciences (Johnson-Cramer Reference Johnson-Cramer2018). Proposing a second answer of the question to whom an enterprise is responsible, the stakeholder approach includes the enterprise’s relations with all “stakeholders” defined as “any group or individual who can affect or is affected by the achievement of an organization’s objectives” (Freeman Reference Freeman1984, 46). That means not only shareholders and owners but also employees, customers, suppliers, communities and other stakeholders are relevant for managerial decisions. Managers have to respond to the interests and claims of the stakeholders and can do it in an “instrumental” way (that is, using these relations for pursuing the organization’s own interest) and/or in a “normative” way (that is, respecting the stakeholders’ rights and interests for their own sake). In other words, the responses can be viewed and theorized from the descriptive-analytical perspective of social sciences and/or from the normative-ethical perspective of philosophy, leading to so-called stakeholder theories. Thereby, many questions arise and have not been answered satisfactorily so far. Who are the relevant stakeholders? Are competitors included, as in Japanese approaches and the Caux Round Table Principles, in contrast to western approaches? Are there crucial differences between stakeholders and how are they distinguished, say, for example, between government and civil society organizations or between “primary” and “secondary” stakeholders? Can the stakeholder approach account for all key factors by which strategic management decisions are affected and which they can affect in turn? And how are instrumental and normative approaches connected to each other?

While the stakeholder approach substantially broadens and deepens the understanding of the enterprise’s connections with other social actors and its potential responsibilities towards them, it also has clear limitations for conceiving corporate responsibility in a comprehensive sense. A third answer to the question of whom an enterprise is responsible should go beyond individual social actors and include society as a whole. Public goods cannot be created and maintained by individual actors alone, but need collective actors and society as such with its formal and informal institutions. Moreover, adopting an intergenerational perspective of sustainability, corporate responsibility extends to future generations who do not yet exist and cannot be identified now, but matter nevertheless. Furthermore, as the stakeholder approach focuses on the enterprise’s relations with stakeholders, the contents of these relationships are not directly addressed. They might be partially influenced by the types of relationship with specific stakeholders and developed through stakeholder engagement and dialogue. But the stakeholder approach itself needs to be complemented by the explicit questions of contents and metrics. It cannot replace the indispensable role of widely agreed upon standards of measurement of corporate responsibility such as the sustainability reporting of the Global Reporting Initiative, the ISO 26000 standards and the UN Guiding Principles on Business and Human Rights.

In sum, all three components of responsibility are essential to fully grasp what corporate responsibility means. If any of them is missing, one cannot understand the ethics of business enterprises in a comprehensive sense. The actors who bear responsibility have to be clearly identified. The contents of responsibility need to be determined in a precise and comprehensive manner. And the authorities or addressees to whom enterprises are responsible should be legitimately established. Chapter 17 maps out these different aspects and provides numerous examples for illustration.

Chapter 18 is dedicated to corporate governance, that is, the locus where corporate responsibility has to be addressed in the first place. It is defined as the responsible direction and control of the business organization in its pursuit of creating wealth in the comprehensive sense and respecting human rights. All seven features of wealth creation are relevant for corporate governance. The narrow focus on financial capital has to be extended to economic, natural, human and social capital. The creation of wealth should include not only private but also public wealth and pay equal attention to the productive and the distributive side of directing and controlling the company. Inspired by a spiritual vision, corporate governance promotes ethical innovation in sustainable ways and is assessed in terms of human capabilities. Moreover, human rights serve as the guiding principles for corporate governance as defined in the UN Framework for Business and Human Rights. When facing difficult trade-offs and ethical dilemmas, the board has to scrutinize the seriousness of the situation, use its well-reasoned judgment and make considerate decisions: it may stick to the company’s principles and reject the trade-offs or it may strike a compromise while respecting the minimal requirements.

To conclude Part III of this book, two specific studies explicate important aspects of corporate responsibility. Chapter 19 examines corporate responsibility for reducing income inequality within the boundaries of the organization and with regard to society at large. Instead of examining the entire range of income distribution, the focus is on the lower and upper ends. The “floor“ is defined as a living wage, supported by strong economic and ethical arguments and proposed as a minimum income standard that can – and thus should – be implemented by companies. As for the ethically acceptable “ceiling” of executive compensation, its identification and justification are more complicated. However, strong economic and ethical arguments can be made in favor of a drastic reduction of top executive pay. Corporate responsibility for reducing income inequality in society means, first, to “walk the talk” and set an example and, second, to be “a good corporate citizen” by supporting legislation for a living wage and an ethically acceptable ceiling of executive pay.

Chapter 20 investigates corporate responsibility in global supply chains and how universities as powerful economic actors with a clear ethical mission can promote corporate responsibility in collaboration with their licensees and factories manufacturing trademark licensed products. This chapter chronicles the twenty-plus year history of the search of the University of Notre Dame for a responsible policy of “trademark licensing and human rights.” Notre Dame engaged two specialized organizations to assess worker participation and corporate responsibility in fourteen factories in Bangladesh, China, El Salvador, Honduras and India. In line with the United Nations Guiding Principles on Business and Human Rights, the chapter concludes with policy suggestions for other like-minded universities and outlines several research opportunities.

To round out the twenty chapters of this book, the epilogue asks again the question of the purpose of business. It has to be aligned with the purpose of the economy and take seriously its people-centered orientation. The answer proposed in this book is creating wealth in the comprehensive sense and respecting human rights. It presents a universal vision for corporate responsibility in the global and pluralistic context and aims to be relevant for any economic, political and cultural system. However, it does not address more specific challenges, which wealth creation and human rights pose in different countries, cultures and industries. Thus this book is only a beginning. It invites further investigations and conversations from multiple geographic and cultural perspectives in order to promote and strengthen the commitment of business enterprises to wealth creation and human rights.